- My Forums

- Tiger Rant

- LSU Recruiting

- SEC Rant

- Saints Talk

- Pelicans Talk

- More Sports Board

- Fantasy Sports

- Golf Board

- Soccer Board

- O-T Lounge

- Tech Board

- Home/Garden Board

- Outdoor Board

- Health/Fitness Board

- Movie/TV Board

- Book Board

- Music Board

- Political Talk

- Money Talk

- Fark Board

- Gaming Board

- Travel Board

- Food/Drink Board

- Ticket Exchange

- TD Help Board

Customize My Forums- View All Forums

- Show Left Links

- Topic Sort Options

- Trending Topics

- Recent Topics

- Active Topics

Started By

Message

re: 3 million kids registered for Trump accounts

Posted on 2/23/26 at 1:58 pm to NewIberiaHaircut

Posted on 2/23/26 at 1:58 pm to NewIberiaHaircut

Democrats should avoid the Trump accounts so that integrity is maintained.

0

0

Posted on 2/23/26 at 2:16 pm to NewIberiaHaircut

This is the equivalent of getting to set up an IRA before you are 1.

Before most people get earned income, you are likely to have 15-20 years of growth.

Additionally, parents can contribute up to $5k/year.

Just like an IRA, you are taxed as ordinary income on withdrawal.

Amazing all around and I am very jealous.

Before most people get earned income, you are likely to have 15-20 years of growth.

Additionally, parents can contribute up to $5k/year.

Just like an IRA, you are taxed as ordinary income on withdrawal.

Amazing all around and I am very jealous.

Posted on 2/23/26 at 3:23 pm to bigjoe1

I'm planning to open one up for the free $1k, but I don't see myself doing anything with it beyond that. There are already better benefits with START/529 accounts for education, and while having a downpayment fund sounds nice in theory, the fact that it automatically transfers ownership to the kid the day they turn 18 gives me significant pause.

Posted on 2/23/26 at 3:39 pm to Joshjrn

quote:

I'm planning to open one up for the free $1k, but I don't see myself doing anything with it beyond that.

this is the way

Posted on 2/23/26 at 3:50 pm to Helo

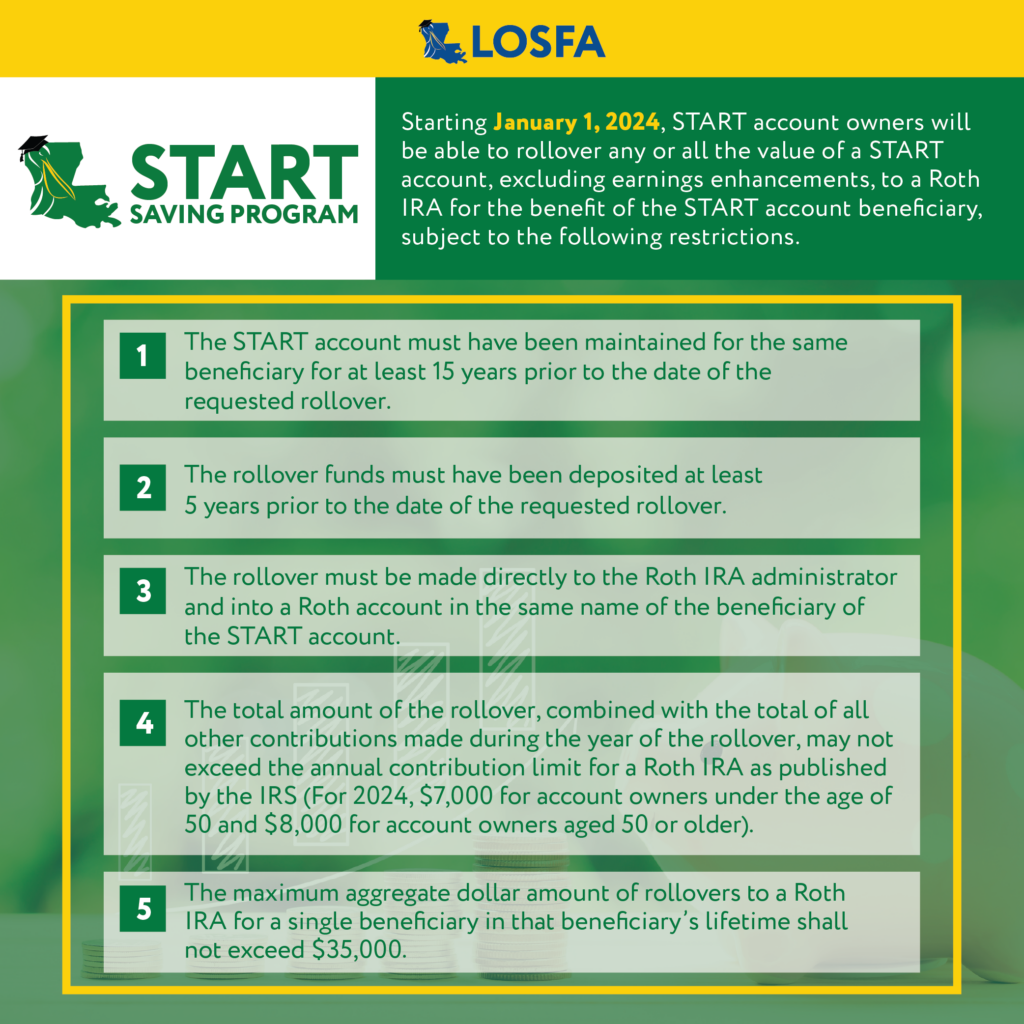

Upon some further research. 529 plans also allow Roth conversion. Found a previous thread on the LA START accounts.

