- My Forums

- Tiger Rant

- LSU Recruiting

- SEC Rant

- Saints Talk

- Pelicans Talk

- More Sports Board

- Fantasy Sports

- Golf Board

- Soccer Board

- O-T Lounge

- Tech Board

- Home/Garden Board

- Outdoor Board

- Health/Fitness Board

- Movie/TV Board

- Book Board

- Music Board

- Political Talk

- Money Talk

- Fark Board

- Gaming Board

- Travel Board

- Food/Drink Board

- Ticket Exchange

- TD Help Board

Customize My Forums- View All Forums

- Show Left Links

- Topic Sort Options

- Trending Topics

- Recent Topics

- Active Topics

Started By

Message

KRMN-picks and shovels space position

Posted on 6/3/26 at 10:32 am

Posted on 6/3/26 at 10:32 am

Business with Brian recommended this and CACi as opposed to rklb and asts which are not making money but losing.

This post was edited on 6/3/26 at 10:55 am

4

4

Posted on 6/3/26 at 11:03 am to LChama

It’s so scary to invest in anything new while trump is crashing the stock market

I might just wait until the adults are back in charge

I might just wait until the adults are back in charge

Posted on 6/3/26 at 11:28 am to el Gaucho

quote:

I might just wait

We will wave to you from the TD yacht

Posted on 6/3/26 at 11:49 am to LSUcam7

They coming to repo the yacht today

Posted on 6/3/26 at 11:55 am to LSUcam7

quote:

We will wave to you from the TD yacht

Aoc and bernie are gonna share the wealth

Posted on 6/3/26 at 7:00 pm to LChama

This post was edited on 6/3/26 at 7:06 pm

Posted on 6/3/26 at 7:27 pm to LChama

Following…

Posted on 6/3/26 at 8:58 pm to bayoubengals88

quote:

Following…

Let me know if you find the reasoning compelling. Im in for 200. Sold my other space stocks to get in here. Not sure if people are familiar with Business with Bob but thats who i first heard about it from.

May buy 5-10 Shares of CACi that he mentions as his no.1.

This post was edited on 6/3/26 at 9:12 pm

Posted on 6/4/26 at 4:19 pm to LChama

My first question was Space or Defense?

By revenue segment, as of Q1 2026, the breakdown is: Tactical Missiles and Integrated Defense Systems 30%, Space and Launch 29%, Hypersonics and Strategic Missile Defense 24%, and Maritime Defense Systems 17%.

So defense — combining tactical missiles, hypersonics, and maritime — accounts for roughly 71% of revenue, and space is 29%. This is primarily a defense company.

- But the specific nature of its defense work is what matters: it's not in legacy platforms like aircraft or armored vehicles.

- It's in the fastest-growing segments of DoD spending: hypersonic weapons, missile defense interceptors, guided munitions, and UAS systems.

- These programs have strong bipartisan support and are explicitly protected in budget discussions.

----------

There was a secondary offering at $61/share in late May for original private equity owners to sell shares. I'm talking about Trive Capital, who brought the company public in 2025. KRMN was not able to receive any money from the sale and no new shares were issued. Good. This sale was Trive making a distribution to their investors.

The good news is that Trive is now largely out of the way with their current ownership at only 3% after selling 65% of their shares in that recent round.

