- My Forums

- Tiger Rant

- LSU Recruiting

- SEC Rant

- Saints Talk

- Pelicans Talk

- More Sports Board

- Fantasy Sports

- Golf Board

- Soccer Board

- O-T Lounge

- Tech Board

- Home/Garden Board

- Outdoor Board

- Health/Fitness Board

- Movie/TV Board

- Book Board

- Music Board

- Political Talk

- Money Talk

- Fark Board

- Gaming Board

- Travel Board

- Food/Drink Board

- Ticket Exchange

- TD Help Board

Customize My Forums- View All Forums

- Show Left Links

- Topic Sort Options

- Trending Topics

- Recent Topics

- Active Topics

Started By

Message

I hate to admit this but cutting right now would be bad

Posted on 9/11/25 at 12:28 pm

Posted on 9/11/25 at 12:28 pm

Id rather have a recession right now than have inflation.

7

7

Posted on 9/11/25 at 6:44 pm to TigersHuskers

A question about the economy? Are we to root for unemployment to go up OR inflation? Is there a way out without either of those options? Or stagflation? Are any of them lesser evils?

Seems like there is a large portion of society living in astronomical unhealthy debt. Thats not a problem that can be solved without some serious education and a lot of time.

Seems like there is a large portion of society living in astronomical unhealthy debt. Thats not a problem that can be solved without some serious education and a lot of time.

