- My Forums

- Tiger Rant

- LSU Recruiting

- SEC Rant

- Saints Talk

- Pelicans Talk

- More Sports Board

- Fantasy Sports

- Golf Board

- Soccer Board

- O-T Lounge

- Tech Board

- Home/Garden Board

- Outdoor Board

- Health/Fitness Board

- Movie/TV Board

- Book Board

- Music Board

- Political Talk

- Money Talk

- Fark Board

- Gaming Board

- Travel Board

- Food/Drink Board

- Ticket Exchange

- TD Help Board

Customize My Forums- View All Forums

- Show Left Links

- Topic Sort Options

- Trending Topics

- Recent Topics

- Active Topics

Started By

Message

re: Discussion of Fed Liquidity’s Impact on Equity Markets

Posted on 8/11/20 at 9:28 pm to RedStickBR

Posted on 8/11/20 at 9:28 pm to RedStickBR

What he said about the 70s, I've never thought about. I'll have to dig back the past twenty years to see why from 11-13 either taxes or inflation were so high. I don't remember that at all.

Timing looks like sovereign debt crisis

Timing looks like sovereign debt crisis

This post was edited on 8/11/20 at 9:29 pm

1

1

Posted on 8/13/20 at 4:00 pm to wutangfinancial

Posted on 8/14/20 at 8:49 am to RedStickBR

LINK

For Q2 2020, the average equity fund and taxable fixed income fund posted a 20.22% and 5.45% return, respectively, which contributed to the big rise in assets under management.

TNA in the conventional funds business rose 13.45%, climbing $2.571 trillion from Q1 2020 to just a little less than $21.685 trillion for Q2 2020.

Once again, the money market funds (+$302.7 billion) macro-group had the largest draw of net new money for Q2, while the developed international markets funds (-$40.6 billion) macro-group witnessed the largest net redemptions.

TNA in U.S. ETPs increased 19.16% (+$703 billion) from $3.672 trillion for Q1 to slightly more than $4.375 trillion for Q2 2020.

The long-term taxable bond ETPs (+$44.7 billion) macro-group had the largest draw of net new money for Q2 of all the ETP macro-groups, while the U.S. diversified equity ETPs (-$12.6 billion) macro-group witnessed the largest net redemptions.

For Q2, actively managed funds—excluding money market funds—took in some $25.7 billion net, while their passively managed counterparts attracted some $88.5 billion.

For Q2 2020, the average equity fund and taxable fixed income fund posted a 20.22% and 5.45% return, respectively, which contributed to the big rise in assets under management.

TNA in the conventional funds business rose 13.45%, climbing $2.571 trillion from Q1 2020 to just a little less than $21.685 trillion for Q2 2020.

Once again, the money market funds (+$302.7 billion) macro-group had the largest draw of net new money for Q2, while the developed international markets funds (-$40.6 billion) macro-group witnessed the largest net redemptions.

TNA in U.S. ETPs increased 19.16% (+$703 billion) from $3.672 trillion for Q1 to slightly more than $4.375 trillion for Q2 2020.

The long-term taxable bond ETPs (+$44.7 billion) macro-group had the largest draw of net new money for Q2 of all the ETP macro-groups, while the U.S. diversified equity ETPs (-$12.6 billion) macro-group witnessed the largest net redemptions.

For Q2, actively managed funds—excluding money market funds—took in some $25.7 billion net, while their passively managed counterparts attracted some $88.5 billion.

Posted on 8/14/20 at 9:09 pm to wutangfinancial

The chart on p.9 of the actual report is pretty telling. The highest net total flows across all fund categories prior to 2020 was $938B in 2019. Through June of 2020, we were already at $856B, and that's even though there were net outflows in 7 of the 10 categories of risk assets. Of that $938B, 105% flowed into money market funds (this amount is more than 100% because of the net outflows in other categories).

This seems like it could support the notion that the funds created by fiscal and monetary policy are finding their way into markets, although they are still biased towards less risky assets for the time being.

This seems like it could support the notion that the funds created by fiscal and monetary policy are finding their way into markets, although they are still biased towards less risky assets for the time being.

Posted on 8/15/20 at 2:03 pm to RedStickBR

I mean we're essentially creating liabilities for the Fed which allows the PDs to lend to financial institutions. We know that money flows to risk assets because velocity of money has completely collapsed. Another aspect of this is when you reflate bond values by clicking buttons you allow risk parity and the 60/40 active crowd to buy equities when in reality they should be selling them if bond prices weren't fixed.

