- My Forums

- Tiger Rant

- LSU Recruiting

- SEC Rant

- Saints Talk

- Pelicans Talk

- More Sports Board

- Fantasy Sports

- Golf Board

- Soccer Board

- O-T Lounge

- Tech Board

- Home/Garden Board

- Outdoor Board

- Health/Fitness Board

- Movie/TV Board

- Book Board

- Music Board

- Political Talk

- Money Talk

- Fark Board

- Gaming Board

- Travel Board

- Food/Drink Board

- Ticket Exchange

- TD Help Board

Customize My Forums- View All Forums

- Show Left Links

- Topic Sort Options

- Trending Topics

- Recent Topics

- Active Topics

Started By

Message

Would you carry a mortgage if you didn't have to?

Posted on 6/5/18 at 7:06 am

Posted on 6/5/18 at 7:06 am

My current home is paid for. We have signed a contract with a builder, and are going to build a new home starting this summer. The new home will cost me about $100-150K more than my current home will sell for I am pretty sure.

I'm trying to decide if carrying a mortgage for that difference is the right move, or take some Roth contributions out to cover it, and not have a mortgage at all. I really hate the idea of paying interest, even if I did a 15 year loan and paid it off in 5 years, it would still cost me about 15K in interest or so.

The other oddity is that I'm going to have to build, then move, then sell, then apply funds, so I will have to get a mortgage for the entire amount initially till I sell, then I can decide to either just put down the selling amount of my current home, or that plus money to zero out my mortgage.

It all comes down to me not having a mortgage now, and hating the idea of paying even a dime extra in interest. But I do understand that anything I pull out of Roth will lower my balance and future returns.

Just trying to weigh out which is the better move. If it matters, I'm trying to retire in about 3 years as well. Thoughts?

I'm trying to decide if carrying a mortgage for that difference is the right move, or take some Roth contributions out to cover it, and not have a mortgage at all. I really hate the idea of paying interest, even if I did a 15 year loan and paid it off in 5 years, it would still cost me about 15K in interest or so.

The other oddity is that I'm going to have to build, then move, then sell, then apply funds, so I will have to get a mortgage for the entire amount initially till I sell, then I can decide to either just put down the selling amount of my current home, or that plus money to zero out my mortgage.

It all comes down to me not having a mortgage now, and hating the idea of paying even a dime extra in interest. But I do understand that anything I pull out of Roth will lower my balance and future returns.

Just trying to weigh out which is the better move. If it matters, I'm trying to retire in about 3 years as well. Thoughts?

11

11

Posted on 6/5/18 at 7:25 am to kywildcatfanone

Depends on the length of the note and the interest rate. If the rate is low enough, absolutely I'd have one.

My current mortgage is 3.25% for 30 years. With the tax deduction my rate is really only about 2.5%, which is only just above inflation, so I wish I had a bigger note than I do.

But if I had to borrow at 10% like my parents did then I'd pay that off with the quickness.

My current mortgage is 3.25% for 30 years. With the tax deduction my rate is really only about 2.5%, which is only just above inflation, so I wish I had a bigger note than I do.

But if I had to borrow at 10% like my parents did then I'd pay that off with the quickness.

Posted on 6/5/18 at 7:35 am to kywildcatfanone

I hate a mortgage note as much as the next guy and believe that even if it is not the financially savoy thing to do (as long as it is somewhat close) that peace of mind means a lot and it is enjoyable not having a note, as for taxes , remember the standard deduction goes up this year so unless you have a lot of deductions the interest may not even be in play. All that said, I would never withdraw from a ROTH or other IRA to pay down a mortgage

Posted on 6/5/18 at 7:36 am to kywildcatfanone

I wouldn't take money out of a Roth, if you have it elsewhere maybe.

I don't like debt either, but taking out $100k from a Roth that would be worth $150k possibly in 5 years in order to save $15k just isn't good math.

Especially as said with mortgage rates still historically low.

But honestly, it sounds like you have a good net worth so I'd do what makes you sleep better.

