- My Forums

- Tiger Rant

- LSU Score Board

- LSU Recruiting

- SEC Rant

- SEC Score Board

- Saints Talk

- Pelicans Talk

- More Sports Board

- Fantasy Sports

- Golf Board

- Soccer Board

- O-T Lounge

- Tech Board

- Home/Garden Board

- Outdoor Board

- Health/Fitness Board

- Movie/TV Board

- Book Board

- Music Board

- Political Talk

- Money Talk

- Fark Board

- Gaming Board

- Travel Board

- Food/Drink Board

- Ticket Exchange

- TD Help Board

Customize My Forums- View All Forums

- Show Left Links

- Topic Sort Options

- Trending Topics

- Recent Topics

- Active Topics

Started By

Message

re: Expiration of “Trump” tax cuts

Posted on 5/3/24 at 2:59 pm to Bestbank Tiger

Posted on 5/3/24 at 2:59 pm to Bestbank Tiger

Sorry…to be clear I was talking about a company sponsored tax deferred 401k vs a company sponsored after tax Roth 401k.

Are you saying the tax deferred is better?

I was under the assumption that the Roth was the way to go….so much so that people are actively converting traditional IRAs to Roths.

Are you saying the tax deferred is better?

I was under the assumption that the Roth was the way to go….so much so that people are actively converting traditional IRAs to Roths.

4

4

Posted on 5/3/24 at 3:03 pm to SquatchDawg

quote:

Sorry…to be clear I was talking about a company sponsored tax deferred 401k vs a company sponsored after tax Roth 401k.

Are you saying the tax deferred is better?

I was under the assumption that the Roth was the way to go….so much so that people are actively converting traditional IRAs to Roths.

I was saying pay the taxes later, since even with a higher rate in the future you're likely going to be in a higher bracket now.

Of course that's purely speculative. You could end up getting screwed if you use pretax dollars now.

Posted on 5/3/24 at 4:12 pm to SquatchDawg

quote:

was under the assumption that the Roth was the way to go….so much so that people are actively converting traditional IRAs to Roths.

I would imagine most people are converting Roths as a bridge from early retirement to 59.5. Or they are in a super low tax bracket. Or they fricked up and listened to Dave Ramsey who for some reason encourages everyone to do a back door Roth no matter what be their financial situation is.

It doesn't make a lot of sense (to me) to fund a Roth in your prime earning years when you're in a high bracket. Roths generally make the most sense when you're in a low tax bracket (i.e. early in your career).

Posted on 5/3/24 at 6:18 pm to SquatchDawg

quote:

Are you saying the tax deferred is better?

Often, yes. Many people mistakenly compare their top bracket today with their projected top bracket at withdrawal. As I tried to explain in earlier post, traditional withdrawals will usually be taxed at an effective rate lower that is lower because they will fill the lower brackets first (unless you have other income to fill those brackets in retirement.)

My guess is many people have mixed up the advice to fund a Roth IRA after maxing employer plans with the misguided advice that Roth 401k usually beats traditional 401k. Also, much advice is geared to new investors and thus skews to early career relatively lower earning years thus the advice to frontload Roth 401k. It's also a way of oversimplifying so new investors take action instead of getting stuck in analysis paralysis.

