- My Forums

- Tiger Rant

- LSU Recruiting

- SEC Rant

- Saints Talk

- Pelicans Talk

- More Sports Board

- Fantasy Sports

- Golf Board

- Soccer Board

- O-T Lounge

- Tech Board

- Home/Garden Board

- Outdoor Board

- Health/Fitness Board

- Movie/TV Board

- Book Board

- Music Board

- Political Talk

- Money Talk

- Fark Board

- Gaming Board

- Travel Board

- Food/Drink Board

- Ticket Exchange

- TD Help Board

Customize My Forums- View All Forums

- Show Left Links

- Topic Sort Options

- Trending Topics

- Recent Topics

- Active Topics

Started By

Message

Mortgage Delinquencies are Spiking

Posted on 7/16/20 at 7:26 am

Posted on 7/16/20 at 7:26 am

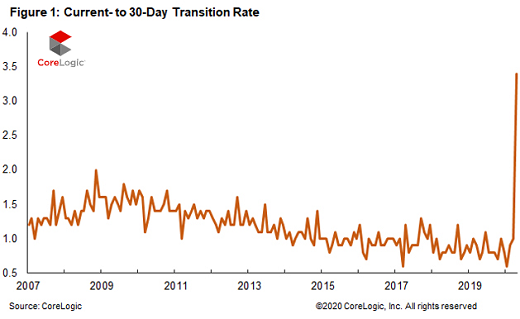

Transition from “Current” to 30-days past due: In April, the share of all mortgages that were past due, but less than 30 days, soared to 3.4% of all mortgages, the highest in the data going back to 1999. This was up from 0.7% in April last year. During the Housing Bust, this rate peaked in November 2008 at 2% (chart via CoreLogic):

It actually may be worse ....

Mortgages that are in forbearance and have not missed a payment before going into forbearance don’t count as delinquent.

They’re reported as “current.” And 8.2% of all mortgages in the US – or 4.1 million loans – are currently in forbearance, according to the Mortgage Bankers Association. But if they did not miss a payment before entering forbearance, they don’t count in the suddenly spiking delinquency data.

The onslaught of delinquencies came suddenly in April, according to CoreLogic, a property data and analytics company (owner of the Case-Shiller Home Price Index), which released its monthly Loan Performance Insights today. And it came after 27 months in a row of declining delinquency rates. These delinquency rates move in stages – and the early stages are now getting hit

LINK

It actually may be worse ....

Mortgages that are in forbearance and have not missed a payment before going into forbearance don’t count as delinquent.

They’re reported as “current.” And 8.2% of all mortgages in the US – or 4.1 million loans – are currently in forbearance, according to the Mortgage Bankers Association. But if they did not miss a payment before entering forbearance, they don’t count in the suddenly spiking delinquency data.

The onslaught of delinquencies came suddenly in April, according to CoreLogic, a property data and analytics company (owner of the Case-Shiller Home Price Index), which released its monthly Loan Performance Insights today. And it came after 27 months in a row of declining delinquency rates. These delinquency rates move in stages – and the early stages are now getting hit

LINK

15

15

Posted on 7/16/20 at 7:29 am to cadillacattack

I’m sure our health experts and leaders carefully considered these consequences.

Posted on 7/16/20 at 7:30 am to cadillacattack

Cases

Posted on 7/16/20 at 8:11 am to cadillacattack

trump and jpow need to react quickly with fiscal to inject $$$ before it gets too late

Posted on 7/16/20 at 8:29 am to cadillacattack

quote:

They’re reported as “current.” And 8.2% of all mortgages in the US – or 4.1 million loans – are currently in forbearance

It will take years for these loans to go through the forebearance process so keep that in mind.

Posted on 7/16/20 at 8:50 am to wutangfinancial

Why do you think it will take years? I think at most it will take 2.5 years. As soon as the forbearance period expires the mortgage companies are going to be hiring or contracting with a ton of people to foreclose on these houses. The foreclosure process differs by state but they can typically be evicted and the property auctioned in a short period of time.

Posted on 7/16/20 at 8:56 am to cadillacattack

quote:

In April, the share of all mortgages that were past due, but less than 30 days, soared to 3.4% of all mortgages, the highest in the data going back to 1999.

Does this count people who wait until the 15th day to pay mortgage, since there is a 15 day late grace period for late fees?

Posted on 7/16/20 at 8:57 am to Lickitty Split

quote:

Why do you think it will take years? I think at most it will take 2.5 years. As soon as the forbearance period expires the mortgage companies are going to be hiring or contracting with a ton of people to foreclose on these houses. The foreclosure process differs by state but they can typically be evicted and the property auctioned in a short period of time.

Are the banks going to want all that inventory, or are they going to give people additional chances to work with them?

Posted on 7/16/20 at 9:00 am to cadillacattack

It's hard to believe a lot of people will stop paying their mortgage just because the government says they can't be foreclosed on for non-payment.

Posted on 7/16/20 at 9:01 am to Lickitty Split

quote:

The foreclosure process differs by state but they can typically be evicted and the property auctioned in a short period of time.

