- My Forums

- Tiger Rant

- LSU Recruiting

- SEC Rant

- Saints Talk

- Pelicans Talk

- More Sports Board

- Fantasy Sports

- Golf Board

- Soccer Board

- O-T Lounge

- Tech Board

- Home/Garden Board

- Outdoor Board

- Health/Fitness Board

- Movie/TV Board

- Book Board

- Music Board

- Political Talk

- Money Talk

- Fark Board

- Gaming Board

- Travel Board

- Food/Drink Board

- Ticket Exchange

- TD Help Board

Customize My Forums- View All Forums

- Show Left Links

- Topic Sort Options

- Trending Topics

- Recent Topics

- Active Topics

Started By

Message

re: Remainder Of Mortgage - Which Path To Take?

Posted on 7/1/23 at 6:55 pm to lynxcat

Posted on 7/1/23 at 6:55 pm to lynxcat

quote:

. I cannot comprehend the obsession with “it feels so good”…

I can't comprehend wasting money on luxury vehicles, dining out, name brand clothes etc. I can use that to legitimately build more wealth. Ultimately, we all choose what luxuries we want. If you want to call being debt free a luxury, then fine, it makes me money.

0

0

Posted on 7/2/23 at 1:20 pm to TimeAndTide

It depends on the opportunity cost of the extra money. What would you do with it? On that low of a mortgage balance with a 4.5 rate, I would consider stopping the extra payments as long as you use the money to make more money. There are a number of options available to do this.

Having said that, if the peace of mind for paying it off is strong, then do what gives you peace. I personally have a small mortgage that could have been paid off anytime I wanted. It doesn't stress me and I invest the money.

Having said that, if the peace of mind for paying it off is strong, then do what gives you peace. I personally have a small mortgage that could have been paid off anytime I wanted. It doesn't stress me and I invest the money.

Posted on 7/2/23 at 3:46 pm to KWL85

quote:

It depends on the opportunity cost of the extra money. What would you do with it? On that low of a mortgage balance with a 4.5 rate, I would consider stopping the extra payments as long as you use the money to make more money. There are a number of options available to do this. Having said that, if the peace of mind for paying it off is strong, then do what gives you peace. I personally have a small mortgage that could have been paid off anytime I wanted. It doesn't stress me and I invest the money.

When you say extra money, do you mean the extra $200 I'm planning to dedicate to something each month from now on, or if I were to reduce the double payment I'm making each time?

You're right, the peace of mind thing does affect me, and what I also think about is how if I'm going to perhaps be in another house in say, 4 years, I really like the idea of clearing 100% (so to speak) when selling it.

That's why I'm thinking, keep on trucking with the double payment, and also take that $200 to just put into the APY savings each month. I have some stocks/mutual funds already, but I really don't think it's the most wonderful time to be gambling with extra money on that stuff.

So more or less, having a mix of both worlds, if that makes sense?

This post was edited on 7/2/23 at 3:50 pm

Posted on 7/4/23 at 3:52 pm to TimeAndTide

I meant both, but same is true of just the $200. At 4.5% on a relatively small balance, the technical answer is that you will come out ahead financially if you net (after tax) more than 4.5% by investing the extra money.

That doesn't mean you are wrong with what you are doing. Having low debt has value. It's value to you is important. You are giving your options thoughtful consideration and are probably doing what is best for you.

One consideration is major purchases in your near future like the next house you mention. You have to consider what liquid assets will you have for purchases; ie down payment on the next house. No assumptions about your financial well being on my part, just having a discussion. If the extra payments keep you from having what you will need, then you could be required to buy your next house contingent upon selling your current house. This is done frequently, but has some drawbacks. Makes me think of a friend that owns a farm. He is considered "land poor" because most of his assets are tied up in his land. It causes him to borrow against his land for major purchases. There are pros and cons, but there are times where he wishes he had more liquid assets. Just something to consider. Good luck!

That doesn't mean you are wrong with what you are doing. Having low debt has value. It's value to you is important. You are giving your options thoughtful consideration and are probably doing what is best for you.

One consideration is major purchases in your near future like the next house you mention. You have to consider what liquid assets will you have for purchases; ie down payment on the next house. No assumptions about your financial well being on my part, just having a discussion. If the extra payments keep you from having what you will need, then you could be required to buy your next house contingent upon selling your current house. This is done frequently, but has some drawbacks. Makes me think of a friend that owns a farm. He is considered "land poor" because most of his assets are tied up in his land. It causes him to borrow against his land for major purchases. There are pros and cons, but there are times where he wishes he had more liquid assets. Just something to consider. Good luck!