Posted on 8/15/20 at 6:10 pm to wutangfinancial

quote:

Another aspect of this is when you reflate bond values by clicking buttons you allow risk parity and the 60/40 active crowd to buy equities when in reality they should be selling them if bond prices weren't fixed.

This is a great point. Hadn’t thought about it quite like that, but you’re exactly right. It’s a double whammy.

Posted on 8/16/20 at 8:54 am to RedStickBR

You should check out the Lacy Hunt Endgame podcast. I'm thinking he's got this game nailed. Essentially argues when the politards start having the Fed pay the bills you go from deflation to hyperinflation. I think that's about spot on. Imagine thinking Congress can be responsible brokers of the printing press

Posted on 8/16/20 at 9:04 am to wutangfinancial

Awesome. I’ll check it out. Real Vision put out a new interview with Mike G. yesterday as well.

LINK

Also, have you listened to End Game Ep. 2 with “The Lord of the Dark Matter?” That’s a good one, too

LINK

Also, have you listened to End Game Ep. 2 with “The Lord of the Dark Matter?” That’s a good one, too

Posted on 8/16/20 at 6:49 pm to RedStickBR

I don't have time to read 8 pages. Any cliffs on when the financial Armageddon is coming?

Posted on 8/16/20 at 7:09 pm to GREENHEAD22

March 15th, 2020

Posted on 8/18/20 at 2:40 pm to wutangfinancial

Q2 Treasury Purchases

I have no clue who this guy is but he said out who purchased our Treasuries in Q2. Hint: it's not foreigners.

I have no clue who this guy is but he said out who purchased our Treasuries in Q2. Hint: it's not foreigners.

Posted on 8/20/20 at 6:17 pm to wutangfinancial

Fed assets up $50+B this week and now back above $7T

By the way, binge-listened to the Russell Napier and Lacy Hunt episodes back to back. Both were incredible, but Hunt in particular was tremendously convincing re: disinflation/deflation. Makes me want to hold more cash unless, as he highlighted, Fed assets become legal tender, in which case, buy Gold hand over fist

By the way, binge-listened to the Russell Napier and Lacy Hunt episodes back to back. Both were incredible, but Hunt in particular was tremendously convincing re: disinflation/deflation. Makes me want to hold more cash unless, as he highlighted, Fed assets become legal tender, in which case, buy Gold hand over fist

Posted on 8/25/20 at 8:07 am to RedStickBR

Good read from James Montier from GMO who argues, “No, it’s not the Fed. It’s still fundamentals.” However, he simultaneously spills significant ink complaining the fundamentals have become detached from reality. So maybe it’s not fundamentals ...

LINK

LINK

Posted on 8/25/20 at 10:12 am to RedStickBR

quote:

Hunt in particular was tremendously convincing re: disinflation/deflation

Ya, he has an incredible line in that interview. He says something to the tune of "We've been doing the same thing since the late 1600s do you think the results will change?"

quote:

Makes me want to hold more cash unless, as he highlighted, Fed assets become legal tender, in which case, buy Gold hand over fist

I'm just using options at this point instead of buying equities so I can have a huge cash cushion with virtually no risk of principal losses. Most people don't care to learn but preventing drawdowns is almost as important for wealth creation than time in the market.

Posted on 8/27/20 at 7:02 pm to wutangfinancial

Posted on 8/27/20 at 7:19 pm to RedStickBR

hey dude what did you think about jpows inflation comments today

Posted on 9/1/20 at 12:09 pm to Mr Perfect

I don't think what they announced really amounted to anything different, except insofar as the "average" approach to inflation means they'd tolerate something well in excess of 2% to make up for past years of less than 2% inflation.

What they didn't say that is more telling is that they're becoming a bit desperate on the inflation front, which could means they see a legitimate risk of deflation out there. Certainly, we're not yet seeing inflation priced into the bond market and the economic environment seems to be more suggestive of deflation than inflation at this point.

What they didn't say that is more telling is that they're becoming a bit desperate on the inflation front, which could means they see a legitimate risk of deflation out there. Certainly, we're not yet seeing inflation priced into the bond market and the economic environment seems to be more suggestive of deflation than inflation at this point.

Posted on 9/1/20 at 12:10 pm to wutangfinancial

quote:

I'm just using options at this point instead of buying equities so I can have a huge cash cushion with virtually no risk of principal losses. Most people don't care to learn but preventing drawdowns is almost as important for wealth creation than time in the market.

I'm with you. I've been heavily cash since late April. Starting to feel a bit lonely, but I just don't see a favorable risk/reward at all right now. Considering moving some significant funds into the dollar as an uncorrelated play against another crash in the markets.