I don't like debt either, but taking out $100k from a Roth that would be worth $150k possibly in 5 years in order to save $15k just isn't good math.

Especially as said with mortgage rates still historically low.

But honestly, it sounds like you have a good net worth so I'd do what makes you sleep better.

Posted on 6/5/18 at 7:52 am to kywildcatfanone

quote:

I'm trying to decide if carrying a mortgage for that difference is the right move, or take some Roth contributions out to cover it, and not have a mortgage at all.

I'm against debt as much as the next guy, but I'm not sure about taking out Roth to avoid a mortgage.

quote:

I really hate the idea of paying interest

I would look at your balance sheet - if your Roth is outpacing what your quoted mortgage rate is going to be, even by as little as half a point, I would go ahead and take the mortgage.

quote:

The other oddity is that I'm going to have to build, then move, then sell, then apply funds, so I will have to get a mortgage for the entire amount initially till I sell

This isn't really an oddity - pretty common when someone has a lot of equity tied up in their existing house and moves.

Posted on 6/5/18 at 8:47 am to foshizzle

quote:

My current mortgage is 3.25% for 30 years. With the tax deduction my rate is really only about 2.5%, which is only just above inflation, so I wish I had a bigger note than I do.

This at rates close to that I wish someone would lend me millions. I don’t have an issue with borrowing money.

Posted on 6/5/18 at 8:58 am to baldona

quote:

Especially as said with mortgage rates still historically low.

Maybe because I haven't had a mortgage for a while, I'm not paying close enough attention.

I'm seeing a 30 year at 4.5 and a 15 at 4.25. Is that really that low?

I took out a 15 year in 2002 at 5.25 which seemed really low at the time. Is 4.5 really that low? Sorry, I'm just out of the loop.

Posted on 6/5/18 at 9:19 am to kywildcatfanone

Absolutely not

Posted on 6/5/18 at 9:24 am to kywildcatfanone

I’m with the ones that say taking out of a Roth may not be the best idea, it’s hard to find an IRA for a reason, it’s great tax savings.

And I don’t have a mortgage and do not want one, even at great rates. I was in a position where I had to pay cash for a great deal and decided to not take out the loan after the fact. I’ll save my debt for business opportunities.

You will get some guys in here saying that “peace of mind” is not something taught it finance classes but they are wrong. It’s built into risk tolerance, which is never a given in the real world.

The way I see it is my minimum cash flow is much lower than those with a substantial mortgage. It gives me the opportunity to pivot my energy if need be; my decisions aren’t affected by having to meet a $1500/month debt obligation. It’s not unlike insurance.

For instance my wife is having our second baby this year. We can pretty easily lighten both of our workloads during that time because we don’t have any debt at the moment.

All that said I am not averse to having a mortgage, and will wish I had a cheap one when we eventually upgrade our house.

And I don’t have a mortgage and do not want one, even at great rates. I was in a position where I had to pay cash for a great deal and decided to not take out the loan after the fact. I’ll save my debt for business opportunities.

You will get some guys in here saying that “peace of mind” is not something taught it finance classes but they are wrong. It’s built into risk tolerance, which is never a given in the real world.

The way I see it is my minimum cash flow is much lower than those with a substantial mortgage. It gives me the opportunity to pivot my energy if need be; my decisions aren’t affected by having to meet a $1500/month debt obligation. It’s not unlike insurance.

For instance my wife is having our second baby this year. We can pretty easily lighten both of our workloads during that time because we don’t have any debt at the moment.

All that said I am not averse to having a mortgage, and will wish I had a cheap one when we eventually upgrade our house.

Posted on 6/5/18 at 9:25 am to kywildcatfanone

quote:

I'm seeing a 30 year at 4.5 and a 15 at 4.25. Is that really that low?

