- My Forums

- Tiger Rant

- LSU Recruiting

- SEC Rant

- Saints Talk

- Pelicans Talk

- More Sports Board

- Fantasy Sports

- Golf Board

- Soccer Board

- O-T Lounge

- Tech Board

- Home/Garden Board

- Outdoor Board

- Health/Fitness Board

- Movie/TV Board

- Book Board

- Music Board

- Political Talk

- Money Talk

- Fark Board

- Gaming Board

- Travel Board

- Food/Drink Board

- Ticket Exchange

- TD Help Board

Customize My Forums- View All Forums

- Show Left Links

- Topic Sort Options

- Trending Topics

- Recent Topics

- Active Topics

Started By

Message

Basic math of Roth vs Traditional many get wrong

Posted on 5/16/26 at 4:01 pm

Posted on 5/16/26 at 4:01 pm

Many including professionals get the basic Roth vs Traditional math concept wrong. This makes it nearly impossible for them to get strategies right to address complexities including widow penalty, shifting tax rates, IRMAA, ACA subsidy income limits, tax credits, inheritance etc.

Several posts in the previous thread didnt seem to grasp the commutative property of multiplication and/or conflated paying lower total taxes with a better net balance after taxes. I encounter this often from the "almost always choose Roth crowd." I'm a big proponent of Roth myself but it isnt always optimal. That said, when in doubt probably go Roth.

This video tackles the foundational math mistakes even some pros get wrong YouTube The Retirement Nerds

(rewind if you want the full context and intro)

Several posts in the previous thread didnt seem to grasp the commutative property of multiplication and/or conflated paying lower total taxes with a better net balance after taxes. I encounter this often from the "almost always choose Roth crowd." I'm a big proponent of Roth myself but it isnt always optimal. That said, when in doubt probably go Roth.

This video tackles the foundational math mistakes even some pros get wrong YouTube The Retirement Nerds

(rewind if you want the full context and intro)

This post was edited on 5/16/26 at 4:17 pm

11

11

Posted on 5/16/26 at 5:01 pm to TorchtheFlyingTiger

I have a pretty decent mixture of both, pre-tax and post-tax accounts. I figure in retirement there might be advantages to being able to withdraw from whichever one I want.

This post was edited on 5/16/26 at 5:10 pm

Posted on 5/16/26 at 5:36 pm to TorchtheFlyingTiger

Honestly, how many people fall into the category of earning enough where the traditional is more beneficial than the Roth?

Posted on 5/16/26 at 7:15 pm to lsuconnman

More than you might think. If you dont have pension or other sizeable income sources in retirement the effective tax rate on withdrawals as a primary income source could be quite low. For instance, if in 22% bracket while contributing you could have same income from withdrawals but pay a much lower EFFECTIVE rate due to most of income falling in standard deduction and 10% bracket before a fraction hits 22%.

Posted on 5/16/26 at 8:34 pm to lsuconnman

quote:

Honestly, how many people fall into the category of earning enough where the traditional is more beneficial than the Roth?

The sweet spot is to have enough traditional so that your trad withdrawals + SS + keeps you in the 12% bracket, then Roth after that.

Some people are late starters. They are probably better off in trad.

Sometimes plans change, such as getting married late in life, then all the math changes.

Some people want to retire early and use 72t withdrawals. If you draw your assets early, even without penalty, some of the Roth tax benefits go away. You can get by this in a Roth IRA by converting trad to Roth, but you have to have trad first.

A Roth Ladder might be very useful if you retire early, but you have to convert from trad.

Some people want to do trad now then convert it to Roth when they are retired and have lower income, therefore paying lower taxes on the conversion.

Some people want to use trad contributions to lower their taxable income to get a more favorable tax outcome, maybe to try to avoid IIRMA when they retire.

Posted on 5/16/26 at 8:49 pm to CharlesUFarley

I created a traditional a couple years ago because of insight from the MB. It’s still at zero $ because I discovered I might be poor.

…I also tried to get a health care plan that offered the HSA benefits, but discovered every eligible plan had a copay.

This place is definitely hit or miss.

…I also tried to get a health care plan that offered the HSA benefits, but discovered every eligible plan had a copay.

This place is definitely hit or miss.

Posted on 5/16/26 at 9:05 pm to TorchtheFlyingTiger

quote:Thanks for posting.

Basic math of Roth vs Traditional many get wrong

Many including professionals get the basic Roth vs Traditional math concept wrong.

Posted on 5/16/26 at 9:31 pm to lsuconnman

quote:But for those who do, unless soak-the-rich rates raise our kids' taxes above our 40.8% Federal rate, tax advantages will be flipped.

Honestly, how many people fall into the category of earning enough where the traditional is more beneficial than the Roth?

Intuitively, the backdoor Roth thing made no sense in our circumstance. The OP demonstrates that mathematically.

In simple terms, my takeaway is if the contributional tax bracket is higher than the withdrawal tax bracket (peak earnings contributions, heirs in lower brackets, etc.), Roth is a dubious strategy. If the reverse is the case, and especially if the differential is predictably pronounced (e.g., early career earnings, heirs financially more successful, etc.), a Roth should be beneficial.

