- My Forums

- Tiger Rant

- LSU Recruiting

- SEC Rant

- Saints Talk

- Pelicans Talk

- More Sports Board

- Fantasy Sports

- Golf Board

- Soccer Board

- O-T Lounge

- Tech Board

- Home/Garden Board

- Outdoor Board

- Health/Fitness Board

- Movie/TV Board

- Book Board

- Music Board

- Political Talk

- Money Talk

- Fark Board

- Gaming Board

- Travel Board

- Food/Drink Board

- Ticket Exchange

- TD Help Board

Customize My Forums- View All Forums

- Show Left Links

- Topic Sort Options

- Trending Topics

- Recent Topics

- Active Topics

Started By

Message

re: 600 pts down? WTH is going on

Posted on 10/25/24 at 6:00 pm to notiger1997

Posted on 10/25/24 at 6:00 pm to notiger1997

quote:

Can you please cut and paste a few more things?

That took 3 minutes to do while sitting on the shitter.

You also wanna be dead wrong about something and then be a smug little prick about it? If so, I'm happy to rub your nose in it during my next bowel movement (tomorrow sometime).

0

0

Posted on 10/26/24 at 9:48 am to Longhorn Actual

Editing my post for clarity.

My initial post was a sarcastic remark towards another poster who was giddy about the .5 cut (thinking it should have been a full cut) because he believes the FedFund directly impacts mortgage rates to the point where a cut to it automatically means a cut to mortgages.

Your response was so vague it seemed to support that poster's belief so I responded with a gentle rebuttal.

And you lost your shite.

My initial post was a sarcastic remark towards another poster who was giddy about the .5 cut (thinking it should have been a full cut) because he believes the FedFund directly impacts mortgage rates to the point where a cut to it automatically means a cut to mortgages.

Your response was so vague it seemed to support that poster's belief so I responded with a gentle rebuttal.

And you lost your shite.

This post was edited on 10/26/24 at 10:19 am

Posted on 10/26/24 at 12:09 pm to Longhorn Actual

quote:

You're little passive-aggressive smily face is itself laughable given you aren't nearly as knowledgable/smart as you think you are.

Bard is one of the dumbest posters to ever grace the money board

Its amazing how smart he thinks he is

Posted on 10/26/24 at 12:44 pm to Bard

quote:

so I responded with a gentle rebuttal. And you lost your shite.

You can be dead wrong and you can be a smartass.

One or the other is understandable on occasion. We all have our moments.

Being both simultaneously should be avoided at all costs.

You were wrong and acted like a condescending passive-aggressive prick about it.

You were dismissed with 3 minutes’ worth of receipts, copy/pasted while taking a dump. That’s how dead wrong you were.

And you still haven’t learned anything.

Posted on 10/26/24 at 1:06 pm to SDVTiger

quote:

Bard is one of the dumbest posters to ever grace the money board Its amazing how smart he thinks he is

This isn’t a dogpile. Take your shots directly at him…if you think you hold the high ground…

Posted on 10/26/24 at 1:11 pm to SDVTiger

quote:

SDVTiger

quote:

Bard is one of the dumbest posters to ever grace the money board

Hilarious coming from you.

Posted on 10/26/24 at 1:13 pm to Longhorn Actual

quote:

You were wrong and acted like a condescending passive-aggressive prick about it.

You're right. I was wrong in thinking you weren't so overly sensitive that you would take a benign response and turn it into butthurt rage-posting.

quote:

You were dismissed with 3 minutes’ worth of receipts, copy/pasted while taking a dump. That’s how dead wrong you were.

I was wrong again. I thought you were an adult. Only children type something like that.

After you've napped off your White Claw rage, if you're game to non-emotionally discourse on 10yr tails, auctions, MBS and how continued debt-creation basically mandates mortgage rates staying strong, I'm game.

This post was edited on 10/26/24 at 1:17 pm

Posted on 10/26/24 at 1:15 pm to SDVTiger

quote:

Bard is one of the dumbest posters to ever grace the money board

Its amazing how smart he thinks he is

Tell me, son, how is that 30yr mortgage rate doing now that you've gotten your .5 cut? If the FedFund has such control over it, why is it going back up?

I'll hang up and listen.