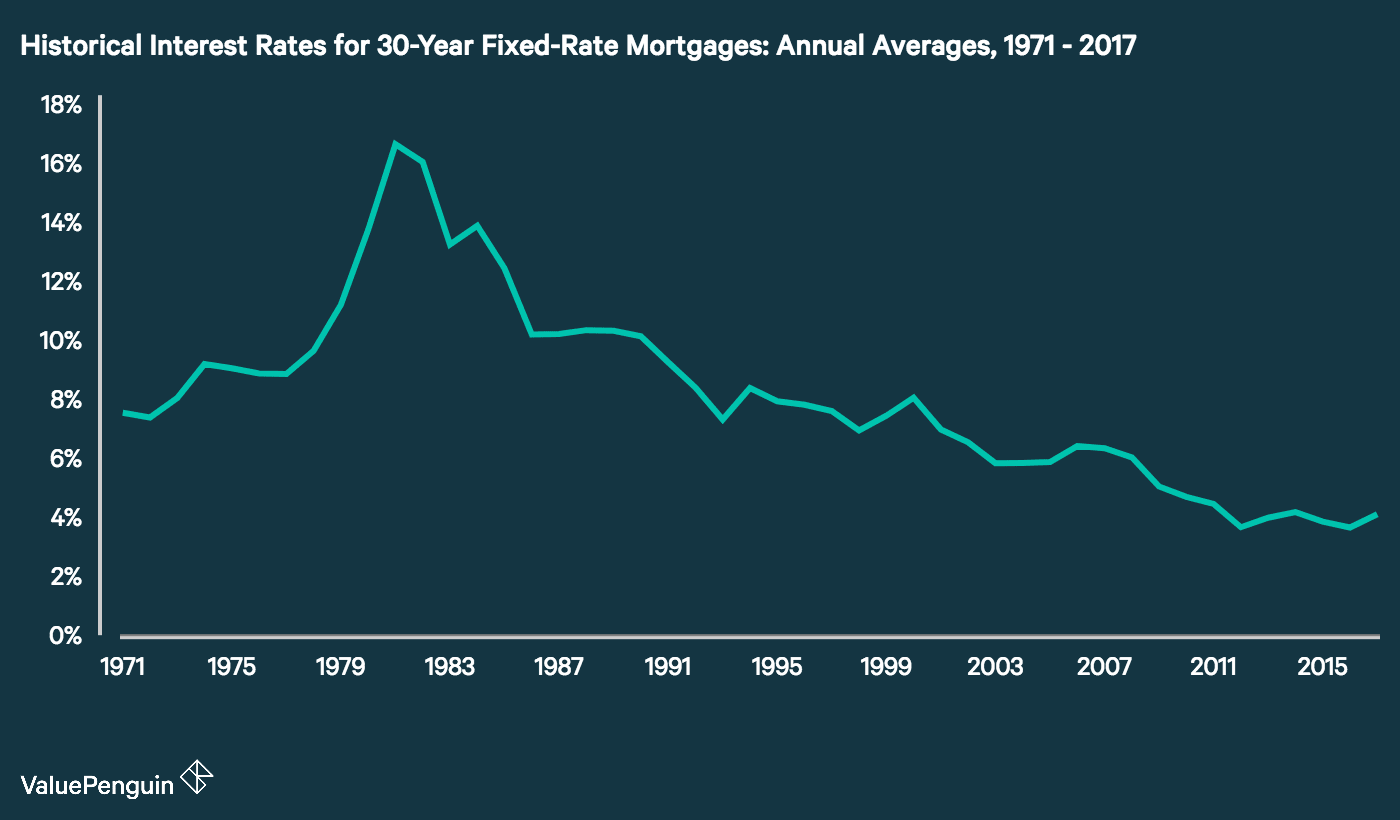

In 2000, 30 year rates were at 8%. In 1990, rates were at 10%. In 1981, rates peaked at 18%.

The last few years, rates have averaged around 4% or less.

So yes in our lifetime, rates are still historically low.

https://www.valuepenguin.com/mortgages/historical-mortgage-rates#nogo

This post was edited on 6/5/18 at 9:26 am

Posted on 6/5/18 at 10:10 am to kywildcatfanone

Sounds like you're going to be able to put a lot down on your house. No way you should take money from retirement. You'll be able to find a great interest rate putting down as much as you will be. If you're worried about the interest expense try a 15 year mortgage. much better rates and paying it off faster will decrease interest payments.

