- My Forums

- Tiger Rant

- LSU Recruiting

- SEC Rant

- Saints Talk

- Pelicans Talk

- More Sports Board

- Fantasy Sports

- Golf Board

- Soccer Board

- O-T Lounge

- Tech Board

- Home/Garden Board

- Outdoor Board

- Health/Fitness Board

- Movie/TV Board

- Book Board

- Music Board

- Political Talk

- Money Talk

- Fark Board

- Gaming Board

- Travel Board

- Food/Drink Board

- Ticket Exchange

- TD Help Board

Customize My Forums- View All Forums

- Show Left Links

- Topic Sort Options

- Trending Topics

- Recent Topics

- Active Topics

Started By

Message

HLIT - Harmonic, Inc. | GPU Connection Software Company

Posted on 5/23/26 at 10:23 am

Posted on 5/23/26 at 10:23 am

Here’s the thesis:

“AI is shifting from occasional chatbot queries to persistent agents, multimodal streaming and automated workflows running 24/7. That puts completely different demands on a network than video ever did and broadband companies have been stuck on 1990’s infrastructure the longest.

NVIDIA just invested in Nokia to turn existing cell towers into edge AI nodes via a software update with no physical rebuild required. Harmonic is the exact same play for broadband. Their CableOS software virtualizes the core of a cable network the same way. Wireless got Nokia, broadband gets Harmonic.

At GTC 2026 Comcast and Charter confirmed they are moving NVIDIA RTX 6000 Blackwell GPUs out of distant data centers and into local neighborhood hubs to monetize AI at the edge. The problem is you cannot connect a Blackwell GPU to a 30 year old cable network and expect it to function.

Harmonic is the only software that bridges that gap.

They hold a monopoly on vCMTS, the virtualization layer that modernizes cable infrastructure. The CMTS market is $5.18B in 2026 with only 15-20% of global broadband virtualized. Harmonic is doing $450M in revenue, meaning less than 10% of their own market captured with no real competition.

-> $1.2B market cap next to a $573M backlog up 77% YoY

-> 3.5x book-to-bill in Q4 2025 alone

-> Virtualization growing 33% YoY at 55% gross margins

-> Just sold the legacy video segment so headline numbers look messy but the core business is clean and accelerating

-> Comcast and Charter spending $22B combined with 2026 being the most aggressive year

-> FCC’s “Delete Delete Delete” initiative effective May 8th forces operators off 30 year old copper, freeing up tens of billions redirected into upgrades

-> $42B in BEAD grants requiring fast deployment, Harmonic software goes live in days versus months for physical builds

Biggest risk was always customer concentration but international revenue is now 41% of the business up 33% YoY. Comcast and Charter are proving the model. ”

ETA Add’l Information from bayoubengals88 post below:

“Forward P/E: sub 20. Check

PEG ratio: 1.21 Check

P/S ratio: ~3. Check

Market cap: sub 2bn. Love this size

Chart: Room to run

Theme: excellent

Watchers on StockTwits: sub 2k (big check)

Institutional ownership: 85% Check”

“AI is shifting from occasional chatbot queries to persistent agents, multimodal streaming and automated workflows running 24/7. That puts completely different demands on a network than video ever did and broadband companies have been stuck on 1990’s infrastructure the longest.

NVIDIA just invested in Nokia to turn existing cell towers into edge AI nodes via a software update with no physical rebuild required. Harmonic is the exact same play for broadband. Their CableOS software virtualizes the core of a cable network the same way. Wireless got Nokia, broadband gets Harmonic.

At GTC 2026 Comcast and Charter confirmed they are moving NVIDIA RTX 6000 Blackwell GPUs out of distant data centers and into local neighborhood hubs to monetize AI at the edge. The problem is you cannot connect a Blackwell GPU to a 30 year old cable network and expect it to function.

Harmonic is the only software that bridges that gap.

They hold a monopoly on vCMTS, the virtualization layer that modernizes cable infrastructure. The CMTS market is $5.18B in 2026 with only 15-20% of global broadband virtualized. Harmonic is doing $450M in revenue, meaning less than 10% of their own market captured with no real competition.

