- My Forums

- Tiger Rant

- LSU Recruiting

- SEC Rant

- Saints Talk

- Pelicans Talk

- More Sports Board

- Fantasy Sports

- Golf Board

- Soccer Board

- O-T Lounge

- Tech Board

- Home/Garden Board

- Outdoor Board

- Health/Fitness Board

- Movie/TV Board

- Book Board

- Music Board

- Political Talk

- Money Talk

- Fark Board

- Gaming Board

- Travel Board

- Food/Drink Board

- Ticket Exchange

- TD Help Board

Customize My Forums- View All Forums

- Show Left Links

- Topic Sort Options

- Trending Topics

- Recent Topics

- Active Topics

Started By

Message

re: Home prices up 30% because of Biden era illegal immigration

Posted on 7/6/26 at 5:50 am to SlowFlowPro

Posted on 7/6/26 at 5:50 am to SlowFlowPro

quote:

SlowFlowPro

Letting in 166% of what went through Ellis Island in its ENTIRE history in ONLY 4 years is going to have deleterious effects, don't you think?

1

1

Posted on 7/6/26 at 6:04 am to SlowFlowPro

quote:This isn't hard. The housing price increases during Bidenflation aren't debatable.... From 2023 - Early 2024 ~6–7%; Late 2024 ~4–5%.

Yes a huge spike during the free money Covid era (2020-2022). What were prices doing 2023-2024?

I know you know that, because we've discussed it several times. I (presumably like you) did not previously recognize the input of illegal immigration into that equation.

Posted on 7/6/26 at 6:07 am to RohanGonzales

quote:

Letting in 166% of what went through Ellis Island in its ENTIRE history in ONLY 4 years

There isn't any real, valid data to support that claim.

Posted on 7/6/26 at 6:08 am to Padme

Almost like capitalism is working, supply meets demand

Posted on 7/6/26 at 6:09 am to NC_Tigah

quote:

The housing price increases during Bidenflation aren't debatable.... From 2023 - Early 2024 ~6–7%; Late 2024 ~4–5%.

Yes, when Trump and Biden print trillions and lower interest rates to 0, that's going to happen (to more than housing, which we saw).