This post was edited on 5/17/26 at 4:54 am

Posted on 5/16/26 at 9:34 pm to TorchtheFlyingTiger

[url=LINK ]  [/url]

[/url]

[/url]Posted on 5/16/26 at 10:33 pm to fallguy_1978

quote:

I have a pretty decent mixture of both, pre-tax and post-tax accounts. I figure in retirement there might be advantages to being able to withdraw from whichever one I want.

Same. My portfolio is split between pre-tax (54%), taxable (17%) and tax free (29%).

I will have options to control my taxable income when I retire.

Posted on 5/16/26 at 10:37 pm to TorchtheFlyingTiger

quote:

but it isnt always optimal

I don’t think I’ve ever seen anyone here actually state it is always better.

This post was edited on 5/16/26 at 10:55 pm

Posted on 5/17/26 at 12:02 am to lsuconnman

quote:

Honestly, how many people fall into the category of earning enough where the traditional is more beneficial than the Roth?

I did. I think a lot of people do, especially in their peak earning years.

Have a trajectory to RMD kaboom to prove it!

Posted on 5/17/26 at 5:12 am to dragginass

While the commutative property argument is very real for some people, it assumes the same tax rate now and later, which really isn’t the case for many…

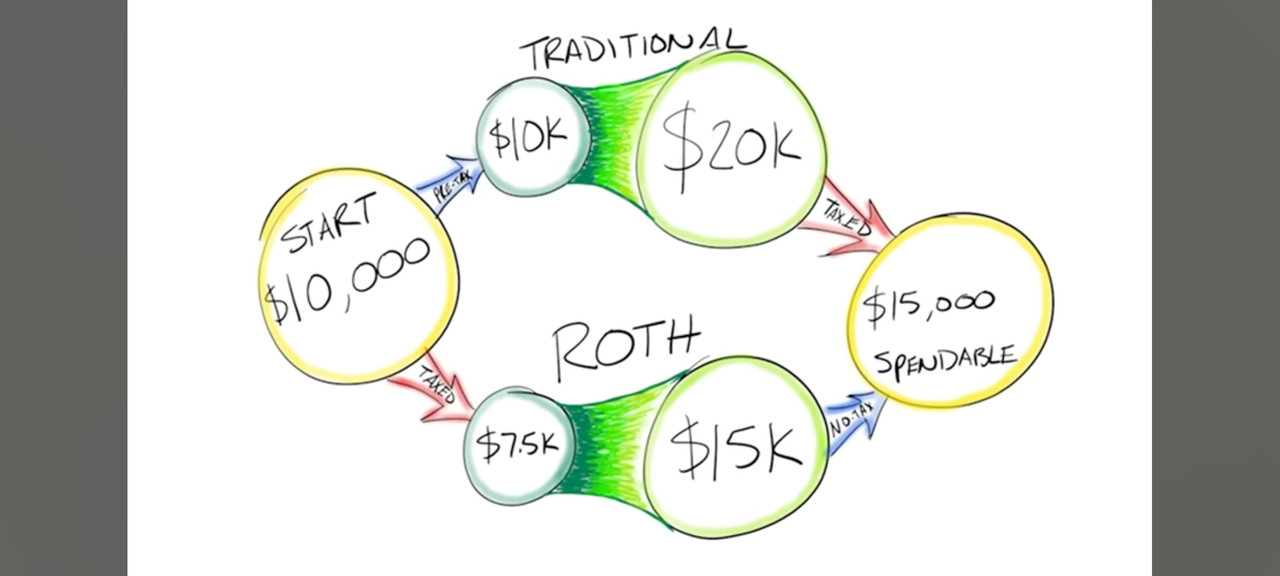

Traditional: $10k - no tax - x2 = $20k - 12% taxed = $17,600 spendable

Roth: $10k - 22% tax = $7800 - x2 = $15,600 - no tax = $15,600 spendable

This is why I contribute 100% of my 401k traditional and supplement with 2 Roth IRAs and cash.

Traditional: $10k - no tax - x2 = $20k - 12% taxed = $17,600 spendable

Roth: $10k - 22% tax = $7800 - x2 = $15,600 - no tax = $15,600 spendable

This is why I contribute 100% of my 401k traditional and supplement with 2 Roth IRAs and cash.

Posted on 5/17/26 at 7:51 am to CecilShortsHisPants

Agreed, tax rate is the primary variable. Specifically, current bracket vs future EFFECTIVE rate on withdrawals.

I'm just repeatedly surprised by the prevalence of misunderstanding how the math actually works. In previous thread, I was told it was a "very short sighted strategy" to prefer projected 12% Traditional withdrawals over 22% Roth contributions. (that poster mentions clients which is troubling) Another responder made the common mistake that Roth beats traditional the more years you have. We even have those insisting on comparing same exact contribution amount ignoring tax on Roth contributions. Unfortunately, those that dont grasp the foundational math are often strong proponents confidently spreading their misinformation.