-> $1.2B market cap next to a $573M backlog up 77% YoY

-> 3.5x book-to-bill in Q4 2025 alone

-> Virtualization growing 33% YoY at 55% gross margins

-> Just sold the legacy video segment so headline numbers look messy but the core business is clean and accelerating

-> Comcast and Charter spending $22B combined with 2026 being the most aggressive year

-> FCC’s “Delete Delete Delete” initiative effective May 8th forces operators off 30 year old copper, freeing up tens of billions redirected into upgrades

-> $42B in BEAD grants requiring fast deployment, Harmonic software goes live in days versus months for physical builds

Biggest risk was always customer concentration but international revenue is now 41% of the business up 33% YoY. Comcast and Charter are proving the model. ”

ETA Add’l Information from bayoubengals88 post below:

“Forward P/E: sub 20. Check

PEG ratio: 1.21 Check

P/S ratio: ~3. Check

Market cap: sub 2bn. Love this size

Chart: Room to run

Theme: excellent

Watchers on StockTwits: sub 2k (big check)

Institutional ownership: 85% Check”

This post was edited on 5/23/26 at 6:40 pm

10

10

Posted on 5/23/26 at 10:25 am to iPad

Trusted source who was early to NBIS & AAOI recommended this one to me - his entry price was $14.97/share.

Finished up 19.69% Friday at a price of $15.20/share. After after-hours trading closed, the share price was $16.56 (up another 8.95%)

I encourage each of you to perform your due diligence over the extended weekend on this one - I’ll be beginning a position on Tuesday.

Finished up 19.69% Friday at a price of $15.20/share. After after-hours trading closed, the share price was $16.56 (up another 8.95%)

I encourage each of you to perform your due diligence over the extended weekend on this one - I’ll be beginning a position on Tuesday.

Posted on 5/23/26 at 10:26 am to iPad

Posted on 5/23/26 at 10:31 am to iPad

Loading Twitter/X Embed...

If tweet fails to load, click here. I located the original thesis post - the one in the post I made came directly from a source I trust who certainly lifted it from this X user. He goes into further detail so I wanted to include it here.

Posted on 5/23/26 at 10:32 am to iPad

Posted on 5/23/26 at 10:32 am to iPad

Posted on 5/23/26 at 10:46 am to iPad

Forward P/E: sub 20. Check

PEG ratio: 1.21 Check

P/S ratio: ~3. Check

Market cap: sub 2bn. Love this size

Chart: Room to run

Theme: excellent

Watchers on StockTwits: sub 2k (big check)

Institutional ownership: 85% Check

Yeah, this looks like a winner.

I’ll probably dump some speculative stuff and pile in on Tuesday.

I need a 3rd or 4th name to be really bullish on, comfortable with, high conviction hold.

PEG ratio: 1.21 Check

P/S ratio: ~3. Check

Market cap: sub 2bn. Love this size

Chart: Room to run

Theme: excellent

Watchers on StockTwits: sub 2k (big check)

Institutional ownership: 85% Check

Yeah, this looks like a winner.

I’ll probably dump some speculative stuff and pile in on Tuesday.

I need a 3rd or 4th name to be really bullish on, comfortable with, high conviction hold.

This post was edited on 5/23/26 at 10:50 am

Posted on 5/23/26 at 10:48 am to bayoubengals88

quote:

Forward P/E: Check PEG ratio: Check P/S ratio: Check Market cap: Love Chart: Room to run Theme: excellent Yeah, this looks like a winner.

I always value your second opinion - was hoping you’d be around today to scope it out and let me know your thoughts. I think that our investing philosophies align well.

Hoping this is half as good as your OUST prediction - I still think OUST has multi-bagger potential. Not selling a single share no matter what and will continue to accumulate with any pullback.

This post was edited on 5/23/26 at 10:49 am

Posted on 5/23/26 at 10:51 am to iPad

Sure thing

Keep bringing the alpha (though I may have all can handle at this point)!

Keep bringing the alpha (though I may have all can handle at this point)!