When the free money stopped and interest rates rose, housing prices fell

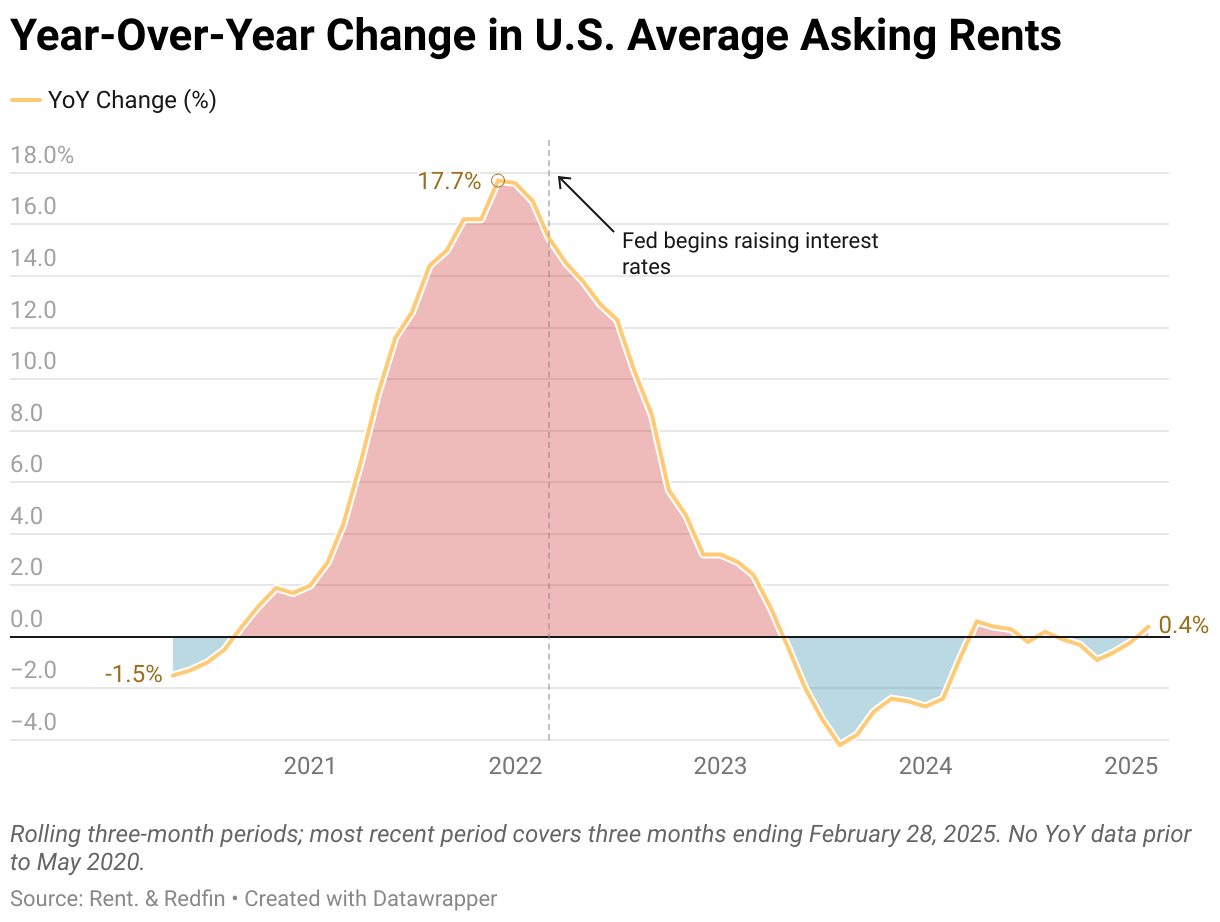

FWIW, rent is a much more applicable variable when discussing illegals, for obvious reasons.

Posted on 7/6/26 at 6:16 am to SlowFlowPro

quote:As I've repeatedly established with you, and you repeatedly forget, one of those was VERY different from the other.

Yes, when Trump and Biden print trillions

Posted on 7/6/26 at 6:22 am to NC_Tigah

You're leaving objectivity and going into partisanship by trying that argument.

Money is fungible.

The impact of a dollar printed in 2020 and 2021 is the same (well it's technically less in 2021 due to the inflation of the 2020 printing but that's hyper technical)

It's the same with borrowing dollars at near-0%

Money is fungible.

The impact of a dollar printed in 2020 and 2021 is the same (well it's technically less in 2021 due to the inflation of the 2020 printing but that's hyper technical)

It's the same with borrowing dollars at near-0%

Posted on 7/6/26 at 7:16 am to SlowFlowPro

quote:No. Sorry. We've been down this road before.

The impact of a dollar printed in 2020 and 2021 is the same

The 2020 CARES payments ($2.2 trillion) were explicitly designed as replacement income during a period when real output had collapsed and people literally could not work. The economy had a supply-side hole which fiscal transfers bridged.

The 2021 American Rescue Plan ($1.9 trillion), by contrast, arrived when the economy was already rebounding sharply (real growth accelerating toward 5.7%) and output was closing back in on its pre-pandemic trend.

As we've discussed many times, dollar for dollar, the 2021 money was considerably more inflationary than the 2020 money. In 2020, production and spending had collapsed, CARES money simply replaced income that otherwise would have disappeared. Supply-demand (after the initial toilet paper, run and mask fiasco) remained in balance.

Extra money went into personal savings, and certainly later contributed somewhat to inflation. However, the counter is that without the CARES Act, there would have been massive economic destruction, and likely a second great recession, or depression.

By contrast, the ARP threw money on top of aggregate savings accumulated during the CARES act, and did so at a time where the economy was predictably rapidly recovering. The effect was purely inflationary, and was compounded by the Biden administration's supply chain ineptitude creating a massive supply-demand imbalance ... a ton of extra money on the one hand, and a lack of supply on the other.

Drawing equivalency between those two programs, and the basis for them, is flatly ignorant.

Posted on 7/6/26 at 7:23 am to Padme

The article is dumb. No doubt Biden's policies affected home prices, but trying to tie one specific policy to a specific % of the rise in the market is dumb for many reasons. The most basic reason is the broad brush this article uses b y assuming there is a national market when RE is very area specific. As I told SFP last night, there is no national market. No company that tracks RE data does it that way outside of doing it for headlines. CoreLogic, NAR, ATTOM, etc. all track down to zip codes if you want to get real technical.

One could use the data provided by those firms and cross reference it to the data of wich areas had the largest influx of illegals and get a much more accurate idea of how badly they affected the market but that is time consuming and doesn't capture headlines.

Here is what I posted on the OT about this article in the thread there. Feel free to debate me

FYI, this is just one of the things Biden did that helped send home prices through the roof.