Posted on 9/12/25 at 8:19 am to TigersHuskers

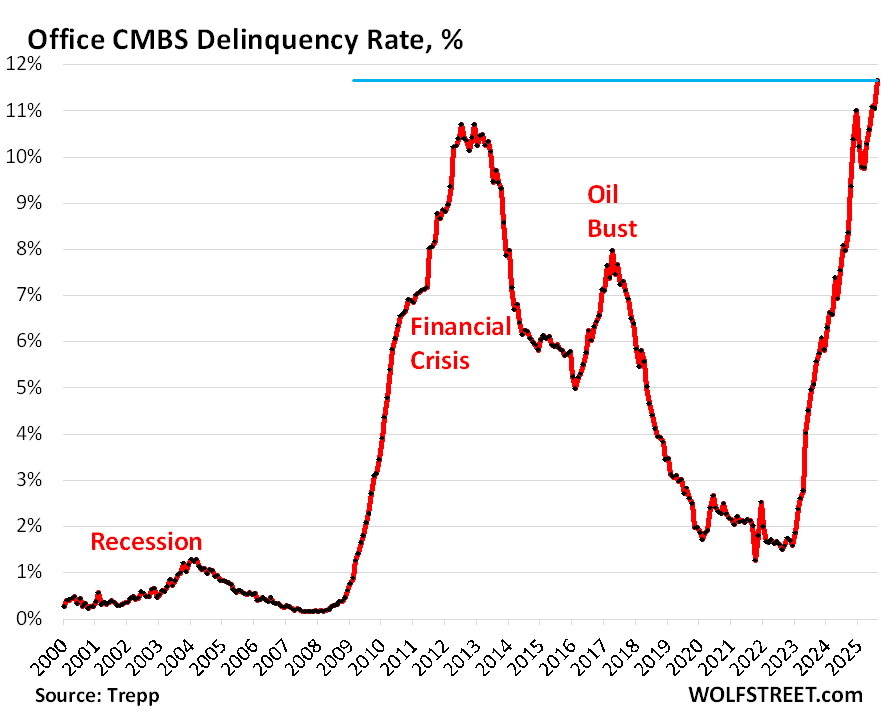

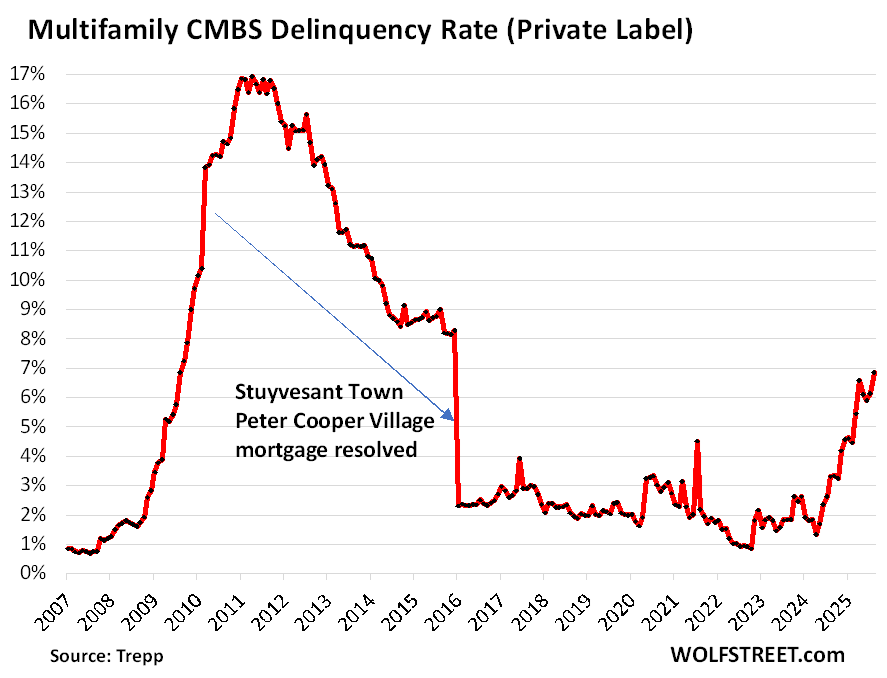

If you don’t cut the rates we are going to have massive bank failures across the US because of the CMBS exposure. Banks tied to SF, Chicago, Atlanta commercial office and NY apartments are in significant turmoil unless those the developers/property owners can refinance those loans others the defaults will wipe a lot of banks out.

The exposures are a real problem in NY especially with the stupid rent caps the city instituted years ago.

Can’t have another round of bank failures right now. As of last Dec there were over 68 at risk of failure. Also would allow states and local gov’ts to refinance their loan obligations thus lowering the interest payments they are paying.

The exposures are a real problem in NY especially with the stupid rent caps the city instituted years ago.

Can’t have another round of bank failures right now. As of last Dec there were over 68 at risk of failure. Also would allow states and local gov’ts to refinance their loan obligations thus lowering the interest payments they are paying.

This post was edited on 9/12/25 at 8:22 am

Posted on 9/12/25 at 8:26 am to TigersHuskers

How can blackstone buy up all the single family homes in America if rates aren’t lowered? How can the Chinese and bill gates buy up all the farmland?

Some of you people are so greedy wanting your own house and food to eat

Some of you people are so greedy wanting your own house and food to eat

Posted on 9/12/25 at 9:17 am to MrLSU

quote:

If you don’t cut the rates we are going to have massive bank failures across the US because of the CMBS exposure. Banks tied to SF, Chicago, Atlanta commercial office and NY apartments are in significant turmoil unless those the developers/property owners can refinance those loans others the defaults will wipe a lot of banks out.

Holy overreaction Batman

Posted on 9/12/25 at 9:20 am to MrLSU

quote:

NY apartments are in significant turmoil

OH NOZ!!

Posted on 9/12/25 at 9:26 am to WhiskeyThrottle

quote:

A question about the economy? Are we to root for unemployment to go up OR inflation? Is there a way out without either of those options? Or stagflation? Are any of them lesser evils?

The TL;DR answer is to root for unemployment to go up (because inflation is the problem and the only way we're going to drain off enough of the money supply is through high unemployment). Inflation's continued growth will lead to that anyway.

The quick answer is that there's no way out of this without pain and there never has been (contrary to happy-fluffy talk about "soft landings"). You can't distort currency values like we saw during COVID without the eventual adjustment being painful. We're already in a "stagflation-lite" scenario with growing Unemployment and growing Inflation but while also having positive GDP growth. We will go through stagflation, into recession. The recession will be bad, but we will eventually come out of it and see tons of growth.

The longer answer starts with where we are currently:

-Inflation (CPI/PCE) has been growing since April

-PPI has been seeing steady growth since the end of 2023

-Job growth has been slowing (and we're seeing that it was FAR more than early numbers showed)

-Unemployment has been slowly growing

-Initial claims have been slowly growing since January 2024

-Continued claims have been slowly growing since mid-2022

-Wage growth has been dropping since ~June 2024

-Consumer credit card balances have shot up since COVID (at a greater pace than pre-COVID)

-Credit card default rates and delinquency rates have shot up since 2021 to 2012 levels (for context, post-GFC through COVID we saw those levels being well below that of the previous couple of decades) with delinquencies still being below the overall average but defaults being at the high end of what we saw leading up to 2000.

-GDP has been largely positive, but that growth has been slowly shrinking since 2023

-Government deficit spending has been out of control since COVID (it was merely "bad" to "really bad" since the GFC)

-Economic growth is usually built on debt being created somewhere, but a healthy economy has debt being created and discharged at a healthy pace. Generally, if your Debt to GDP ratio is 60% or below, you've got a strong economy. A ratio over 60%, therefore, means an economy is more unhealthy/fragile the higher that ratio goes (and the longer it stays there). The US hasn't been at 60% (much less below it) since 2005, hasn't been below 90% since 2010, hasn't been below 100% since 2015 and hasn't been below 115% since 2020.

So we have an economy so dependent on continued (and escalating) public and private debt growth that even modest GDP growth requires large annual debt increases. That's not a sustainable path, but like weening an addict off of drugs it's going to mean a lot of pain to correct the issue.