Posted on 5/23/26 at 11:02 am to iPad

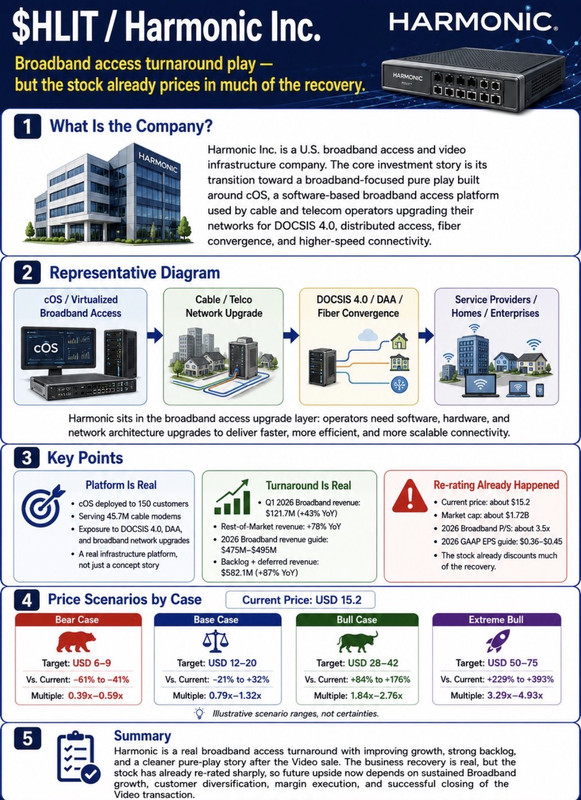

Harmonic Inc. (HLIT) Company Overview

I. Introduction to Harmonic Inc.

Harmonic Inc. is a global technology leader specializing in broadband access solutions and video delivery infrastructure. Headquartered in San Jose, California, the company provides hardware, software, and software-as-a-service (SaaS) solutions that enable network operators, cable providers, and media companies to deliver high-speed data and high-quality video content. Harmonic has been a pioneer in transforming cable networks through virtualized architectures, notably its cOS platform.

II. CEO History and Leadership

The current chief executive officer is Nimrod Ben-Natan, who assumed the role on June 11, 2024. Ben-Natan has a long history with Harmonic, joining the company in 1996 as a software engineer. He was instrumental in developing the company’s first-generation video transmission platform and later led the broadband business as senior vice president starting in 2012. His leadership has been a driving force behind the company’s strategic transition toward virtualized broadband technology. He succeeded longtime CEO Patrick Harshman, who oversaw the company’s multi-year strategic transformation.

III. Business Divisions and Product Offerings

Harmonic is currently transitioning into a "pure-play" broadband business.

A. Broadband Access Networks: This is the company's primary growth engine. Harmonic provides virtualized cable access solutions (the cOS platform), optical networking products, and data gateways. These technologies allow operators to deploy gigabit internet speeds over existing hybrid fiber-coax (HFC) networks more efficiently.

B. Video Business: This division offers compression, processing, and playout solutions. In early 2026, Harmonic entered into an asset purchase agreement to sell this business to MediaKind. Following this agreement, the video segment has been reclassified as discontinued operations in the company's financial reporting.

IV. Profitability and Financial Outlook

Harmonic is currently profitable and reported strong results for the first quarter of 2026.

A. Current Financial Status: In Q1 2026, the company achieved non-GAAP earnings per share of $0.17, surpassing analyst expectations. Broadband revenue grew 43% year-over-year to $121.7 million, with an 87% increase in backlog and deferred revenue.

B. Full-Year 2026 Outlook: Following the strong Q1 performance, management raised its full-year guidance for the broadband segment. The company expects broadband revenue between $475 million and $495 million, with non-GAAP net income per share projected in the $0.57 to $0.67 range.

C. Divestiture Impact: The sale of the video business is expected to close in the first half of 2026, which management expects will improve operational focus and financial flexibility for the remaining broadband operations.

V. Investment Thesis (TLDR)

Harmonic is a compelling play on the global upgrade cycle of broadband infrastructure. By divesting its mature video assets, the company is evolving into a higher-margin, software-focused broadband innovator. The 43% year-over-year growth in its broadband segment and a significant increase in backlog demonstrate a clear path to operational leverage. Although historical profitability has been volatile, the strategic restructuring and the growing industry demand for virtualized cable access networks position HLIT to capture market share and sustain long-term profitability as global operators race to deliver gigabit speeds to consumers.

I. Introduction to Harmonic Inc.

Harmonic Inc. is a global technology leader specializing in broadband access solutions and video delivery infrastructure. Headquartered in San Jose, California, the company provides hardware, software, and software-as-a-service (SaaS) solutions that enable network operators, cable providers, and media companies to deliver high-speed data and high-quality video content. Harmonic has been a pioneer in transforming cable networks through virtualized architectures, notably its cOS platform.

II. CEO History and Leadership

The current chief executive officer is Nimrod Ben-Natan, who assumed the role on June 11, 2024. Ben-Natan has a long history with Harmonic, joining the company in 1996 as a software engineer. He was instrumental in developing the company’s first-generation video transmission platform and later led the broadband business as senior vice president starting in 2012. His leadership has been a driving force behind the company’s strategic transition toward virtualized broadband technology. He succeeded longtime CEO Patrick Harshman, who oversaw the company’s multi-year strategic transformation.

III. Business Divisions and Product Offerings

Harmonic is currently transitioning into a "pure-play" broadband business.

A. Broadband Access Networks: This is the company's primary growth engine. Harmonic provides virtualized cable access solutions (the cOS platform), optical networking products, and data gateways. These technologies allow operators to deploy gigabit internet speeds over existing hybrid fiber-coax (HFC) networks more efficiently.