Another one that doesn’t get talked about enough is how long Biden kept stretching out forbearance, mortgage relief, and all the loss-mitigation stuff after COVID. He basically froze the natural cycle of the market for six years. Forbearance started under Trump during COVID and didn’t end until last year, when Trump stopped it.

Biden didn’t want a housing correction happening on his watch, so instead of letting distress actually work through the system, he just kept kicking the can down the road.

That’s why pointing to one thing and trying to say “this caused the 30% increase” is dumb. Housing bubbles don’t happen because of one policy. It’s years of bad policy, cheap money, restricted supply, government intervention, and people acting like prices can only go up all piling on top of each other.

It’s the same type of thinking from people who say I was wrong for saying the market was going to correct because I pointed this stuff out years ago on here. None of this stuff happens overnight. These cycles take years to build. Bad policy can delay the correction, but it doesn’t make it disappear.

The only question now is what Trump does to try to kick the can down the road, because he definitely will. He has Pulte of Pulte Homes as Director of the FHFA overseeing Fannie and Freddie. Pulte is going to try to keep mortgage credit flowing and keep the whole thing chugging along instead of letting the market fully reset.

And don’t forget, they also want to make Fannie and Freddie private again. That’s a big part of why they have every reason to keep kicking the can down the road. They’re not going to take them private in the middle of a correction. They need the market to look stable so the incentive is to delay the reset, not let it happen naturally.

The subprime crash happened in 2008, but the reality is that it was set in motion with the revision of the CRA in 1995. Our peak damage of the subprime crash was in 2010, and the recovery started soon after. We are about as far away from recovery now as we were from the CRA revision back then.

It’s called cycles for a reason. The bad decisions happen years before the crash, and by the time everyone finally admits there’s a problem, the correction is already baked in. Realize where we are and where I have been telling this board for around 2 years now we were heading.

One could use the data provided by those firms and cross reference it to the data of wich areas had the largest influx of illegals and get a much more accurate idea of how badly they affected the market but that is time consuming and doesn't capture headlines.

Here is what I posted on the OT about this article in the thread there. Feel free to debate me

FYI, this is just one of the things Biden did that helped send home prices through the roof.

Another one that doesn’t get talked about enough is how long Biden kept stretching out forbearance, mortgage relief, and all the loss-mitigation stuff after COVID. He basically froze the natural cycle of the market for six years. Forbearance started under Trump during COVID and didn’t end until last year, when Trump stopped it.

Biden didn’t want a housing correction happening on his watch, so instead of letting distress actually work through the system, he just kept kicking the can down the road.

That’s why pointing to one thing and trying to say “this caused the 30% increase” is dumb. Housing bubbles don’t happen because of one policy. It’s years of bad policy, cheap money, restricted supply, government intervention, and people acting like prices can only go up all piling on top of each other.

It’s the same type of thinking from people who say I was wrong for saying the market was going to correct because I pointed this stuff out years ago on here. None of this stuff happens overnight. These cycles take years to build. Bad policy can delay the correction, but it doesn’t make it disappear.

The only question now is what Trump does to try to kick the can down the road, because he definitely will. He has Pulte of Pulte Homes as Director of the FHFA overseeing Fannie and Freddie. Pulte is going to try to keep mortgage credit flowing and keep the whole thing chugging along instead of letting the market fully reset.

And don’t forget, they also want to make Fannie and Freddie private again. That’s a big part of why they have every reason to keep kicking the can down the road. They’re not going to take them private in the middle of a correction. They need the market to look stable so the incentive is to delay the reset, not let it happen naturally.

The subprime crash happened in 2008, but the reality is that it was set in motion with the revision of the CRA in 1995. Our peak damage of the subprime crash was in 2010, and the recovery started soon after. We are about as far away from recovery now as we were from the CRA revision back then.

It’s called cycles for a reason. The bad decisions happen years before the crash, and by the time everyone finally admits there’s a problem, the correction is already baked in. Realize where we are and where I have been telling this board for around 2 years now we were heading.

Posted on 7/6/26 at 7:25 am to NC_Tigah

quote:

The 2020 CARES payments ($2.2 trillion) were explicitly designed as replacement income during a period when real output had collapsed and people literally could not work. The economy had a supply-side hole which fiscal transfers bridged.

The 2021 American Rescue Plan ($1.9 trillion), by contrast, arrived when the economy was already rebounding sharply (real growth accelerating toward 5.7%) and output was closing back in on its pre-pandemic trend.

Why the dollars were printed has no bearing on this discussion.

The dollars printed are fungible. Trying to increase the impact of your team's dollars by justifying why they were printed is partisanship, not objective analysis.