Thats before getting into the many complexities of individual situations. The math is no longer simple when accounting for all the factors that effect actual effective withdrawal tax rate. But if they dont get that simple math right the complex math is impossible.

I'm just repeatedly surprised by the prevalence of misunderstanding how the math actually works. In previous thread, I was told it was a "very short sighted strategy" to prefer projected 12% Traditional withdrawals over 22% Roth contributions. (that poster mentions clients which is troubling) Another responder made the common mistake that Roth beats traditional the more years you have. We even have those insisting on comparing same exact contribution amount ignoring tax on Roth contributions. Unfortunately, those that dont grasp the foundational math are often strong proponents confidently spreading their misinformation.

Thats before getting into the many complexities of individual situations. The math is no longer simple when accounting for all the factors that effect actual effective withdrawal tax rate. But if they dont get that simple math right the complex math is impossible.

This post was edited on 5/17/26 at 7:55 am

Posted on 5/17/26 at 9:49 am to TorchtheFlyingTiger

quote:

many complexities

We under-educate our populace on personal finance. We have over complicated our personal finance tools & rules. Understatement!

Roth vs Traditional

59.5yo withdrawals penalty unless 72(t), Rule of 55 or withholding tax triggers penalty if neither and…

Don’t roll 401k to IRA if…

Watch out for pro rata rule in Roth Conversions

MAGI for IRMAA, AGI for…

2-yrs income before Medicare / IRMAA

Tax deferred, taxable, tax free layers

Capital gains tax table % break lines

Qualified vs non qualified

LTCG vs ordinary income tax

…and many more

…before even getting to estate planning starting line.

As if market and interest rate / inflation risk are not enough, we have created high complexity risk.

FA/Estate Attorneys 1, Avg Joe Citizen 0...unless & until AI cometh (kidding...its here).

When I helicopter up, it seems more than a bit ridiculous.

This post was edited on 5/17/26 at 10:37 am

Posted on 5/17/26 at 10:19 am to lsuconnman

quote:

how many people fall into the category of earning enough where the traditional is more beneficial than the Roth?

me. i have had a TIRA for ages. had no choice.

Posted on 5/17/26 at 10:51 am to TorchtheFlyingTiger

I have said this in other posts, but everyone should at least try to project actual after tax income once you start taking Social Security, and of course in combination with other income sources you might have, like pension or rental income or cap gains and interest from taxable accounts.

The math changes for every variable I just stated, and still changes for every variable mentioned in the posts above. The Roth could be huge for some, a handy tool for others. Every situation is different. There is no one size fits all. And of course, the further out you project, the less accurate your projection, so you need to run your projections every year and adjust your allocation to Roth and Trad and taxable accordingly.

The math changes for every variable I just stated, and still changes for every variable mentioned in the posts above. The Roth could be huge for some, a handy tool for others. Every situation is different. There is no one size fits all. And of course, the further out you project, the less accurate your projection, so you need to run your projections every year and adjust your allocation to Roth and Trad and taxable accordingly.

Posted on 5/17/26 at 12:02 pm to TorchtheFlyingTiger

Has anyone developed an AI tool where you just plug in all the assumptions and voila!

My situation is difficult because my income can fluctuate pretty significantly. And what I consider “retirement” is going to be a steady off ramp over the next 3-5 (I’m 51) years that results in some very part time low-stress completely remote work that I actually enjoy and keeps my mind sharp.

We will also have three houses with no debt (two of them at least periodically rented and can be full-time).

I’ve paid into SS since I was whatever age they allow you do be a W2 employee (my first job was at 12).

It’s really hard for me to calibrate everything under these circs. Right now we have all SEP and trad IRAs and a couple 403(b)s we need to roll over.

My situation is difficult because my income can fluctuate pretty significantly. And what I consider “retirement” is going to be a steady off ramp over the next 3-5 (I’m 51) years that results in some very part time low-stress completely remote work that I actually enjoy and keeps my mind sharp.

We will also have three houses with no debt (two of them at least periodically rented and can be full-time).

I’ve paid into SS since I was whatever age they allow you do be a W2 employee (my first job was at 12).

It’s really hard for me to calibrate everything under these circs. Right now we have all SEP and trad IRAs and a couple 403(b)s we need to roll over.

This post was edited on 5/17/26 at 12:03 pm

Posted on 5/17/26 at 12:29 pm to fallguy_1978

quote:

I figure in retirement there might be advantages to being able to withdraw from whichever one I want.

Correct. There is a strategy for this. You really need three different retirement vehicles to draw from. I realize for a lot of folks this isn’t an option but if you have a 401k, Roth, and HSA for example you are going to be able to have a huge advantage when it comes to to withdrawal strategies.

Posted on 5/17/26 at 1:13 pm to TorchtheFlyingTiger

Right now 52% of investments are Roth/brokerage. 48% in traditional ira. Anticipate when we retire about 60% with be post tax but think that’ll help since retiring early and can be flexible with some tax planning

Page 1 of 3

Page 1 of 3

Popular

Back to top