- My Forums

- Tiger Rant

- LSU Recruiting

- SEC Rant

- Saints Talk

- Pelicans Talk

- More Sports Board

- Fantasy Sports

- Golf Board

- Soccer Board

- O-T Lounge

- Tech Board

- Home/Garden Board

- Outdoor Board

- Health/Fitness Board

- Movie/TV Board

- Book Board

- Music Board

- Political Talk

- Money Talk

- Fark Board

- Gaming Board

- Travel Board

- Food/Drink Board

- Ticket Exchange

- TD Help Board

Customize My Forums- View All Forums

- Show Left Links

- Topic Sort Options

- Trending Topics

- Recent Topics

- Active Topics

Started By

Message

re: Shocker: study suggests insurance companies are breaking it off in our butts

Posted on 5/1/26 at 10:45 am to BugAC

Posted on 5/1/26 at 10:45 am to BugAC

quote:quote:Well, they have to cover the losses for the endless amount of frivolous lawsuits. You'd be shocked at the amount of repeat offenders suing because they got in a wreck and "got injured".

"The fact that the loss ratios are so low means that the insurance industry is charging too much,"

Wouldn’t that be part of the loss ratio?

quote:

Oh you are bitching because your shop was destroyed and you only have coverage on your house? Let's call the media! You waived flood insurance despite living in a flood zone? And....most times insurance will pay it anyway, to avoid the bad press.

There’s no way you actually believe this.

quote:

I think the bitching should be done at government for requiring insurance. You want to bitch, aim it at fedgov. I think if a government is requiring a private service for its citizens, then that service is now subject to government controls.

The bank is requiring homeowner’s insurance, not the government.

1

1

Posted on 5/1/26 at 10:47 am to GeauxldMember

quote:

insurance companies are breaking it off in our butts

Posted on 5/1/26 at 10:58 am to lostinbr

quote:

Wouldn’t that be part of the loss ratio?

Part of combined ratio. Loss ratio is usually directly related to claims payouts.

Posted on 5/1/26 at 11:02 am to DCtiger1

quote:

You want 30 years to pay it back? Well then you need insurance. Don't see the issue

What about with only 10 years to go? 5?

Posted on 5/1/26 at 11:06 am to UptownJoeBrown

Just talked to somebody whose elderly parent was somehow paying $127 a month for a single land-line phone line. Random taxes and fees were 20% of the bill.

How much of the US economy is a result of older people getting exorbitantly overcharged on phone, cable, internet, insurance, security systems?

How much of the US economy is a result of older people getting exorbitantly overcharged on phone, cable, internet, insurance, security systems?

Posted on 5/1/26 at 11:14 am to UptownJoeBrown

quote:

What about with only 10 years to go? 5?

The house is an asset as a whole unit. Are you suggesting you should pay less because you owe less when the asset and cost to replace has appreciated and increased over the same time period?

Posted on 5/1/26 at 11:14 am to GeauxldMember

quote:

I’m sure it won’t take long for our resident insurance agents to come white knighting for the industry and poo-poo this study.

You believe every study put out out just those that confirm your bias? I can show you studies that show that kids of gay parents turnout better than kids of straight parents.

quote:

Brian Shearer, director of competition and regulatory policy at the Vanderbilt University think tank and a former senior adviser at the Consumer Financial Protection Bureau.

Wonder if he’s ever come to another conclusion when he performed a “study”?

Posted on 5/1/26 at 11:20 am to UptownJoeBrown

quote:

What about with only 10 years to go? 5?

Does insurance cover the mortgage or the actual dwelling?!?

Posted on 5/1/26 at 11:58 am to GeauxldMember

suggests

—-not exactly stone cold proof

—-not exactly stone cold proof

Posted on 5/1/26 at 1:10 pm to BugAC

quote:

What's wrong with making a profit?

Nothing.

Posted on 5/1/26 at 1:13 pm to UptownJoeBrown

quote:

What about with only 10 years to go? 5?

What about it. No relevance to the insurance carrier other than noting whose getting billed for payments

Posted on 5/1/26 at 1:52 pm to Chad504boy

OP calls out insurance agents, everyone disappears from logical debate. Every single thread every single time

Posted on 5/1/26 at 2:56 pm to BugAC

quote:

So frivolous lawsuits play no part in any of this?

Yeah, I bet frivolous lawsuits account for far more than 80 years of collusion and anti trust behavior.

Please tell me about all the frivolous lawsuits against property and casualty insurers that are releasing record earnings year after year. Many states have specific laws in place to protect insurers against unmerited claims of damages.

Most states (except Mississippi) have adopted some form of the NAIC Model Act or similar fair claims handling regulations, which provide a standard framework for what constitutes valid vs. unfair claims. Additionally, states like California and Illinois have specific Insurance Fraud Prevention Acts that allow insurers to actively sue and recover funds from those filing fraudulent or meritless claims.

Sure, there are ambulance chasers looking for quick payouts, but nowhere near the number of people left holding the bag with denied claims in major disaster events, all to protect balance sheets of extraordinarily healthy companies who would rather invest that money for even higher returns on the premiums they’ve been paid for years by policy holders.

Posted on 5/1/26 at 2:59 pm to Dixie2023

quote:

Insurance is mostly legal thievery.

it's transfer of risk to protect against catastrophic loss

Posted on 5/1/26 at 3:01 pm to The Third Leg

In the last five years, P&C carriers have paid out well in excess of 2.5 Trillion in claims.

