- My Forums

- Tiger Rant

- LSU Recruiting

- SEC Rant

- Saints Talk

- Pelicans Talk

- More Sports Board

- Fantasy Sports

- Golf Board

- Soccer Board

- O-T Lounge

- Tech Board

- Home/Garden Board

- Outdoor Board

- Health/Fitness Board

- Movie/TV Board

- Book Board

- Music Board

- Political Talk

- Money Talk

- Fark Board

- Gaming Board

- Travel Board

- Food/Drink Board

- Ticket Exchange

- TD Help Board

Customize My Forums- View All Forums

- Show Left Links

- Topic Sort Options

- Trending Topics

- Recent Topics

- Active Topics

Started By

Message

0

0

Posted on 5/24/24 at 7:08 pm to BabyTac

I don’t understand mine is 775. I owe on a truck about $15,000. And our mortgage about $275,000.

Posted on 5/24/24 at 7:19 pm to Gorilla Ball

quote:

I don’t understand mine is 775. I owe on a truck about $15,000. And our mortgage about $275,000

Those should both help your score as long as you aren't missing any payments.

What is your age of credit history (years?), payment history (100%?), utilization( Less than 10%?) , number of inquires/new accounts?. This is the stuff that matters.

Posted on 5/24/24 at 7:28 pm to BabyTac

quote:

I’m guessing the score is meant to lean towards information to maximize the lender’s experience:

No.

The score is a probability index that you will go 90 days past due on credit in the future (I forget how far into the future it is forecasting, but my guess would be 2 years).

What most people don't understand are the different types of scores and different types of scorecards.

A mortgage score is different than a consumer credit score is different from a bank checking/savings account is different from an insurance score.

And there are about 8 different scorecards for a mortgage score.

It is how someone with light credit who is young could potentially have a higher score than someone who is older and never has been late but has lots of use on the credit cards.

Posted on 5/24/24 at 7:33 pm to meansonny

High enough

Posted on 5/24/24 at 7:52 pm to NATidefan

Thanks for replying

I’m also using the app - credit karma so I’m not sure how accurate it is.

100% payment

Utilization 7%

Credit history 12 yrs 1 month - I thought it would be longer.

Number of inquiries- 2

I’m also using the app - credit karma so I’m not sure how accurate it is.

100% payment

Utilization 7%

Credit history 12 yrs 1 month - I thought it would be longer.

Number of inquiries- 2

Posted on 5/24/24 at 8:19 pm to Gorilla Ball

Hmm, all that looks pretty good, I would think it would be higher. Have you checked your credit reports to see what is on them? It will show if you have any missed payments from the past or anything bad..

annualcreditreport

annualcreditreport

This post was edited on 5/24/24 at 8:22 pm

Posted on 5/24/24 at 8:39 pm to BabyTac

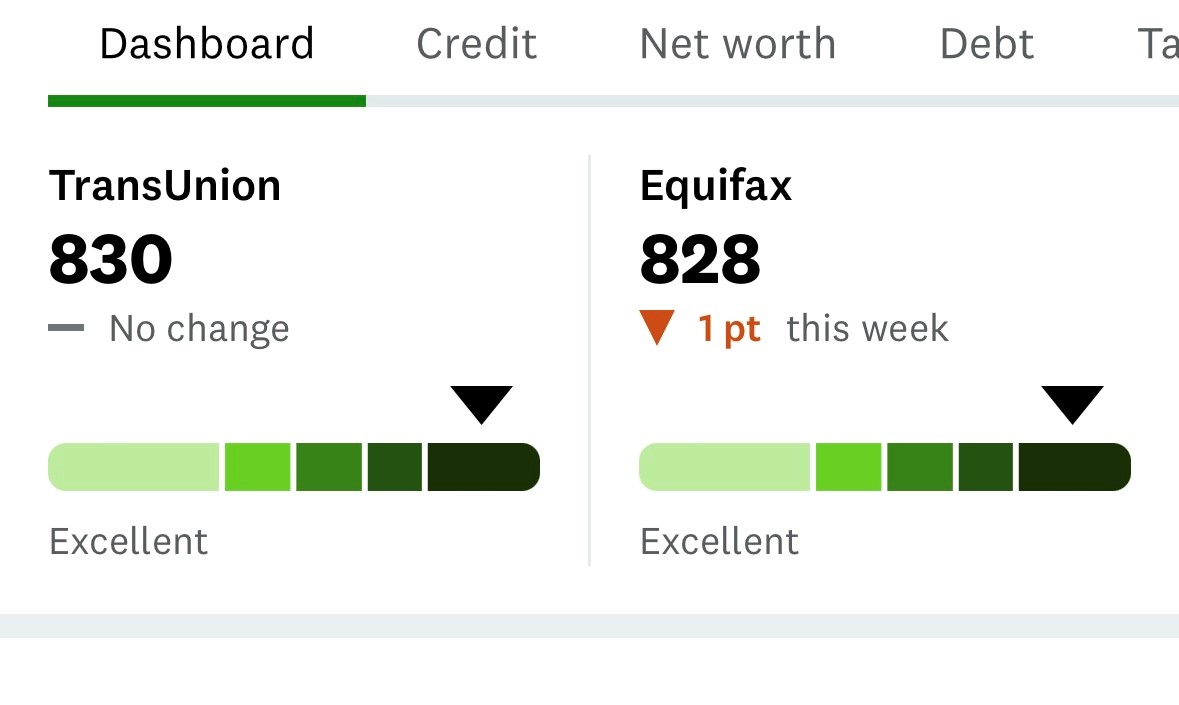

TransUnion 801

Equifax 814

FICO 825

We had a little windfall (inheritance) in March and have paid off a bunch of shite in the last two months. Was around 750 FICO before that happened.