Posted on 6/5/18 at 10:24 am to SouthOfSouth

15 year makes a lot of sense in this situation for sure

Posted on 6/5/18 at 10:50 am to SouthOfSouth

Thanks All

Yes, I will do a 15 year mortgage, and plan to pay it off in maybe 5, that's what I did last time.

As far as the rates, I guess I was hoping that low rates were in the 3's, but I guess it's low 4's at the moment. But then again, I won't be getting this mortgage till sometime next year, so I hope they stay somewhat low.

Yes, I will do a 15 year mortgage, and plan to pay it off in maybe 5, that's what I did last time.

As far as the rates, I guess I was hoping that low rates were in the 3's, but I guess it's low 4's at the moment. But then again, I won't be getting this mortgage till sometime next year, so I hope they stay somewhat low.

Posted on 6/5/18 at 10:59 am to kywildcatfanone

Rates in the 4's is still a steal. Once it starts heading towards 6 and above is when it's getting tough to swallow. The fact it got below 4 at any point is unbelievable to me.

Posted on 6/5/18 at 11:06 am to kywildcatfanone

I wouldn't tap a retirement vehicle to avoid a manageable mortgage payment. The retirement money will be there if something changes and you can utilize it in the most effective manner.

As for the mortgage, you may want to ask about an ARM. I'm not familiar with current rates, but you can possibly get a lower rate. The fact you have the money to pay off the mortgage eliminates the risk associated with the potential for increasing future rates.

As for the mortgage, you may want to ask about an ARM. I'm not familiar with current rates, but you can possibly get a lower rate. The fact you have the money to pay off the mortgage eliminates the risk associated with the potential for increasing future rates.

This post was edited on 6/5/18 at 12:17 pm

Posted on 6/5/18 at 12:11 pm to OceanMan

quote:

You will get some guys in here saying that “peace of mind” is not something taught it finance classes but they are wrong. It’s built into risk tolerance, which is never a given in the real world.

The min/maxxers inexplicably value housing at $0, too. Mind boggling. I'm all for making a buck off "the man" - but to pretend that eliminating housing costs (which is what happens when you retire your mortgage)is somehow worth $0 per month is just batty, IMHO.

Posted on 6/5/18 at 1:09 pm to Ace Midnight

I like HELOC.

You only pay interest on what you need at that moment (great for new construction).

As you pay it down, you have a great resource to dip into if needed (i.e. you won't ever have to ask about taking funds from a roth).

In order to take advantage of a down market, you need funds not in the market to do the buying. That is where the HELOC is golden. Imagine having $150,000 back in 2008 to invest after the crash. HELOC

You only pay interest on what you need at that moment (great for new construction).

As you pay it down, you have a great resource to dip into if needed (i.e. you won't ever have to ask about taking funds from a roth).

In order to take advantage of a down market, you need funds not in the market to do the buying. That is where the HELOC is golden. Imagine having $150,000 back in 2008 to invest after the crash. HELOC

Posted on 6/5/18 at 1:19 pm to meansonny

quote:

Imagine having $150,000 back in 2008 to invest after the crash. HELOC

or

Imagine having the balls to borrow 150K in 2008 after the market crash, and not knowing what direction it was going, and investing in the market

Posted on 6/5/18 at 1:27 pm to kywildcatfanone

I'd be hesitant to take out anything out of my retirement accounts to avoid a mortgage. What kind of penalty is it going to cost you to take money out your retirement and also how much lost gains on that money? At least with the mortgage you can still have the tax deduction on mortgage interest to help.

Posted on 6/5/18 at 1:49 pm to kywildcatfanone

having a forced escrow is nice

rates have been generally low for the past 8 years not to have had a mortgage.

interest is deductible

rates have been generally low for the past 8 years not to have had a mortgage.

interest is deductible

Page 1 of 2

Page 1 of 2

Popular

Back to top