Posted on 9/2/20 at 11:10 am to RedStickBR

For more on the inflation vs. deflation debate:

Hoisington Investment Management (Lacy Hunt) Q2 Letter

Hoisington Investment Management (Lacy Hunt) Q2 Letter

quote:

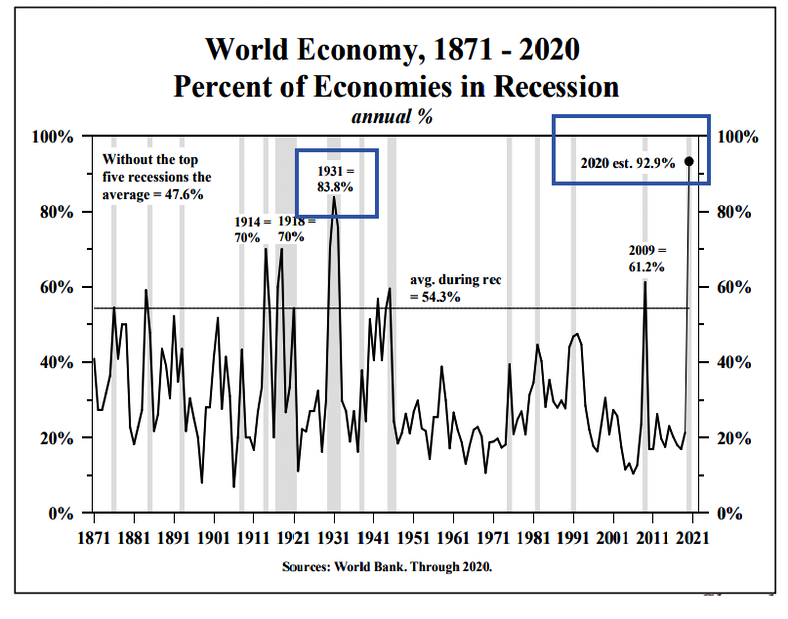

Recessions are either deeper or longer lasting when a very high percentage of the world’s economies are contracting rather than when they are centered on a limited number of countries.

quote:

Confirming economic research regarding diminishing returns of the overuse of debt, each dollar of debt generated only 38.5 cents of GDP in the first quarter of this year. This result is defined as the marginal revenue product of debt (MRPD), which is down from 40 cents at the end of 2019. Each dollar of debt has generated only 13 cents of GDP growth for the past four quarters, compared with less than one-half of the 26.5 cents generated during the final four quarters immediately before the recession that started in late 2008.

quote:

The rising debt levels and subsequent result of falling MRPD will produce two major macroeconomic consequences. First is diminishing returns, a conclusion that is derived from the production function. This idea is that unless offset by the contribution from technology, demographics or natural resources, the overuse of debt will lead to a further weakening economic growth, thereby placing downward pressure on inflation. The second macro-economic effect of weaker MRPD will be the continued downward pressure on the velocity of money.

quote:

The U.S. business sector continues to ignore Benjamin Graham’s dictum for sound corporate financial management: sell company shares when stock prices are high and use the proceeds to pay off debt and buy shares when stock prices are low by issuing debt. In the first quarter, corporate debt jumped to a record 48.7% of GDP, more than 300 basis points higher than during the Lehman crisis. The surge in corporate indebtedness coincided with a profits recession that was evident even before the coronavirus hit. Real corporate profits after tax with IVA and CCA, which were unchanged from 2012 at the end of 2019, fell in this year’s first quarter to the lowest level in nine years. The situation will be considerably worse after the figures are tabulated for the spring quarter. The stressed corporate income statement and balance sheet circumstances strongly indicate that the reopening rebound in capital spending will simply not have staying power.

quote:

Considering the depth of the decline in global GDP, the massive debt accumulation by all countries, the collapse in world trade and the synchronous nature of the contracting world economies the task of closing this output gap will be extremely difficult and time consuming. This situation could easily cause aggregate prices to fall, thus putting persistent downward pressure on inflation which will be reflected in declining long-dated U.S. government bond yields.

Posted on 9/2/20 at 11:30 am to RedStickBR

Funny I just came here to let you know the George Gammon podcast with Steven Van Metre is pretty good on the deflation narrative. I'm starting to turn into a deflation pumper at this point. My entire opinion on M2, velocity and QE has changed since this thread started.

Edit: Just noticed that's Lacy Hunt's letter. I'll definitely read the entire thing.

Edit: Just noticed that's Lacy Hunt's letter. I'll definitely read the entire thing.

This post was edited on 9/2/20 at 11:31 am

Page 8 of 23

Page 8 of 23

Popular

Back to top