2024 TD Thread

To each their own, but I still don't see the benefit of the Trump accounts if you're not eligible for the seed money or an employer match.

2024 TD Thread

To each their own, but I still don't see the benefit of the Trump accounts if you're not eligible for the seed money or an employer match.

Posted on 2/23/26 at 4:35 pm to Joshjrn

quote:

I'm planning to open one up for the free $1k, but I don't see myself doing anything with it beyond that. There are already better benefits with START/529 accounts for education, and while having a downpayment fund sounds nice in theory, the fact that it automatically transfers ownership to the kid the day they turn 18 gives me significant pause.

I don't plan on having kids, so ill admit to being the grump here on this.

When student loan forgiveness is talked about as other people paying off other peoples debts, why is this any different. Why are my tax dollars used for other kids accounts? It's pretty socialistic to take my money and redistribute to other people. It all comes off as a gimmick to put Trumps name on something else

Posted on 2/23/26 at 5:16 pm to Helo

I'll stick with a 529 that has some actual tax benefits on the backend. The $1K is great for those that cannot afford to start saving.

If this was a ROTH IRA type treatment then I would put $5K a year for every year as long as they allow it....but this is not the case.

If this was a ROTH IRA type treatment then I would put $5K a year for every year as long as they allow it....but this is not the case.

Posted on 2/23/26 at 7:07 pm to GamecockUltimate

Socialistic is exactly what it is, but people look the other way when it benefits them. As our forefathers warned us; the republic will start to fail once people realize they can vote themselves money.

Posted on 2/24/26 at 2:10 am to bigjoe1

That’s a massive response in such a short time. The Super Bowl ad definitely reached a lot of households if they're already hitting the 2 million form mark.

Posted on 2/24/26 at 11:27 am to Combaro01

I wouldn't put money in any account that has a trump name added to it.

Posted on 2/24/26 at 1:15 pm to basiletiger

So if this account had some tax advantage for your kid to get them ahead in life, you would forego doing what's in your child's best interest just to spite Trump? This is what people mean by TDS

Posted on 2/24/26 at 2:26 pm to lynxcat

quote:

I'll stick with a 529 that has some actual tax benefits on the backend. The $1K is great for those that cannot afford to start saving.

If this was a ROTH IRA type treatment then I would put $5K a year for every year as long as they allow it....but this is not the case.

I wouldn't treat it as an either/or. Fund your 529s to max the $4,800 state tax deduction, then contribute to the Trump account. At 18, your kid(s) convert the whole ~$298K to Roth over 4-5 year period while in college/early earning years. That $298K turns into tax free millions in the long run.

Assuming your kid is not irresponsible, that's probably the easiest (or at least the biggest jumpstart towards) path to lay the foundation for generational wealth. Hurts mom and dad now. Benefits kid later. Just my thoughts. YMMV

This post was edited on 2/24/26 at 11:43 pm

Posted on 2/24/26 at 2:48 pm to Lurkalot

quote:

Assuming your kid is not irresponsible

Gambling from birth that an 18 year old kid won't do something catastrophically stupid with $300k that falls into their lap one day just seems like it's asking for trouble. Everyone obviously hopes that their kid can handle it, but I think that's asking a lot. Now, build something in that treats it more like a trust and I'm completely on board.

Posted on 2/24/26 at 4:07 pm to Lurkalot

1. I do not get state tax deduction benefit.

2. What Roth conversion are you speaking of? You can only convert $35K from 529 into Roth assets.

I’m unaware of a conversion of a Trump account. You could pay the taxes on a withdrawal and then fund a ROTH IRA with that cash flow early in career…but I do not believe there is a more tax efficient way to do so .

2. What Roth conversion are you speaking of? You can only convert $35K from 529 into Roth assets.

I’m unaware of a conversion of a Trump account. You could pay the taxes on a withdrawal and then fund a ROTH IRA with that cash flow early in career…but I do not believe there is a more tax efficient way to do so .

Posted on 2/24/26 at 4:29 pm to Joshjrn

quote:

quote:

Assuming your kid is not irresponsible

Gambling from birth that an 18 year old kid won't do something catastrophically stupid with $300k that falls into their lap one day just seems like it's asking for trouble. Everyone obviously hopes that their kid can handle it, but I think that's asking a lot. Now, build something in that treats it more like a trust and I'm completely on board.

I think you're looking at the gamble the wrong way. You're looking at it as risking a $300K loss if your kid is irresponsible.

I'm looking at it as a $39M win if my kid is responsible.

I like my chances that my kids will turn out OK.

Could be wrong, but I'm willing to roll the dice.