B. Video Business: This division offers compression, processing, and playout solutions. In early 2026, Harmonic entered into an asset purchase agreement to sell this business to MediaKind. Following this agreement, the video segment has been reclassified as discontinued operations in the company's financial reporting.

IV. Profitability and Financial Outlook

Harmonic is currently profitable and reported strong results for the first quarter of 2026.

A. Current Financial Status: In Q1 2026, the company achieved non-GAAP earnings per share of $0.17, surpassing analyst expectations. Broadband revenue grew 43% year-over-year to $121.7 million, with an 87% increase in backlog and deferred revenue.

B. Full-Year 2026 Outlook: Following the strong Q1 performance, management raised its full-year guidance for the broadband segment. The company expects broadband revenue between $475 million and $495 million, with non-GAAP net income per share projected in the $0.57 to $0.67 range.

C. Divestiture Impact: The sale of the video business is expected to close in the first half of 2026, which management expects will improve operational focus and financial flexibility for the remaining broadband operations.

V. Investment Thesis (TLDR)

Harmonic is a compelling play on the global upgrade cycle of broadband infrastructure. By divesting its mature video assets, the company is evolving into a higher-margin, software-focused broadband innovator. The 43% year-over-year growth in its broadband segment and a significant increase in backlog demonstrate a clear path to operational leverage. Although historical profitability has been volatile, the strategic restructuring and the growing industry demand for virtualized cable access networks position HLIT to capture market share and sustain long-term profitability as global operators race to deliver gigabit speeds to consumers.

Posted on 5/23/26 at 11:04 am to bayoubengals88

Ok, I’m done hijacking after this one:

An investment analyst or macro-trader focused on telecom infrastructure—similar to the style of sector-specific "Stock Talk" publications—looks for distinct catalysts, operational leverage, and clear secular trends. Based on this typical investment framework, an analysis reveals what an investor actively trading the telecom and network infrastructure space would find appealing and concerning about Harmonic Inc. (HLIT):

What They Would Like

* **Pure-Play Telecommunications Exposure:** By selling off its legacy Video business to MediaKind, Harmonic is shedding its identity as a fragmented media-tech hybrid. A telecom-focused trader would love this transformation into a "pure-play" broadband infrastructure company, as it makes the equity significantly easier to value and align with broader telecom CapEx spending trends.

* **Secular "Gigabit Upgrade" Tailwinds:** Telecom service providers globally are in a mandatory multi-year cycle to upgrade existing hybrid fiber-coax (HFC) and cable networks to meet massive consumer demand for bandwidth. Harmonic's cOS platform is the market leader in virtualized cable access, meaning the company sits directly in the sweet spot of this telecom CapEx wave.

* **Explosive Broadband Backlog Growth:** A macro or momentum trader in the sector would heavily favor the raw operational data from Harmonic's first quarter 2026 earnings. A 43% year-over-year increase in broadband segment revenue, coupled with an 87% increase in backlog and deferred revenue, demonstrates massive, high-conviction forward demand that de-risks future quarters.

What They Would Not Like

* **Volatile Historical Earnings and Margin Compression:** A strict fundamental value investor or risk-averse trader might hesitate at Harmonic's historical profit volatility. Even with strong raised guidance for full-year 2026 non-GAAP EPS ($0.57 to $0.67), gross margins are being tightly compressed by elevated component/memory costs and the operational friction of ramping up new hardware lines.

* **Customer Concentration Risk:** Like many mid-cap telecom equipment providers, Harmonic relies heavily on a handful of massive Tier-1 telecom and cable giants (such as Comcast and Charter) for the bulk of its revenue. Any delay in rollouts or a shifting capital deployment strategy by just one major customer can create sudden, dramatic earnings misses.

* **Execution Risk in the Divestiture Transition:** While the sale of the Video division is structurally positive, a trader would remain cautious until the deal officially closes and the company successfully completes the restructuring. Corporate carve-outs frequently present unexpected friction, unabsorbed overhead costs, or temporary operational distractions.

An investment analyst or macro-trader focused on telecom infrastructure—similar to the style of sector-specific "Stock Talk" publications—looks for distinct catalysts, operational leverage, and clear secular trends. Based on this typical investment framework, an analysis reveals what an investor actively trading the telecom and network infrastructure space would find appealing and concerning about Harmonic Inc. (HLIT):

What They Would Like

* **Pure-Play Telecommunications Exposure:** By selling off its legacy Video business to MediaKind, Harmonic is shedding its identity as a fragmented media-tech hybrid. A telecom-focused trader would love this transformation into a "pure-play" broadband infrastructure company, as it makes the equity significantly easier to value and align with broader telecom CapEx spending trends.