CC Utilization is now like 4% with $36,500 across 4 cards.

Only debt we have left is 150k on our mortgage and like $4500 on wife’s vehicle.

Got denied the Chase Sapphire Reserve last week. WTF

Looks like I can call the reconsideration line when they send me the letter outlining why and state my case and probably be approved?

ETA: Funny part about the Chase thing, is they increased our business’ credit line by 60% like two days after denying the personal card.

Equifax 814

FICO 825

We had a little windfall (inheritance) in March and have paid off a bunch of shite in the last two months. Was around 750 FICO before that happened.

CC Utilization is now like 4% with $36,500 across 4 cards.

Only debt we have left is 150k on our mortgage and like $4500 on wife’s vehicle.

Got denied the Chase Sapphire Reserve last week. WTF

Looks like I can call the reconsideration line when they send me the letter outlining why and state my case and probably be approved?

ETA: Funny part about the Chase thing, is they increased our business’ credit line by 60% like two days after denying the personal card.

This post was edited on 5/24/24 at 8:41 pm

Posted on 5/24/24 at 8:49 pm to prostyleoffensetime

I saw chase has a 5/24 rule. If you only have 4 cards that shouldn't affect you though. But it basically means if you have opened 5 cards (from any issuers) in the last 24 months they won't approve you no matter what.

Chase business cards don't count towards your 5 though, they view those different.

Chase business cards don't count towards your 5 though, they view those different.

This post was edited on 5/24/24 at 8:52 pm

Posted on 5/24/24 at 8:52 pm to BabyTac

I used to run the 800s…..then I went into business for myself.

Ouch.

I have no personal debt- but I am the personal guarantor on tens of millions of dollars of LOCs.

Never been late on a payment in my life- business or otherwise, and my credit score now looks like I’m the guy they would want to try to stick an 18% interest rate to on a used car loan.

It took me a long time to accept it.

Then I started to understand that my situation is in the absolute minority and the system isn’t geared to understand.

Or maybe it is- because I can sure as hell tell you- everytime I sign a personal guarantee I think “I’d like to know how TF someone thinks I’m gonna pay for this if this ship sinks” :-)

Ouch.

I have no personal debt- but I am the personal guarantor on tens of millions of dollars of LOCs.

Never been late on a payment in my life- business or otherwise, and my credit score now looks like I’m the guy they would want to try to stick an 18% interest rate to on a used car loan.

It took me a long time to accept it.

Then I started to understand that my situation is in the absolute minority and the system isn’t geared to understand.

Or maybe it is- because I can sure as hell tell you- everytime I sign a personal guarantee I think “I’d like to know how TF someone thinks I’m gonna pay for this if this ship sinks” :-)

Posted on 5/24/24 at 8:56 pm to NATidefan

Yeah I haven’t opened a personal card in probably 7 or 8 years. I read on the Chase subreddit that they deny all the time and send a letter outlining why. You can see their reasoning and call a reconsideration line and kind of state your case and verify your financial situation and they’ll approve most of the time.

Was just floored that I was denied in less than 5 seconds after clicking submit.

Was just floored that I was denied in less than 5 seconds after clicking submit.

Posted on 5/24/24 at 9:26 pm to BabyTac

Mine would be perfect but I get negative points because I don't have a mortgage anymore

Posted on 5/24/24 at 9:34 pm to BabyTac

1 UV 39 DV poor guy

Posted on 5/25/24 at 7:45 am to NATidefan

quote:

annualcreditreport

This. Bawt a new vehicle a few years ago. At the time, Credit Karma showed three scores in low 790s. Actual score was mailed to me weeks after credit was pulled. Real score was 50 points higher than Credit Karma showed. I called and asked about this and was told that Credit Karma is a guesstimate. The report I received was accurate and that I can obtain a free report once per year at annualcreditreport.com that has the real reports and scores.

Have done that since and it’s great. Full breakdown of accounts and history. Told friends about this and one used it to dispute some negative hits. He disputed some and was able to get some removed. Said his scores went up.

This post was edited on 5/26/24 at 11:27 am

Posted on 5/25/24 at 7:55 am to BabyTac

Now that Joe Biden and the tax payers just paid off my student loans, my credit score jumped 75 points to 755. Thank you all!!

Posted on 5/25/24 at 12:03 pm to NATidefan

Thank you for sharing

Posted on 5/25/24 at 2:39 pm to BabyTac

FICO says 850.

I feel special.

I feel special.

Posted on 5/25/24 at 3:08 pm to BabyTac

Recently dropped after paying of the last $17k on my truck a couple months ago.

This post was edited on 5/26/24 at 1:21 pm

Posted on 5/26/24 at 7:48 am to Grinder

Am 15 less

Posted on 5/26/24 at 5:22 pm to NATidefan

quote:This week I submitted an lease* application, they ran a Trans-Union on my credit. It was 801.

My Equifax runs around 815-820, it was at 819 the day the TransUnion was run.

I wasn’t aware there’s that much of a disparity.

*The property is a one-of-a-kind, worth it to me to take the credit ding.

Page 3 of 4

Page 3 of 4

Popular

Back to top