This post was edited on 10/26/24 at 1:18 pm

Posted on 10/26/24 at 1:37 pm to Bard

quote:

Tell me, son, how is that 30yr mortgage rate doing now that you've gotten your .5 cut? If the FedFund has such control over it, why is it going back up?

What does the fed rate drop have to do with mortgagae rates

Go take a gander at what mortgage rates do after a first cut

quote:

you think you hold the high ground

The 2 tards below you said there was zero % chance of a fed cut of .5% cause they have no idea what they are talking about and cant read data very well

But they love them some charts

This post was edited on 10/26/24 at 1:41 pm

Posted on 10/26/24 at 2:04 pm to SDVTiger

quote:

What does the fed rate drop have to do with mortgagae rates

That's what I'm asking you. You were the big cheerleader for not just the .5, but a full point cut because you wanted mortgage rates to go down.

quote:

Go take a gander at what mortgage rates do after a first cut

Mortgage rates were dropping before the rate cut. Less than two weeks after the cut they started moving back up and continue to do so.

Sooooo...?

This post was edited on 10/26/24 at 2:05 pm

Posted on 10/26/24 at 2:14 pm to Bard

quote:

because you wanted mortgage rates to go down.

Did they go down after the cut? Did i say it would be permanent?

Its amazing you think I think the fed fund rate controls mortgage rates

quote:

Mortgage rates were dropping before the rate cut. Less than two weeks after the cut they started moving back up and continue to do so.

Because inflation has been dropping like a rock and UE wentt up along with the revised jobs report of almost 1mil

Then we got another BLOW out fake jobs report. Plus 600bil in Gov spending in 2mnths and Chyna. Sooooo

Yet despite that we will still get 2 more .25 cuts cause they cant control the 2 biggest parts of the inflation reports. If you knew how to read them then you would know

This post was edited on 10/26/24 at 2:25 pm

Posted on 10/26/24 at 5:57 pm to SDVTiger

quote:

Its amazing you think I think the fed fund rate controls mortgage rates

Link:

quote:quote:

Also will this (.5 cut -Bard) affect mortgages relatively

Pricing will get better immediately but will take time with more cuts to have a bif impact

But 4%s will be popping up soon

Another:

quote:quote:

know the recent mortgage interest rates had already baked in a little bit of this, but do you think the rates will go down even more because of was 50 bps

Most likely but maybe not immediately

And another:

quote:quote:

Why do that with possible rate cuts coming and likelihood that home prices drop?

If rates drop off the cut values will increase by 10% or more with buying frenzy

.5 mortgage drop equal 2.5mil.new buyers with a 1mil homes avaialble

quote:

Because inflation has been dropping like a rock

That's being a bit generous, don't you think? PCE went up in July before having a good drop in August, meanwhile Core PCE has been inching up since June (part of the mixed messaging we've seen from the data all year). During this, PPI did indeed drop like a rock, except that Core remains sticky above 3%.

quote:

Plus 600bil in Gov spending in 2mnths and Chyna. Sooooo

Yet despite that we will still get 2 more .25 cuts cause they cant control the 2 biggest parts of the inflation reports. If you knew how to read them then you would know

I know how to read the data, I also know enough to look at the wider picture and that's why I still think .5 was foolish and a pair of quarter points before the end of the year just adds to that foolishness.

Inflation is a function of too much money in an economy, rates are generally raised or lowered to combat inflation (I know unemployment is a focus as well, but if you really have to choose a primary it's logically going to be inflation). Since COVID, the consumer and the federal government have been on a debt creation spree which has created trillions of extra dollars (which created inflation, which necessitated rates being raised). GDP growth since COVID has been predominantly created through this increasing debt load (which is increasingly only being serviced).