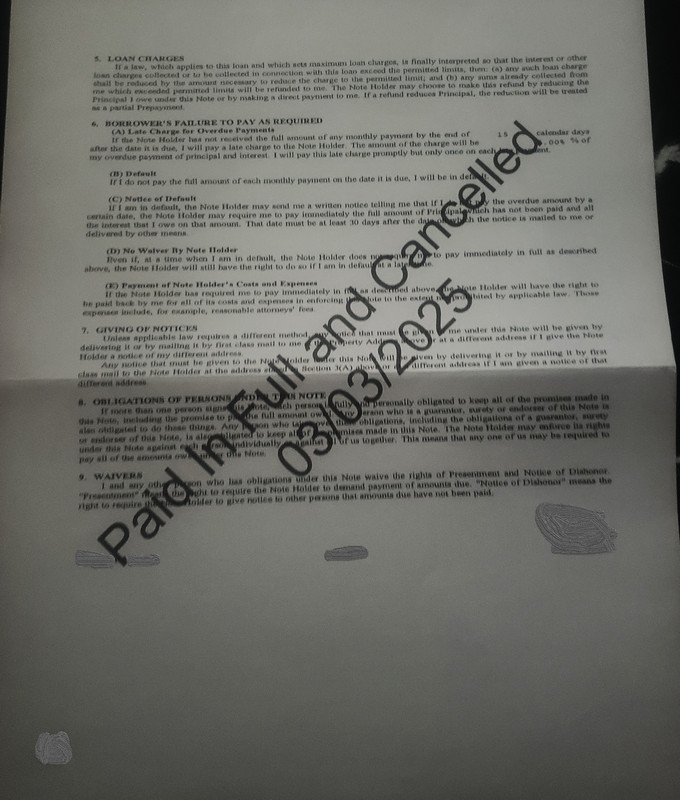

Posted on 3/24/25 at 11:04 am to KWL85

Well, this is pretty much all I have to say...

Posted on 3/24/25 at 11:43 am to TimeAndTide

quote:

Well, this is pretty much all I have to say...

Congratulations on all that peace of mind you have now, bet it feels a lot better than having more money

Posted on 3/24/25 at 12:40 pm to TimeAndTide

Insurance company and tax assessor would like a word.

Posted on 3/24/25 at 1:18 pm to kc8876

quote:

Congratulations on all that peace of mind you have now, bet it feels a lot better than having more money

Thanks - it'll take a little time for the surreal feeling to cool down, I'd imagine.

Posted on 3/24/25 at 2:14 pm to kc8876

quote:

Congratulations on all that peace of mind you have now, bet it feels a lot better than having more money

Do you drive a 1993 or a 1995 Honda Civic?

Posted on 3/25/25 at 8:55 am to TimeAndTide

I’ve never been highly incentivized to pay off low interest debt, but in some cases my perspective has changed.

For the properties I own in South Florida, I would pay them off just to cancel my wind insurance policies. After tripling the last 4-5 years I no longer see the value in them. I’d keep the flood for resale reasons.

For the properties I own in South Florida, I would pay them off just to cancel my wind insurance policies. After tripling the last 4-5 years I no longer see the value in them. I’d keep the flood for resale reasons.

Posted on 3/25/25 at 10:08 am to TimeAndTide

Interest rate is strong so I would invest that 200$ a month into VOO for the next 2.5 years. I would stay the course you are on, no need in sprinting in the last 10 yards of the race.

Posted on 3/25/25 at 3:17 pm to TimeAndTide

quote:Epic bump! Looks like you went for the no-early-payoff option?

TimeAndTide

Posted on 3/26/25 at 10:04 am to Big Scrub TX

quote:

Epic bump! Looks like you went for the no-early-payoff option?

For the most part, that's true. A while back, I decided that March would be the time, not for some special reason, but that's what seemed right, so I committed to that.

Posted on 3/26/25 at 10:32 am to TimeAndTide

quote:

For the most part, that's true. A while back, I decided that March would be the time, not for some special reason, but that's what seemed right, so I committed to that.

People really underestimate the value that creating goals and hitting goals provides in life. Good for you.

Posted on 3/26/25 at 10:40 am to notsince98

quote:

People really underestimate the value that creating goals and hitting goals provides in life. Good for you.

Nice way to put it, and much appreciated.

Page 3 of 3

Page 3 of 3

Popular

Back to top