And you're completely ignoring the interest rate variable, which likely had more impact than the printed dollars.

This post was edited on 7/6/26 at 7:26 am

Posted on 7/6/26 at 7:32 am to SlowFlowPro

quote:

Without those terrible policies from Trump and Biden we probably don't even notice the impact of the illegals on the market.

I disagree. The rental market would have felt the price hikes 100%, and it has.

I do agree that it took years of bad policy across multiple administrations to get where we are. Just like the subprime crash and the horrible policy after policy that preceded it. I have been telling this board for 2 years now that none of this happens overnight and none of it is due to one specific policy. They take time.

This board accused me of hoping for a 2008 crash when I have said it will be a correction and that 2008 can never happen again. That doesn't mean some areas won't see a horrible market for a while.

FL has 7% of all SFH in America yet currently accounts for 1 in 7 of all homes on the nationwide market. FL also leads the nation with1 in 2110 homes in some state of foreclosure. FL is screwed and unless insurance rates magically drop, it will be for a while.

I tried telling everyone a few years ago where we were heading. People made fun of me instead

Posted on 7/6/26 at 7:35 am to LemmyLives

quote:

Fair. But hundreds of thousands of Indians abusing H1B/F1 and other visas have an impact on prices, too

That is going to be very area-specific, where large concentrations of Indians are, like DFW, which has been happening.

Those small pockets have zero impact on me in Lake Charles.

The bad policy from administrations does impact me, though. See the difference?

Posted on 7/6/26 at 7:38 am to NC_Tigah

quote:

As I've repeatedly established with you, and you repeatedly forget, one of those was VERY different from the other.

Correct but the market doesn't care where the influx of new dollars came from or why.

quote:

As we've discussed many times, dollar for dollar, the 2021 money was considerably more inflationary than the 2020 money

That may be true, but it was inflationary nonetheless.

This post was edited on 7/6/26 at 7:40 am

Posted on 7/6/26 at 7:43 am to stout

The hot markets in the CV era increased dramatically and then have fallen dramatically. It goes beyond Florida. Austin was a gem for American immigration and it's housing market has also crashed.

I don't think we have data to look at where the most illegals have been removed, to do what you spoke of last night.

I don't think we have data to look at where the most illegals have been removed, to do what you spoke of last night.

Posted on 7/6/26 at 7:46 am to NC_Tigah

quote:

The 2020 CARES payments ($2.2 trillion) were explicitly designed as replacement income during a period when real output had collapsed and people literally could not work. The economy had a supply-side hole which fiscal transfers bridged.

The 2021 American Rescue Plan ($1.9 trillion), by contrast, arrived when the economy was already rebounding sharply (real growth accelerating toward 5.7%) and output was closing back in on its pre-pandemic trend.

Trump did an additional $900 billion in December 2020. You can add that to your $2.2 trillion.

Posted on 7/6/26 at 7:47 am to SlowFlowPro

quote:

And you're completely ignoring the interest rate variable, which likely had more impact than the printed dollars.

I'm happy to discuss "the interest rate variable". Is the reference to the Fed? Is the reference to lending rates?

Regarding the impact of dollars, the proof is in the pudding. Inflation during 2020 was virtually nonexistent with a fed rate basically at zero. It really wasn't until Q2 2021 that inflation started to pick up subsequent to the passage of the ARP, supply chain disruption, and too late Powell's stupid Fed policy.

Economists estimate that in a given hypothetical where just the CARES Act was passed, and supply chain immediately returned to pre-Covid levels in 2021, the inflation rate would have increased to between 2% and 3% by December 2021. Instead, it was 7% and climbing.

Posted on 7/6/26 at 7:49 am to frogtown

But SFP said it was the tariff and wood

Posted on 7/6/26 at 7:50 am to SlowFlowPro

quote:

Austin was a gem for American immigration and it's housing market has also crashed.

Austin was way overhyped as the next Silicon Valley during CV, and then people changed their minds after a dry, hot Texas summer. That impacted the price drops there a lot, too.

Posted on 7/6/26 at 7:50 am to SDVTiger

quote:

But SFP said it was the tariff and wood

wut

Posted on 7/6/26 at 7:52 am to SlowFlowPro

quote:

Without those terrible policies from Trump and Biden we probably don't even notice the impact of the illegals

You found the silver lining.

Had they remained unnoticed there may not have been as much impetus to rid ourselves of them.

Page 2 of 3

Page 2 of 3

Popular

Back to top