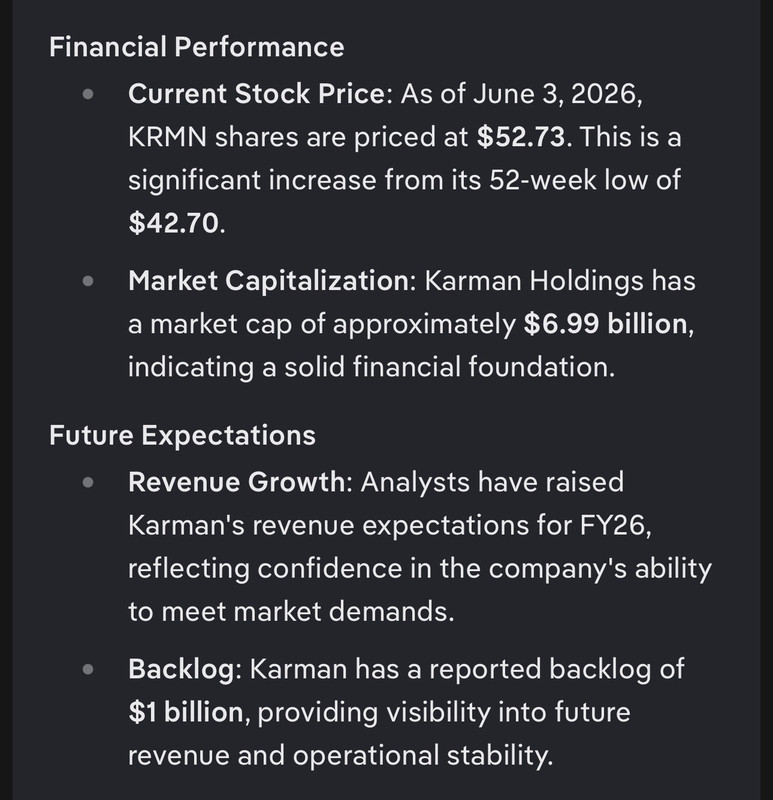

So $54/share isn't bad IMO, especially given the price targets, guidance, and backlog.

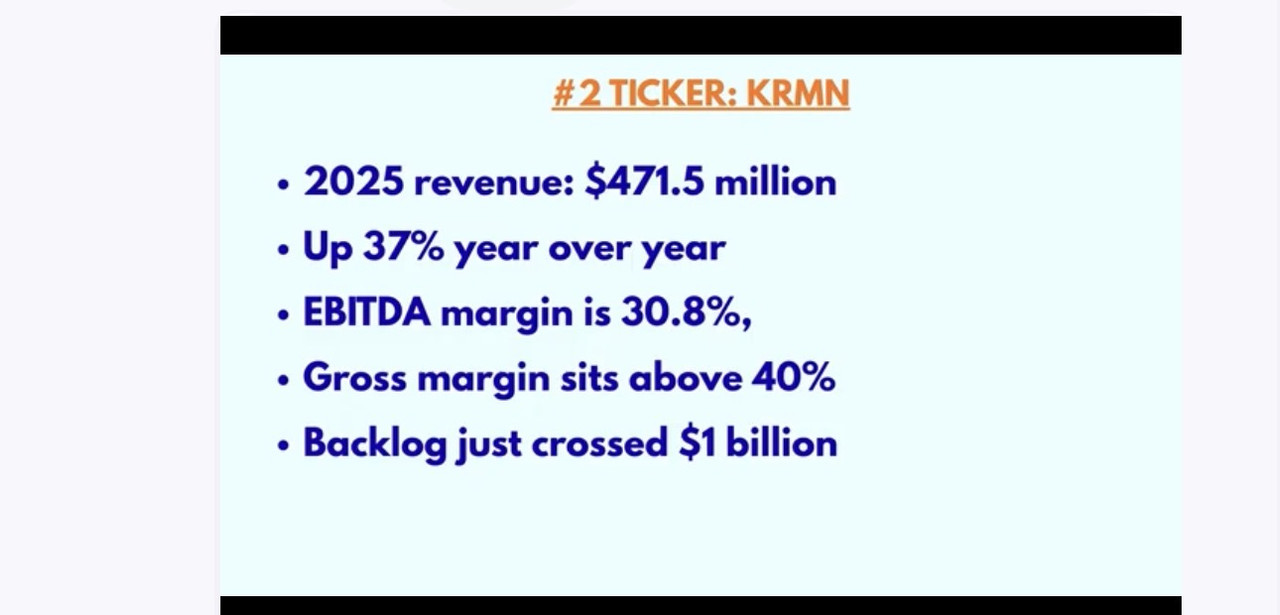

I bought 115 shares because, in short, EPS is expected to improve tremendously due to a good cleaning up of the capital structure:

The first and biggest is intangible amortization. Every time Karman acquires a company, accounting rules require it to assign fair values to the acquired customer relationships, technology, backlog, and brand — and then amortize those values over their estimated useful lives, typically 7–15 years. Amortization rose to $10.9 million in Q1 2026 alone, with intangible assets now sitting at $400.5 million net on the balance sheet. Annualized, that's roughly $44M in non-cash amortization eating directly into GAAP net income every single year. This drag shrinks predictably over time as the intangible balances age down — it's mathematical, not operational.

The second is interest expense. Interest expense was $12.6 million for Q1 2026 — roughly $50M annualized — on the $758M term loan. That's real cash out the door to Citibank every quarter, and it flows directly through the income statement reducing taxable income and net income.

The third is that Karman is in a heavy investment phase right now. Roughly half of 2026 growth is inorganic, meaning integration costs, one-time transaction fees, and the setup costs of folding Seemann, ISP, and Metal Technology into the operating structure are all burdening the current GAAP P&L even as those acquisitions produce revenue.

By revenue segment, as of Q1 2026, the breakdown is: Tactical Missiles and Integrated Defense Systems 30%, Space and Launch 29%, Hypersonics and Strategic Missile Defense 24%, and Maritime Defense Systems 17%.

So defense — combining tactical missiles, hypersonics, and maritime — accounts for roughly 71% of revenue, and space is 29%. This is primarily a defense company.

- But the specific nature of its defense work is what matters: it's not in legacy platforms like aircraft or armored vehicles.

- It's in the fastest-growing segments of DoD spending: hypersonic weapons, missile defense interceptors, guided munitions, and UAS systems.

- These programs have strong bipartisan support and are explicitly protected in budget discussions.

----------

There was a secondary offering at $61/share in late May for original private equity owners to sell shares. I'm talking about Trive Capital, who brought the company public in 2025. KRMN was not able to receive any money from the sale and no new shares were issued. Good. This sale was Trive making a distribution to their investors.

The good news is that Trive is now largely out of the way with their current ownership at only 3% after selling 65% of their shares in that recent round.

So $54/share isn't bad IMO, especially given the price targets, guidance, and backlog.

I bought 115 shares because, in short, EPS is expected to improve tremendously due to a good cleaning up of the capital structure:

The first and biggest is intangible amortization. Every time Karman acquires a company, accounting rules require it to assign fair values to the acquired customer relationships, technology, backlog, and brand — and then amortize those values over their estimated useful lives, typically 7–15 years. Amortization rose to $10.9 million in Q1 2026 alone, with intangible assets now sitting at $400.5 million net on the balance sheet. Annualized, that's roughly $44M in non-cash amortization eating directly into GAAP net income every single year. This drag shrinks predictably over time as the intangible balances age down — it's mathematical, not operational.

The second is interest expense. Interest expense was $12.6 million for Q1 2026 — roughly $50M annualized — on the $758M term loan. That's real cash out the door to Citibank every quarter, and it flows directly through the income statement reducing taxable income and net income.

The third is that Karman is in a heavy investment phase right now. Roughly half of 2026 growth is inorganic, meaning integration costs, one-time transaction fees, and the setup costs of folding Seemann, ISP, and Metal Technology into the operating structure are all burdening the current GAAP P&L even as those acquisitions produce revenue.

Posted on 6/16/26 at 1:24 pm to bayoubengals88

Maybe this is finally making a turn.

Posted on 6/16/26 at 1:34 pm to BottomFeeder

I kept dumping for slight gain or loss.

It should damn well be bottomed.

Extremely low margin type of business though. Not really my cup of tea long term.

It should damn well be bottomed.

Extremely low margin type of business though. Not really my cup of tea long term.

Page 1 of 1

Page 1 of 1

Popular

Back to top