* **Secular "Gigabit Upgrade" Tailwinds:** Telecom service providers globally are in a mandatory multi-year cycle to upgrade existing hybrid fiber-coax (HFC) and cable networks to meet massive consumer demand for bandwidth. Harmonic's cOS platform is the market leader in virtualized cable access, meaning the company sits directly in the sweet spot of this telecom CapEx wave.

* **Explosive Broadband Backlog Growth:** A macro or momentum trader in the sector would heavily favor the raw operational data from Harmonic's first quarter 2026 earnings. A 43% year-over-year increase in broadband segment revenue, coupled with an 87% increase in backlog and deferred revenue, demonstrates massive, high-conviction forward demand that de-risks future quarters.

What They Would Not Like

* **Volatile Historical Earnings and Margin Compression:** A strict fundamental value investor or risk-averse trader might hesitate at Harmonic's historical profit volatility. Even with strong raised guidance for full-year 2026 non-GAAP EPS ($0.57 to $0.67), gross margins are being tightly compressed by elevated component/memory costs and the operational friction of ramping up new hardware lines.

* **Customer Concentration Risk:** Like many mid-cap telecom equipment providers, Harmonic relies heavily on a handful of massive Tier-1 telecom and cable giants (such as Comcast and Charter) for the bulk of its revenue. Any delay in rollouts or a shifting capital deployment strategy by just one major customer can create sudden, dramatic earnings misses.

* **Execution Risk in the Divestiture Transition:** While the sale of the Video division is structurally positive, a trader would remain cautious until the deal officially closes and the company successfully completes the restructuring. Corporate carve-outs frequently present unexpected friction, unabsorbed overhead costs, or temporary operational distractions.

Posted on 5/23/26 at 11:07 am to bayoubengals88

quote:

Ok, I’m done hijacking after this one:

Let’s call this one a collaborative effort! I appreciate the work you put in here on MB. Helped me get interested in becoming a regular here.

Feel free to keep sharing over the extended weekend, the more information prior to Tuesday’s open, the better.

Posted on 5/23/26 at 1:15 pm to iPad

Loading Twitter/X Embed...

If tweet fails to load, click here. Read this full post thread for more information on the long HLIT thesis.

Posted on 5/23/26 at 1:26 pm to iPad

Thank you both for the info

I’ll be picking up some shares Tuesday morning

I’ll be picking up some shares Tuesday morning

Posted on 5/23/26 at 1:29 pm to iPad

What are y'all thinking as far as entry price?

Posted on 5/23/26 at 1:35 pm to Sabans straw hat

quote:

What are y'all thinking as far as entry price?

It closed at $16.58 in Friday’s after-hours trading. I’m eyeing around that but would be fine for anything under $17 since I’ll be in this one for the long haul. I’ll probably see in pre-market if I can get anything under the $16.58 mark.

Thesis is compelling enough to convince me to buy at current price even after a +20% day and large additional gain during after hours. That’s just my 2 cents.

This post was edited on 5/23/26 at 1:36 pm

Posted on 5/23/26 at 1:45 pm to iPad

Thank you for the info.

Posted on 5/23/26 at 3:02 pm to Sabans straw hat

quote:

Thank you for the info.

Happy to help! Hope this one turns out to be a winner

Posted on 5/23/26 at 3:14 pm to iPad

Robot counterpoint - I have not looked into this myself enough to take a position:

The “monopoly” framing is the weakest part. Harmonic had ~98% vCMTS share in 2023 because Comcast was effectively the only deployment at scale. That’s a first-mover lead, not a moat. The reality:

• Vecima already won Cox in April 2025 as its first vCMTS customer and acquired Casa Systems’ cable assets

• CommScope launched vCore and is “increasingly aggressive”

• Charter has publicly said it wants multiple vCMTS vendors, leaving the door open for Vecima

• Dell’Oro’s own analyst calls the market “wide open”

The “monopoly” framing is the weakest part. Harmonic had ~98% vCMTS share in 2023 because Comcast was effectively the only deployment at scale. That’s a first-mover lead, not a moat. The reality:

• Vecima already won Cox in April 2025 as its first vCMTS customer and acquired Casa Systems’ cable assets

• CommScope launched vCore and is “increasingly aggressive”

• Charter has publicly said it wants multiple vCMTS vendors, leaving the door open for Vecima

• Dell’Oro’s own analyst calls the market “wide open”

Posted on 5/23/26 at 3:21 pm to iPad

Page 1 of 3

Page 1 of 3

Popular

Back to top