If inflation is a function of too much money chasing too few goods (it is), then in a society willing to create larger and larger amounts of public and private debt in order to avoid even a minor lifestyle hit to an already high lifestyle (compared to the rest of the world), we can reasonably expect inflation to continue to rise for at least the near term. The rate cut (and possible other ones for this year) will not create enough jobs to reverse the problem because the problem isn't jobs, it's inflation.

The market will probably react favorably next week to whatever cut we get, but inflation will continue. When inflation doesn't go down in a couple of months, businesses are going to get concerned and begin layoffs. So we'll have inflation continuing to grow while job growth continues to bounce around but unemployment continues it's slow, plodding trek upward. This means we'll stick in a stagflation environment until inflation growth comes to the point where businesses realize they cannot grow their way out of it (again, because employment isn't the problem, inflation is) so they cut jobs because that's all that's left to them to keep revenues positive.

At that point unemployment begins rising faster. Enough high unemployment (for context, the average unemployment rate going back to the 1940s is 5.7%) for long enough will move us from stagflation into a recession. The consumer debt issue is going to greatly enhance both the unemployment climb as well as the depth of the recession (due to the economy being so dependent on continued high debt growth). Such a recession would cause deflation (due to lack of credit access for many). This will allow for more rate cuts, eventually bringing rates extremely low once again. At that point we begin climbing out of the recession and back into growth.

The big factor on how long the recession lasts before recovery can begin will be government spending. The kneejerk reaction for government is to increase spending on "welfare" programs. As more people move onto those programs, that's going to mandate more deficit spending by the federal government, thus dragging out the inflation problem by keeping the money supply too full. How much that happens is anyone's guess. If it's too much deficit spending (enough to stave off deflation), then the can is just kicked down the road a bit and the recovery growth is tempered.

Posted on 9/12/25 at 3:55 pm to Craft

This post was edited on 9/12/25 at 3:57 pm

Posted on 9/12/25 at 5:16 pm to TigersHuskers

I think the public’s reaction to the inevitable cut will be counter intuitive.

After people discover the .25% reduction they waited three years for does little to change the 30% APR on their credit cards or 7% on mortgages….the pitch forks with begin to gather and the drumbeat to provide more will get louder.

After people discover the .25% reduction they waited three years for does little to change the 30% APR on their credit cards or 7% on mortgages….the pitch forks with begin to gather and the drumbeat to provide more will get louder.

Posted on 9/12/25 at 5:49 pm to Bard

quote:

The big factor on how long the recession lasts before recovery can begin will be government spending.

Bingo, too much at stake for everyone in politics to let a serious recession occur. They will spend their way out of it and kick the can down the road.

Posted on 9/12/25 at 6:42 pm to lsuconnman

Well…yeah, there won’t be just one.

Posted on 9/13/25 at 10:35 am to MrLSU

I’m old enough to remember when they allowed recessions to clean up shite like this.

And as for poor public policy, they voted for it so they deserve it.

And as for poor public policy, they voted for it so they deserve it.

Posted on 9/13/25 at 11:51 am to TigersHuskers

We have been in a recession

The last admin change the definition

And created 2mil fake jobs

The last admin change the definition

And created 2mil fake jobs

Posted on 9/13/25 at 12:51 pm to TigersHuskers

a .25% would still signal general confidence in the economy and the markets would react favorably. .5% would spark more fear and would likely be viewed negatively.

Posted on 9/13/25 at 1:22 pm to MrLSU

The CRE market has been a ticking bomb in plain sight for 5 years. Are you telling me there’s a shitload of CRE MBS’s out there?

Great.

Great.

This post was edited on 9/13/25 at 1:23 pm

Posted on 9/15/25 at 7:48 am to SquatchDawg

CRE loans are a huge problem. Most are 5-year ARMs or balloons. Businesses refi’ing a 3% to 6.5-7% now. Some won’t even qualify.

As for Blackrock and China - the reason they are so prominent is the lack of demand competition from average Americans that are sidelined by high rates.

Guarantee you China doesn’t care what American interest rates are when they buy American properties.

As for Blackrock and China - the reason they are so prominent is the lack of demand competition from average Americans that are sidelined by high rates.

Guarantee you China doesn’t care what American interest rates are when they buy American properties.

Posted on 9/15/25 at 9:17 am to TigersHuskers

I want a 15% rate

Posted on 9/15/25 at 1:26 pm to SDVTiger

Lol, they sure don't like the truth around here do they?

Posted on 9/16/25 at 12:04 am to SDVTiger

quote:

We have been in a recession The last admin change the definition

By that very definition we have not been in a recession since 2022.

Posted on 9/16/25 at 5:55 am to slackster

quote:

By that very definition we have not been in a recession since 2022.

So we were in a recession in 2022?

Page 1 of 2

Page 1 of 2

Back to top