- My Forums

- Tiger Rant

- LSU Recruiting

- SEC Rant

- Saints Talk

- Pelicans Talk

- More Sports Board

- Coaching Changes

- Fantasy Sports

- Golf Board

- Soccer Board

- O-T Lounge

- Tech Board

- Home/Garden Board

- Outdoor Board

- Health/Fitness Board

- Movie/TV Board

- Book Board

- Music Board

- Political Talk

- Money Talk

- Fark Board

- Gaming Board

- Travel Board

- Food/Drink Board

- Ticket Exchange

- TD Help Board

Customize My Forums- View All Forums

- Show Left Links

- Topic Sort Options

- Trending Topics

- Recent Topics

- Active Topics

Started By

Message

In Schwab see some government bonds 10-20y yielding 6.09 and 6.12% respectively

Posted on 8/8/23 at 3:07 pm

Posted on 8/8/23 at 3:07 pm

They are callable FFCB and FHLB

Why so high? Is their risk? Seems like they are quasi government bonds. Seems like and awesome place for someone with 20y to go for their fixed income portion of retirement.

What am I missing?

Why so high? Is their risk? Seems like they are quasi government bonds. Seems like and awesome place for someone with 20y to go for their fixed income portion of retirement.

What am I missing?

3

3

Posted on 8/8/23 at 3:13 pm to thelawnwranglers

Both are government sponsored entities not agencies

Posted on 8/8/23 at 3:29 pm to thelawnwranglers

I haven't checked on these but the shorter maturities I've looked at are all callable. I've been checking 1-5 years. Pretty quick continuous calls. So if rates go down they call them and if rates go up they let them ride. Heads I win tails you lose. I won't touch them. I used to like to buy FFCB, FHLB, CoBank but no more.

Posted on 8/8/23 at 3:50 pm to thelawnwranglers

There's going to be additional risk premium but I'd take a guess that they have to entice investors with higher yield because of the negative convexity when yield drop. Same with MBS but MBS prices are way more complex than that.

Posted on 8/8/23 at 4:11 pm to wutangfinancial

quote:

There's going to be additional risk premium

I feel like you are telling me to diversify my bonds? Lol

Posted on 8/8/23 at 5:37 pm to thelawnwranglers

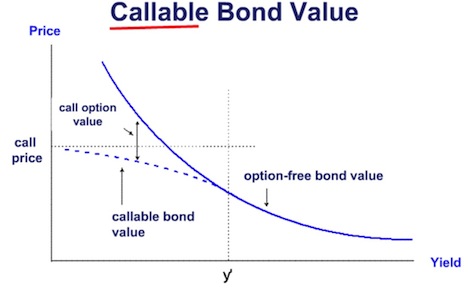

Callable bonds don’t typically appreciate like other long term bonds when rates ultimately fall.

If rates go up, you’re stuck. If they go down, the issuer will bail.

Most of these have coupons of 5.5-5.75%, so if rates fall 1.5-2% they’ll likely get called as soon as possible. Keep in mind the coupon is the cost to the issuer - the YTW is largely irrelevant to them even though it’s important to you.

A callable bond with a coupon of 2% isn’t getting called for a long time.

If rates go up, you’re stuck. If they go down, the issuer will bail.

Most of these have coupons of 5.5-5.75%, so if rates fall 1.5-2% they’ll likely get called as soon as possible. Keep in mind the coupon is the cost to the issuer - the YTW is largely irrelevant to them even though it’s important to you.

A callable bond with a coupon of 2% isn’t getting called for a long time.

Posted on 8/8/23 at 5:51 pm to slackster

quote:

Callable bonds don’t typically appreciate like other long term bonds when rates ultimately fall.

I don’t understand appreciate? Do they not pay out yearly or not until they mature? Why are we assuming rates ultimately fall? For a 10y I’m not sure they aren’t a good deal, historically rates are not really high

Posted on 8/8/23 at 7:16 pm to bovine1

quote:

Heads I win tails you lose.

Well put callable bigger deal breaker for me then I thought

Posted on 8/8/23 at 7:16 pm to baldona

quote:

I don’t understand appreciate? Do they not pay out yearly or not until they mature? Why are we assuming rates ultimately fall? For a 10y I’m not sure they aren’t a good deal, historically rates are not really high

Almost all bonds that we discuss on this board have a market value between purchase and maturity. Most retail investors think of bonds as buy and hold to maturity instruments, which is great, but bonds are traded all the damn time. If you think long term rates have peaked, buying a long duration bond (15+ years) could be a lucrative bet. Your bond will appreciate in price if rates fall, just as bond prices were destroyed in 2022 in a rapidly rising rate environment.

Part of buying a bond is at least understanding the price fluctuation of the bond until maturity. It will mature at par, but the price can swing wildly until then.

Posted on 8/8/23 at 7:19 pm to bovine1

quote:

I haven't checked on these but the shorter maturities I've looked at are all callable. I've been checking 1-5 years. Pretty quick continuous calls. So if rates go down they call them and if rates go up they let them ride. Heads I win tails you lose. I won't touch them. I used to like to buy FFCB, FHLB, CoBank but no more.

It’s an intriguing bet or they wouldn’t exist. Even if it’s called it’s markedly better than CDs with essentially the same risk.

However, if you’re buying them as a way to insulate yourself from rates falling, they won’t work.

Page 1 of 1

Page 1 of 1

Popular

Back to top