- My Forums

- Tiger Rant

- LSU Recruiting

- SEC Rant

- Saints Talk

- Pelicans Talk

- More Sports Board

- Coaching Changes

- Fantasy Sports

- Golf Board

- Soccer Board

- O-T Lounge

- Tech Board

- Home/Garden Board

- Outdoor Board

- Health/Fitness Board

- Movie/TV Board

- Book Board

- Music Board

- Political Talk

- Money Talk

- Fark Board

- Gaming Board

- Travel Board

- Food/Drink Board

- Ticket Exchange

- TD Help Board

Customize My Forums- View All Forums

- Show Left Links

- Topic Sort Options

- Trending Topics

- Recent Topics

- Active Topics

Started By

Message

re: Retirement goal and how to get there: looking for advice / opinions

Posted on 7/7/25 at 12:54 pm to NC_Tigah

Posted on 7/7/25 at 12:54 pm to NC_Tigah

It's very conservative. Show your math.

The historical return of VOO, for example, is 13.4%. Given that average one could still easily take out 6% and still be growing their money.

The historical return of VOO, for example, is 13.4%. Given that average one could still easily take out 6% and still be growing their money.

2

2

Posted on 7/7/25 at 1:08 pm to VABuckeye

We've also been in a bull market for the better part of 16 years. I don't know if it would be prudent to expect those types of returns for the next 16 in retirement.

Posted on 7/7/25 at 1:17 pm to fallguy_1978

No disagreement here but the 4% rule is from 1994. It just might be time to look at statistics and make an adjustment rather than just saying "negative". Not to you but show the math. Since the rule was proposed (it's a guideline, not a rule) that market has averaged 9% despite some bad years.

30 year average is a decent basis to debunk the rule.

30 year average is a decent basis to debunk the rule.

Posted on 7/7/25 at 1:18 pm to xBirdx

quote:

Hoping those expenses would be lower by retirement age…. No way would I retire with $6500/mth debt….

What all bills we talking?

Healthcare, utilities, food, country club, vehicle maintenance, maybe a small mortgage payment < $1k.

We will use $340k-ish equity in current home and downsize in a new home. Someone else said ~$7k is conservative. I need to do more research on expected monthly costs in retirement.

This post was edited on 7/7/25 at 1:21 pm

Posted on 7/7/25 at 1:26 pm to VABuckeye

quote:VOO simply tracks the S&P and was formed at a market nadir in 2010. Had it been formed 10yrs earlier, its historical return would be 5.4%.

The historical return of VOO, for example, is 13.4%

Look, I'm not trying to be a "nattering nabob of negativism." If we were talking about someone in their 40's instead of late 50's, this would be a different conversation. But we aren't, so it isn't.

The OP may be inexperienced enough to take your VOO historical return as a forward looking performance assumption, rather than buckling down on current finances, and pushing resultant savings into a portfolio.

Is it possible though that putting everything in VOO could yield 16%/yr x 7yrs w/o any major pullbacks? Sure. It's definitely possible.

This post was edited on 7/7/25 at 1:27 pm

Posted on 7/7/25 at 1:26 pm to Naked Bootleg

quote:

I need to do more research on expected monthly costs in retirement

I've done a lot of research on this. #1 is probably what state you will live in as quite a few states are tax beneficial to retirees (Georgia really hits its' stride after you turn 65).

Focus on tax burden first as other than medical expenses it can be the biggest cash outflow unless you have a mortgage.

Calculator.net has excellent calculators you can play around with for various investments, retirement payouts, etc.

Posted on 7/7/25 at 1:28 pm to NC_Tigah

Fair enough and no offense taken at all. It's a discussion more people need to have and research. Other than the occassional trolls I greatly appreciate the input of those that frequent this board.

This post was edited on 7/7/25 at 1:31 pm

Posted on 7/7/25 at 1:31 pm to Naked Bootleg

Just seems high to me, but idk.

Im estimating my expenses right now ( inflation, I know) to be like $4k all in on the high side

1 auto loan (hopefully not but farrowing in, utilities, food, normal entertainment, eating out, insurance, taxes on home)

Im estimating my expenses right now ( inflation, I know) to be like $4k all in on the high side

1 auto loan (hopefully not but farrowing in, utilities, food, normal entertainment, eating out, insurance, taxes on home)

Posted on 7/7/25 at 1:32 pm to VABuckeye

So what’s the updated rule of thumb?

Posted on 7/7/25 at 1:34 pm to VABuckeye

quote:

VABuckeye

Thank you.

We've been looking at eastern Tennessee (Chatt; Johnson City) but northern Georgia interests us too.

Upon quick look, I see what you mean re: Georgia.

quote:

Georgia does not tax Social Security retirement benefits and provides a maximum deduction of $65,000 per person on all types of retirement income for anyone 65 or older. The state’s sales tax rates and property tax rates are both relatively moderate. Georgia has no inheritance or estate taxes.

smartasset.com

Posted on 7/7/25 at 1:43 pm to xBirdx

quote:

So what’s the updated rule of thumb?

Depends on your tolerance, right? For me, I think 6% won't be a problem.

Posted on 7/7/25 at 1:54 pm to Naked Bootleg

6-7k a month is insane in retirement. To put it in perspective I am 40 and when I retire the only bill besides utilities I will have is property tax. I am also expecting to have 20kish a month coming in combined me and my wife.

Posted on 7/7/25 at 2:01 pm to NC_Tigah

quote:

There is a reason for the standard disclaimer: "Past performance does not guarantee future results."

And that would be exactly why I posted that same exact sentence in my post. Thanks for repeating it.

quote:

E.g., QQQ 10-Year Annualized Return March 2000–March 2010 was negative @ –5.3% per year! You're doing well to point out the rosey assumptions I addressed.