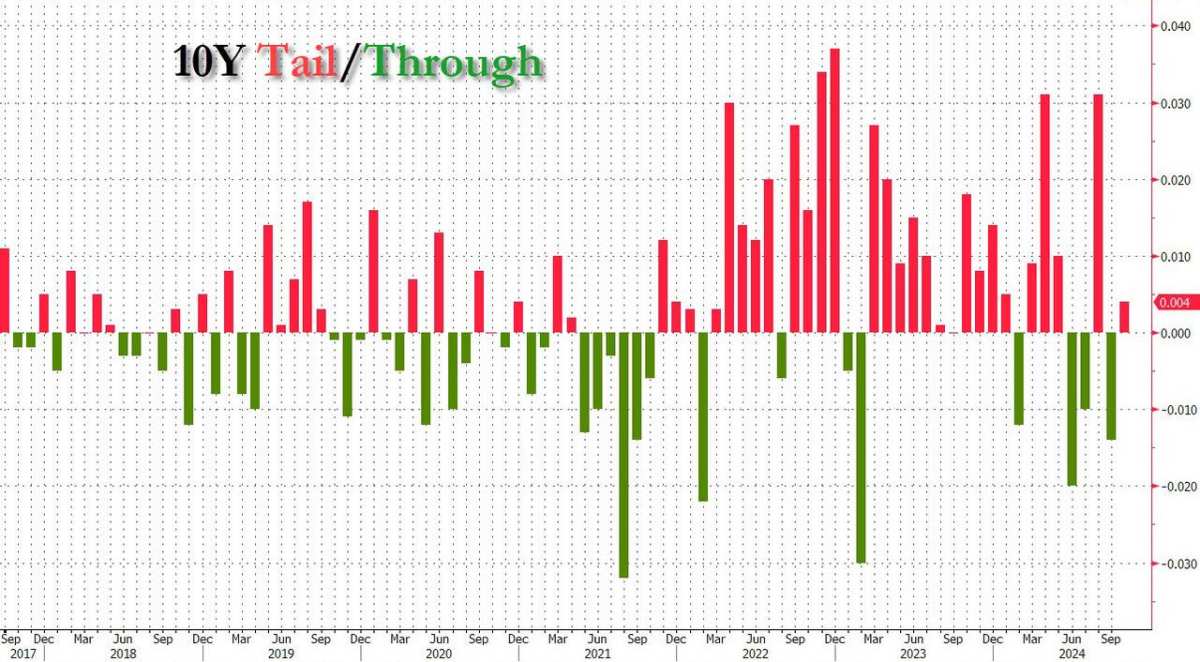

Since COVID, we've seen 10yr tails average much higher and higher much more often than we did pre-COVID (which means the Treasury is having a more difficult time selling this debt).

As long as the Treasury continues having trouble selling debt, the 10yr is going to have to keep offering higher yields. As long as mortgage rates and the 10yr move together, that means mortgage rates are going to stay high.

Posted on 10/26/24 at 6:08 pm to Bard

quote:

Pricing will get better immediately but will take time with more cuts to have a bif impact

This is true and we are seeing it. Did pricing get better immediately or not?

quote:

But 4%s will be popping up soon

This happened

quote:

If rates drop off the cut values will increase by 10% or more with buying frenzy

.5 mortgage drop equal 2.5mil.new buyers with a 1mil homes avaialble

Im not talking about the fed cut

quote:

That's being a bit generous, don't you think?

No its what has happened

quote:

know how to read the data, I

Then you wouldnt have embarrassed yourself by mocking me and claiming there was 0% chance of a .5 cut

You dont even know why the CPI is high cause you dont understand data

The charts

Posted on 10/27/24 at 11:36 am to SDVTiger

quote:

This is true and we are seeing it. Did pricing get better immediately or not?

Home prices? Not really. Redfin

Prices were already dropping due to existing mortgage rates.

According to NAHB's most recent release, new home prices have actually increased since the .5 cut while existing home prices have indeed decreased.

Now if you're talking about mortgage rates, sure. And it lasted for all of 2 weeks.

quote:

But 4%s will be popping up soon

Where? Nerdwallet, MND, Trading Economics, Zillow

At best the 30yr fixed dropped into the high 4's for all of a day or two after the cut, then proceeded to go right back up. Are you talking about special rates from some credit union or something like an FHA loan? Or something like a 10yr?

quote:

The charts

Dat mortgage rate drop, tho.

Posted on 10/28/24 at 8:42 am to Bard

quote:

Home prices? Not really

No one was talking about home prices. Good grief your iq

quote:

Now if you're talking about mortgage rates, sure. And it lasted for all of 2 weeks. ? Your stance wasn't that it would only briefly dip then jump back up, it was that it was the beginning of rates moving back down and now you're trying to play linguistic gymnastics to avoid admitting it.

It is the beginning of rates moving lower

quote:

At best the 30yr fixed dropped into the high 4's

Thank you for admitting im right

Page 3 of 3

Page 3 of 3

Popular

Back to top