Posted on 5/1/26 at 3:10 pm to UptownJoeBrown

quote:

Mortgage? Required to have it.

As you should be.

quote:

Auto? Required to have it if owe on it.

As you should be.

quote:

Businesses? Required by law if you have employees

As you should be.

I mean I guess a bank could make loans to people with none of that coverage, but they wouldn't be in business long

This post was edited on 5/1/26 at 3:10 pm

Posted on 5/1/26 at 3:13 pm to DCtiger1

quote:

OP calls out insurance agents, everyone disappears from logical debate. Every single thread every single time

You came in here and were gonna post this either way, weren't you?

Because I see two pages worth of logical debate. But I guess nice work, you got to post your thing?

Posted on 5/1/26 at 3:22 pm to DCtiger1

quote:

In the last five years, P&C carriers have paid out well in excess of 2.5 Trillion in claims.

Considering they’re insuring trillions of dollars in assets, this should be no surprise they paid a few trillion in claims the last five years.

P&C industry as a whole has an annualized average policy holder surplus of $1T each of the last 3 years

They also regularly deny valid claims and frick their policyholders over. The stories are endless, major disaster comes through, insurers frick policyholders, lawsuits ensue, insurers cry about litigation driving premiums through the roof. Meanwhile…

This post was edited on 5/1/26 at 3:23 pm

Posted on 5/1/26 at 3:34 pm to The Third Leg

those profits include investment returns, which are premium reserves. 2024 is rates catching up to risk and now rates are going back down.

If you think insurance companies shouldn't be profitable, start your own insurance company. 100s of millions of claims are handled every year without incident. Lawsuits from catastrophes generally originate from customers not understanding their policies.

I was helping a customer with a claim from a tornado. Insurance company wanted to repair the roof, he wanted replacement. Got him full replacement payout. Guess what he did? he repaired the roof and pocketed the rest.

If you think insurance companies shouldn't be profitable, start your own insurance company. 100s of millions of claims are handled every year without incident. Lawsuits from catastrophes generally originate from customers not understanding their policies.

I was helping a customer with a claim from a tornado. Insurance company wanted to repair the roof, he wanted replacement. Got him full replacement payout. Guess what he did? he repaired the roof and pocketed the rest.

Posted on 5/1/26 at 3:45 pm to DCtiger1

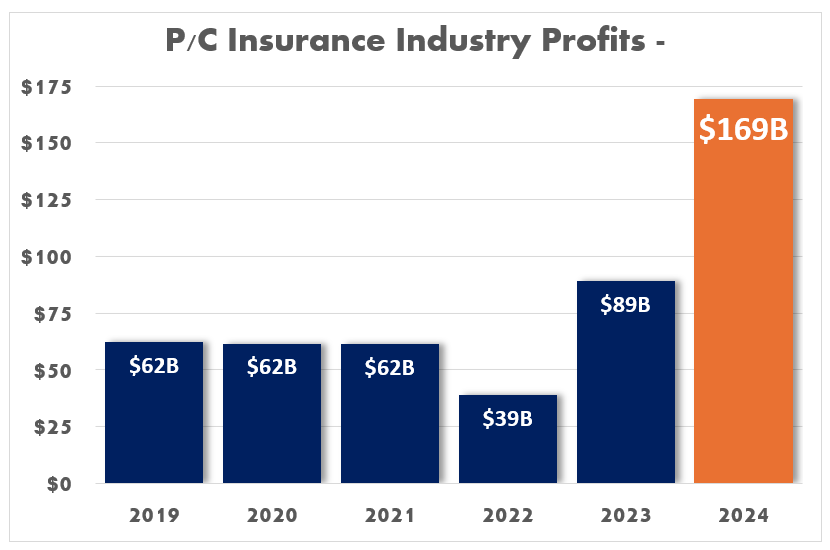

Net Underwriting Gain/Loss:

2025: Estimated $63 billion gain, a significant leap from the $23 billion gain in 2024.

2024: Recorded a $23 billion gain, recovering from a $22 billion loss in 2023

I would assume looking at those numbers, and the $1T surplus — which is money available to pay claims — we will all be getting dirt cheap insurance for a brief period. But we all know these massive hikes were nothing more than profiteering and the prices are never coming down. Worth noting here that in 2025, the premiums paid for P&C eclipsed $1T for the first time.

It’s the ultimate grift. Federal government can’t touch you, states aren’t powerful enough to take on the industry and regulate it. Legislators even design laws to protect them.

But man, that guy pocketed $2K of the $100k he paid your employer for his new roof. What benevolence!

2025: Estimated $63 billion gain, a significant leap from the $23 billion gain in 2024.

2024: Recorded a $23 billion gain, recovering from a $22 billion loss in 2023

I would assume looking at those numbers, and the $1T surplus — which is money available to pay claims — we will all be getting dirt cheap insurance for a brief period. But we all know these massive hikes were nothing more than profiteering and the prices are never coming down. Worth noting here that in 2025, the premiums paid for P&C eclipsed $1T for the first time.

It’s the ultimate grift. Federal government can’t touch you, states aren’t powerful enough to take on the industry and regulate it. Legislators even design laws to protect them.

But man, that guy pocketed $2K of the $100k he paid your employer for his new roof. What benevolence!

Page 4 of 10

Page 4 of 10

Popular

Back to top