- My Forums

- Tiger Rant

- LSU Recruiting

- SEC Rant

- Saints Talk

- Pelicans Talk

- More Sports Board

- Fantasy Sports

- Golf Board

- Soccer Board

- O-T Lounge

- Tech Board

- Home/Garden Board

- Outdoor Board

- Health/Fitness Board

- Movie/TV Board

- Book Board

- Music Board

- Political Talk

- Money Talk

- Fark Board

- Gaming Board

- Travel Board

- Food/Drink Board

- Ticket Exchange

- TD Help Board

Customize My Forums- View All Forums

- Show Left Links

- Topic Sort Options

- Trending Topics

- Recent Topics

- Active Topics

Started By

Message

re: A quarter of Americans have no retirement savings. Zero.

Posted on 5/30/26 at 9:20 am to StormyMcMan

Posted on 5/30/26 at 9:20 am to StormyMcMan

quote:

To be fair, most of today's 65–74-year-olds spent much of their careers before 401(k)s became common. Many expected to retire with pensions, so comparing their 401(k) balances to younger workers can be a little misleading

This is a very accurate statement. I am very fortunate that I am at a company that provides a very healthy contribution to my 401k. I wish I would have started with them earlier.

0

0

Posted on 5/30/26 at 9:23 am to Slippy

quote:

What are these millions upon millions of people going to do to support themselves when they get old? What happens if social security goes belly up?

You just explained why policy wise the country will never let social security fail. Benefits may go down over time, but taxpayers will continue to fund this because old people vote.

Posted on 5/30/26 at 9:27 am to Centinel

I agree with this. I am 44 and will get nothing if they means test. But lets say they do this in 10 years, before I got to my retirement. They will still take out the 13% from my payroll taxes, and then still tell me I am not paying my fair share

Posted on 5/30/26 at 9:29 am to Slippy

But they got a new car!

Posted on 5/30/26 at 9:30 am to UltimaParadox

quote:

se old people vote.

They also die and if we don’t repopulate to cover the deceased there could be quite a few bucks freed up.

Posted on 5/30/26 at 9:30 am to AndyJ

quote:

will get nothing if they means test.

You worked hard and saved AND paid in the wealth distribution program???

frick you dude you get nothing!

Posted on 5/30/26 at 9:32 am to Slippy

I know I am coming into this thread late, but I’m going to add my two cents, if they didn’t say for retirement, that’s a choice they made, it may not have been a choice not to say they may have made other choices that put them in their predicament, but I made a choice to bust my butt for 36 years in sack away as much as I could, and work for an employer who had a good retirement plan and never switched jobs and toughed it out, I didn’t live recklessly, I had fun, but I managed my money. I also know that there are persons that have psychological issues that put them in a different predicament, but otherwise people make choices in those choices have ramifications either good or bad.

Posted on 5/30/26 at 10:03 am to Rabt

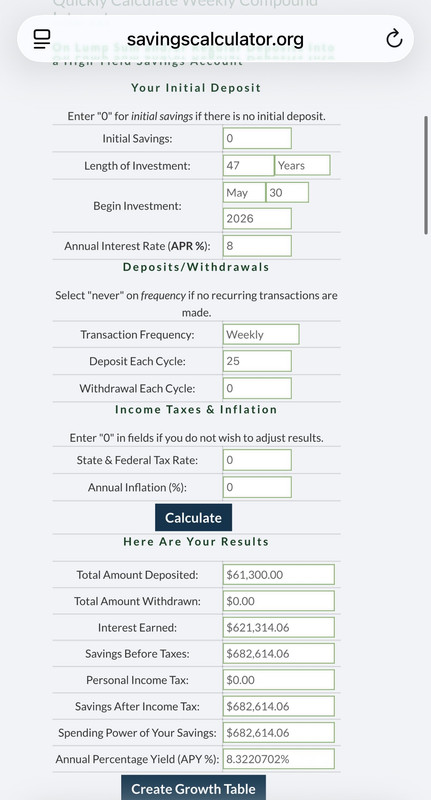

quote:You left 18% on the table, it’s actually ~$682k

Investing $25 a week starting at age 18 through age 65(47 yrs) at 8% interests/growth = $557,000.

Posted on 5/30/26 at 10:15 am to StormyMcMan

quote:1978 is when the Tax Code was changed to allow 401(k) savings.

To be fair, most of today's 65–74-year-olds spent much of their careers before 401(k)s became common.

Hughes Aircraft set up the first one three weeks after the adoption but were extremely nervous about whether it was legal or not. The tale of the tape came the following year after their employees who had contributed to the company plan in Tax Year 1978 weren’t audit/penalized for their compliant contributions.

401(k) plans were slow to catch on; pensions were still available in many industries and blue collar folks didn’t really take a personal hand in investing. (Due, in some parts to not having extra money to invest or, if they did, there was still some institutional distrust of the stock market & brokerage firms held-over from the Great Depression).