The S&P returned -14.4% from 2000-2010.

If you want to cherry pick a time frame that includes The 2000-2002 and 2008 crashes as your base model we should conclude that everyone will lose at least 5% of their investments, correct?

QQQ's 20 year return is 14.17%. That's pretty stable and it's not even an ETF that I love. Should you coun't on a pullback? Sure. Should you model in the two biggest crashes of the last 35 years? Probably not.

This post was edited on 7/7/25 at 2:10 pm

Posted on 7/7/25 at 2:02 pm to VABuckeye

Yea.. hoping least as possible lol

I think I can work with 4%, as I’ll have a couple hundred k in cash as well

I think I can work with 4%, as I’ll have a couple hundred k in cash as well

Posted on 7/7/25 at 2:12 pm to RolltidePA

quote:Au contraire. The question is, looking forward, what actually are the cherries being picked? E.g., In midst of the dot.com boom, one might not have had a decade of negative market performance on their radar screen.

If you want to cherry pick a time frame

quote:Oooh cuz, you have no idea how dumb you'd feel IRL making that statement

If you think that ETFs are high risk, maybe the market isn't the place for your money.

Maybe take your sassy sauce to another board.

Posted on 7/7/25 at 2:19 pm to Naked Bootleg

I just retired in February. Recommendations:

Eliminate or reduce debt, as much as possible.

Have a plan for medical coverage before 65.

4% rule is outstanding.

Your investments may track the last 17 or so years, or we may have another October '87, 1999, or housing crisis. Interest rates will impact you more in retirement because you'll want to be more conservative with investments.

Have emergency funds: You never know when the roof needs repair, the A/C goes out, a car repair or replacement is needed.

Understand what you like to do with your time: trips can cost money, but some are very inexpensive. Eating out costs. Will your habits change?

I started looked at expense ratios for funds like Fidelity Contra. I also noticed that a lot of funds/ETFs were invested in Netflix/AMZN/GOOG/MSFT/NVIDIA, etc and started looking elsewhere.

Eliminate or reduce debt, as much as possible.

Have a plan for medical coverage before 65.

4% rule is outstanding.

Your investments may track the last 17 or so years, or we may have another October '87, 1999, or housing crisis. Interest rates will impact you more in retirement because you'll want to be more conservative with investments.

Have emergency funds: You never know when the roof needs repair, the A/C goes out, a car repair or replacement is needed.

Understand what you like to do with your time: trips can cost money, but some are very inexpensive. Eating out costs. Will your habits change?

I started looked at expense ratios for funds like Fidelity Contra. I also noticed that a lot of funds/ETFs were invested in Netflix/AMZN/GOOG/MSFT/NVIDIA, etc and started looking elsewhere.

Posted on 7/7/25 at 2:28 pm to xBirdx

Updated rule of thumb according to Bengen's research and model is 4.7%

Some of you aren't accounting for sequence of returns risk. If market is down in first years of retirement withdrwals you rapidly deplete nest egg.

Also seem to be falling for recency bias assuming returns will keep up w current tend not hold to historic norms. If anything, recent positive trend and high stock valuations by P/E etc. may be be more likely to portend a higher likelihood of market correction.

Thus 6% is a higher risk withdrwal rate than typically reccomended.

Some of you aren't accounting for sequence of returns risk. If market is down in first years of retirement withdrwals you rapidly deplete nest egg.

Also seem to be falling for recency bias assuming returns will keep up w current tend not hold to historic norms. If anything, recent positive trend and high stock valuations by P/E etc. may be be more likely to portend a higher likelihood of market correction.

Thus 6% is a higher risk withdrwal rate than typically reccomended.

This post was edited on 7/7/25 at 2:46 pm

Posted on 7/7/25 at 2:38 pm to NC_Tigah

quote:

Au contraire. The question is, looking forward, what actually are the cherries being picked? E.g., In midst of the dot.com boom, one might not have had a decade of negative market performance on their radar screen.

Serious question, what is your recommendation then? If you are in the market you assume risk, that's part of the game. Looking forward, where's your money going if you want/need to turnover percentage for the next 7-10 years. Include all the doom and gloom that you'd like.

Snarkiness aside, I am open to the education.

Posted on 7/7/25 at 2:47 pm to tigerbacon

quote:

6-7k a month is insane in retirement. To put it in perspective I am 40 and when I retire the only bill besides utilities I will have is property tax. I am also expecting to have 20kish a month coming in combined me and my wife.

I listed "vehicle maintenance" - OT Ballers' 40 foot yachts don't maintain themselves, baw (kidding)

I am estimating how much we'd pay for healthcare.

How much should I expect to pay for me & wife's health/vision/dental?

eta: question to all; not tigerbacon

This post was edited on 7/7/25 at 2:53 pm

Posted on 7/7/25 at 3:02 pm to Naked Bootleg

quote:

I'm not well-versed, but I don't like the idea of hiring a money manager.

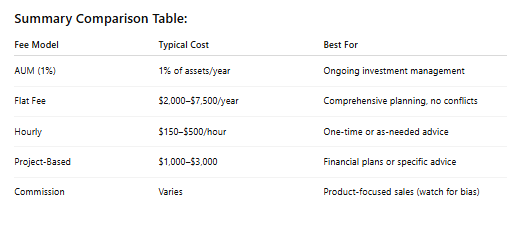

At age 56 it is not a bad idea. There is a lot of smart people here, some are even financial advisors themselves, at the end of the day there is peace of mind sitting down with someone with paper in front of you and charting out the rest of your life. It is not cheap, but it is also not overly expensive

We did a financial advisor a couple of years ago and I personally feel more confident of our end game now being successful.

Page 2 of 5

Page 2 of 5

Popular

Back to top