Posted on 5/3/24 at 7:05 pm to SquatchDawg

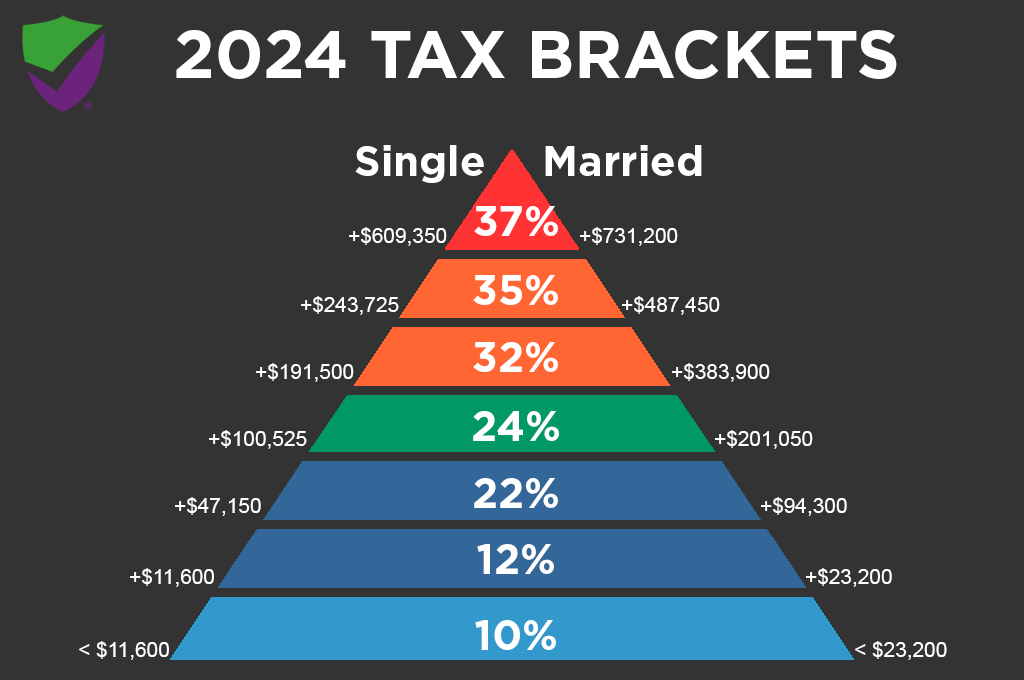

Example: married filing joint, $150k taxable income now, $150k annual retirement. Assumptions: no other retirement income, using 2024 brackets without inflation adjustment for simplicity sake (fair because not adjusting withdrawal amount for inflation either).

Tax bracket today: 22% thus each extra dollar you choose to pay tax on and contribute to Roth is taxed at 22% (thus only contributing .78¢) or you defer tax of 22% and contribute that full dollar to traditional.

At retirement the Roth balance will be 22% smaller than equivalent traditional contribution (unless you max annual contributions in which case to compare apples/apples you would invest the excess traditional tax savings either in a Roth IRA, taxable brokerage, etc)

Retirement Withdrawals from traditional are taxed at a lower EFFECTIVE RATE. First, $29k is tax free due to standard deduction. Next $23k taxed at 10% then additional up to $94k taxed at 12%. At that point you have ~$122k of withdrawals that have been taxed at rates from 0-12% (instead of 22% when you earned them) Only at that point does the last $18k get taxed in the 22% bracket.

Even if brackets are raised it isnt likely your bottom brackets will exceed the top rate you pay today (unles low income in which case Roth is easy choice.)

The math can still work in favor of traditional if you have other income in retirement but its a little more nuanced. You can have quite a bit of income before withdrawals are fully taxed in same bracket or higher than during contribution years. Of course there are other considerations such as triggering tax on SS benefits, ACA subsidy income limits, IRMAA, RMDs on traditional but not Roth etc. Thus, it is a good idea to have $ in multiple tax buckets so you can optimize where you pull from in retirement year to year based on needs and situation.

Tax bracket today: 22% thus each extra dollar you choose to pay tax on and contribute to Roth is taxed at 22% (thus only contributing .78¢) or you defer tax of 22% and contribute that full dollar to traditional.

At retirement the Roth balance will be 22% smaller than equivalent traditional contribution (unless you max annual contributions in which case to compare apples/apples you would invest the excess traditional tax savings either in a Roth IRA, taxable brokerage, etc)

Retirement Withdrawals from traditional are taxed at a lower EFFECTIVE RATE. First, $29k is tax free due to standard deduction. Next $23k taxed at 10% then additional up to $94k taxed at 12%. At that point you have ~$122k of withdrawals that have been taxed at rates from 0-12% (instead of 22% when you earned them) Only at that point does the last $18k get taxed in the 22% bracket.

Even if brackets are raised it isnt likely your bottom brackets will exceed the top rate you pay today (unles low income in which case Roth is easy choice.)

The math can still work in favor of traditional if you have other income in retirement but its a little more nuanced. You can have quite a bit of income before withdrawals are fully taxed in same bracket or higher than during contribution years. Of course there are other considerations such as triggering tax on SS benefits, ACA subsidy income limits, IRMAA, RMDs on traditional but not Roth etc. Thus, it is a good idea to have $ in multiple tax buckets so you can optimize where you pull from in retirement year to year based on needs and situation.

This post was edited on 5/3/24 at 7:08 pm

Page 1 of 1

Page 1 of 1

Popular

Back to top