This post was edited on 5/30/26 at 10:16 am

Posted on 5/30/26 at 10:33 am to soccerfüt

quote:

pensions were still available in many industries and blue collar folks didn’t really take a personal hand in investing

GM gutted my grandfather's pension and health benefits shortly after his retirement in the 80s. I've never trusted anything (including SS) where I wasn't in active control of the $.

Posted on 5/30/26 at 10:41 am to AndyJ

It's fun to get penalized for doing the right thing.

Posted on 5/30/26 at 10:42 am to HailHailtoMichigan!

quote:

individuals are predominantly at fault,

FIFY

Posted on 5/30/26 at 10:44 am to armytiger96

quote:

Almost half of Boomer generation earned a pension as part of their employee benefits.

I seriously doubt that.

If fact the % of baby boomers with a pension is equal to the % of baby boomers that don't even have retirement accounts, both around 20-24%.

The average balance of 200K in retirement savings doesn't include those without retirement accounts. 1/5 boomers aren't factored into the equation.

Posted on 5/30/26 at 10:59 am to TigerintheNO

Agreed.

Once 401k's started pensions started to dissappear.

I do know a lot of folks with military retirements and I assume that counts as a pension.

Once 401k's started pensions started to dissappear.

I do know a lot of folks with military retirements and I assume that counts as a pension.

Posted on 5/30/26 at 11:01 am to F1y0n7h3W4LL

quote:

That gives me nightmares just to read about it.

I've had inlaws who died penniless and struggled to just eat in old age.

My mother (91) and MIL (early 80s) are in that exact position today. Both "retired" in their 60s, but had plenty of fuel in the tank, should kept on working.

Posted on 5/30/26 at 11:13 am to TigerintheNO

quote:

I seriously doubt that.

Here is a quote from the source:

quote:

Around 56% of baby boomers have a traditional pension plan, making them the last generation with widespread access to defined-benefit pensions before employers largely shifted to defined-contribution models like 401(k)s.However, pension coverage varied significantly based on where they worked:Private Sector: The tail end of the boomer generation missed out on private pensions, with only about 6% of late-wave private-sector boomers having a pension plan.Public Sector: A significant portion of boomers with pensions worked for the government, military, or were highly unionized private-sector workers.Because pensions are increasingly rare for younger workers, the boomer demographic still relies heavily on these steady, monthly checks alongside Social Security and 401(k)s to fund their

We can dispute the % all day long. I really don't care. It doesn't change the fact that article may be 100% factual in its statement it in that median retirement accounts for Boomers is $200K but it is misleading in that a significant portion of the Boomers have guaranteed pensions as part of their overall retirement plan.

quote:

If fact the % of baby boomers with a pension is equal to the % of baby boomers that don't even have retirement accounts, both around 20-24%.

If I'm understanding you correctly you can't make this assumption. Just because someone has a pension doesn't mean that they don't also have an IRA or some other form of savings.

The other fallacy of the article is that it doesn't take into any consideration of savings outside of a retirement account. For example a boomer plant "baw" working at refinery ABC likely accumulated a nice chunk of stock throughout his career. If this stock is held in a brokerage account and not a retirement account then he could be receiving a nice chunk of change each quarter as a dividends distribution that would essentially be retirement income that is not accounted for in the article.

In my opinion the article is click bait with the intent to stir up others and throw fuel on the generational warfare that is quickly becoming prevalent in our society.

This post was edited on 5/30/26 at 11:21 am

Posted on 5/30/26 at 11:15 am to armytiger96

So, people aren't saving for retirement -- and are not paying their credit card bills. Yikes.

Loading Twitter/X Embed...

If tweet fails to load, click here.

Posted on 5/30/26 at 11:26 am to Bunk Moreland

It is an epidemic. One I fell trap to in my early adulthood. I have hammered to my children the practice of living below there means early in their adulthood

It is hell to reverse and for me took a stroke of lucky moves. Still shaking my head at not saving at all till my early thirties. Just now fully realizing the miracle of compounding.

It is hell to reverse and for me took a stroke of lucky moves. Still shaking my head at not saving at all till my early thirties. Just now fully realizing the miracle of compounding.

Posted on 5/30/26 at 11:57 am to Slippy

It’s weird but also how many never worked at all ?

That’s a big number too and growing daily

So many takers who contribute nothing but more dependents on the entire system

That’s a big number too and growing daily

So many takers who contribute nothing but more dependents on the entire system

Posted on 5/30/26 at 12:15 pm to greenbean

quote:You work for 45 years and have enough money to coast the rest of your life and someone (who, as a potential heir, has a vested interest in you dying with the most possible assets) tells you that you “should” keep on working.

My mother (91) and MIL (early 80s) are in that exact position today. Both "retired" in their 60s, but had plenty of fuel in the tank, should kept on working.

Hmmm…

If you mean that they retired and went home and sat on the couch for 14 hours a day watching TV, then you should state that they made poor lifestyle choices in their retirement.

That’s understandable.

This post was edited on 5/30/26 at 12:17 pm

Page 14 of 16

Page 14 of 16

Popular

Back to top