I'd have to check the concentration by state, but if it's Florida, California, and Northeast states it takes several years, just like you said (2.5 years). They have the most ridiculous laws to keep people in their houses. When I used to work for a servicing shop there were stories of foreclosures in the Northeast where squatter laws prevented us from getting people out of their foreclosed house for over a year.

Russian hit another point that you're overlooking. How many people are technically delinquent on student loan payments right now that are still working?

This post was edited on 7/16/20 at 9:03 am

Posted on 7/16/20 at 9:18 am to cadillacattack

What a fearmongering article

All these ppl can refi once they are out of forbearance and make one payment

Everyone has equity

Mr Perfect continues to be very low iq

All these ppl can refi once they are out of forbearance and make one payment

Everyone has equity

Mr Perfect continues to be very low iq

Posted on 7/16/20 at 9:32 am to cadillacattack

This is a bunch of "IFs" but if the PPP loans run out and more people lose their jobs, if the forbearance period ends and if this second wave leads to more shutdowns you can really see things going sideways.

All I know is that people are spending money like crazy right now (at least where I live). Interest rate friendly environment, but its a little insane to see people buying 100k boats like nothing is wrong. I was looking at buying a used boat and EVERYTHING listed on FB marketplace was selling within the hour it was listed. Crazy times.

All I know is that people are spending money like crazy right now (at least where I live). Interest rate friendly environment, but its a little insane to see people buying 100k boats like nothing is wrong. I was looking at buying a used boat and EVERYTHING listed on FB marketplace was selling within the hour it was listed. Crazy times.

Posted on 7/16/20 at 9:36 am to SDVTiger

A little fear mongering but there is more to it then just delinquencies.

If someone is in forbearance their credit and loan ability will go down so to refinance the interest rate they refinance to will be higher and more restrictions on the loan and Income to debt ratio. So its not just that easy.

Additionally, banks have to transfer forbearance and late loans to non accrual status which means they cant show any income on the loans. Once a loan is moved to non-accrual is pretty hard to get it out even if the loan holder starts making normal payments again. Less income for bank, less capital, higher restrictions to get a loan, then come housing price decreases etc.

If someone is in forbearance their credit and loan ability will go down so to refinance the interest rate they refinance to will be higher and more restrictions on the loan and Income to debt ratio. So its not just that easy.

Additionally, banks have to transfer forbearance and late loans to non accrual status which means they cant show any income on the loans. Once a loan is moved to non-accrual is pretty hard to get it out even if the loan holder starts making normal payments again. Less income for bank, less capital, higher restrictions to get a loan, then come housing price decreases etc.

Posted on 7/16/20 at 9:41 am to cadillacattack

Isn't this to be expected with double digit unemployment? I'm surprised it isn't worse. If you are in the service industry how are you paying your bills right now?

Posted on 7/16/20 at 9:42 am to Jobo

quote:

If someone is in forbearance their credit and loan ability will go down so to refinance the interest rate they refinance to will be higher and more restrictions on the loan and Income to debt ratio. So its not just that easy.

Additionally, banks have to transfer forbearance and late loans to non accrual status which means they cant show any income on the loans. Once a loan is moved to non-accrual is pretty hard to get it out even if the loan holder starts making normal payments again. Less income for bank, less capital, higher restrictions to get a loan, then come housing price decreases etc.

In a normal world this would be true but that's not the case currently

Posted on 7/16/20 at 9:52 am to LSUFanHouston

I don’t think mortgage lenders are worried about inventory. They are worried about money in their banks. People not paying mortgages means less money in their banks. If they aren’t getting payments and the owner doesn’t have a job, 100% they are gone. It might be different for a newly employed person or someone who has a job but medical or other debt is weighing them down.

Posted on 7/16/20 at 10:02 am to Lickitty Split

quote:Typically mortgage payments are applied to the bonds issued to investors who bought mortgage-backed bonds.

People not paying mortgages means less money in their banks.

Very few banks hold mortgages they've made in their own loan portfolio.

Posted on 7/16/20 at 10:04 am to Lickitty Split

quote:

I don’t think mortgage lenders are worried about inventory. They are worried about money in their banks. People not paying mortgages means less money in their banks. If they aren’t getting payments and the owner doesn’t have a job, 100% they are gone. It might be different for a newly employed person or someone who has a job but medical or other debt is weighing them down.

Right.

But processing a foreclosure takes time and additional costs.

Perhaps a bank wants 60% of their loan paid off in a lump sum in 18 months from now, instead of 100 percent of their loan paid off (with interest) over a renegotiated term of the loan. God willing, this foolishness will end at some point, and people will be back to work. Yes, with additional debt weighing them down, and maybe the banks will take the long view.

Posted on 7/16/20 at 10:33 am to SDVTiger

quote:Assuming they didn't lose their jobs or have hours/salary cut due to Covid and now can't show enough income to qualify for a refi

All these ppl can refi once they are out of forbearance and make one payment

Posted on 7/16/20 at 10:56 am to wutangfinancial

quote:

It will take years for these loans to go through the forebearance process

No it doesn't.

I see where you corrected it but yes it is state-specific

This post was edited on 7/16/20 at 10:57 am

Page 1 of 5

Page 1 of 5

Popular

Back to top