This post was edited on 2/24/26 at 4:33 pm

Posted on 2/24/26 at 4:31 pm to lynxcat

quote:

1. I do not get state tax deduction benefit.

2. What Roth conversion are you speaking of? You can only convert $35K from 529 into Roth assets.

I’m unaware of a conversion of a Trump account. You could pay the taxes on a withdrawal and then fund a ROTH IRA with that cash flow early in career…but I do not believe there is a more tax efficient way to do so

1. If you're in Louisiana, you get a state tax benefit for contributing to a Louisiana 529.

2. I'm talking about converting the Trump Account after the age of 18.

Posted on 2/24/26 at 4:37 pm to Lurkalot

No, I’m not looking at it as a $300k loss; I’m looking at it as a potential landmine that my newly adult kid could use to frick up their lives.

Posted on 2/24/26 at 4:39 pm to Joshjrn

Well, that's fair.

Again, I'm gonna roll the dice. For me, the $39M swing is worth the risk.

Again, I'm gonna roll the dice. For me, the $39M swing is worth the risk.

This post was edited on 2/24/26 at 4:40 pm

Posted on 2/24/26 at 6:18 pm to Lurkalot

quote:

Well, that's fair.

Again, I'm gonna roll the dice. For me, the $39M swing is worth the risk.

Which on some level, I get. However, let's frame it another way. Let's say, instead of putting it in a Trump account, you put it in a trust that you control. What does that final (probably inflated due to assuming 10% gains, but still) number look like?

Posted on 2/24/26 at 9:36 pm to Joshjrn

quote:

Which on some level, I get. However, let's frame it another way. Let's say, instead of putting it in a Trump account, you put it in a trust that you control. What does that final (probably inflated due to assuming 10% gains, but still) number look like?

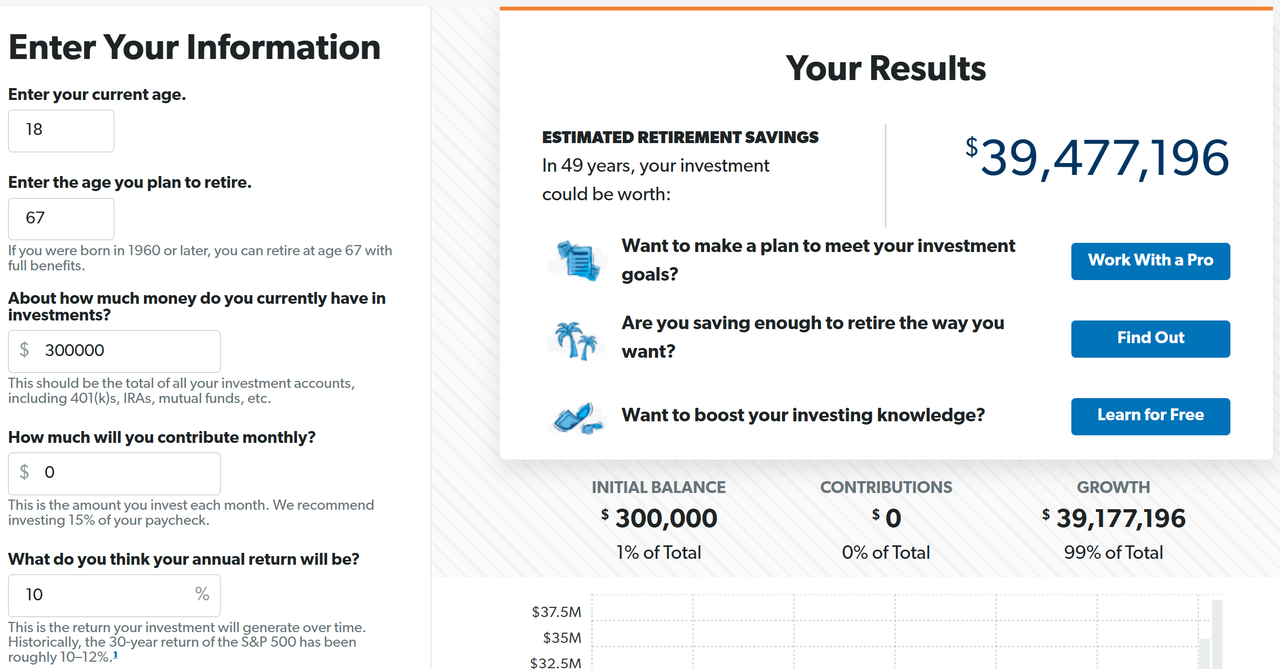

It’s about ~$11–$12 million more wealth if retired at age 67 (40+% higher). That gap widens further if you assume your kid makes annual contributions over the life of the converted Roth IRA.

Key Points

• The Roth (Trump account converted) grows the full amount with no taxes on dividends or gains.

• Roth final value at age 67: ~$39.48 million tax-free (for $300k starting amount; ~$39.18 million for $298k).

• A taxable brokerage account with the same starting amount and monthly compounding would end at roughly $27–$28 million after annual dividend taxes and final long-term capital-gains tax (exact figure depends on dividend timing and turnover).

Page 2 of 3

Page 2 of 3

Popular

Back to top