- My Forums

- Tiger Rant

- LSU Recruiting

- SEC Rant

- Saints Talk

- Pelicans Talk

- More Sports Board

- Fantasy Sports

- Golf Board

- Soccer Board

- O-T Lounge

- Tech Board

- Home/Garden Board

- Outdoor Board

- Health/Fitness Board

- Movie/TV Board

- Book Board

- Music Board

- Political Talk

- Money Talk

- Fark Board

- Gaming Board

- Travel Board

- Food/Drink Board

- Ticket Exchange

- TD Help Board

Customize My Forums- View All Forums

- Show Left Links

- Topic Sort Options

- Trending Topics

- Recent Topics

- Active Topics

Started By

Message

re: Someone help me understand

Posted on 7/28/17 at 1:33 pm to bonhoeffer45

Posted on 7/28/17 at 1:33 pm to bonhoeffer45

quote:

So you now pay $66,875 a year for a family plan?

no my monthly premium was sub-$100/mo in 2009 and is now over $500/mo (deductibles have gone up about as much)

single. male. not a leech. period mid-20s to mid-30s

1

1

Posted on 7/28/17 at 1:36 pm to SlowFlowPro

quote:

no my monthly premium was sub-$100/mo in 2009 and is now over $500/mo (deductibles have gone up about as much)

single. male. not a leech. period mid-20s to mid-30s

And I suppose you are in the employer market?

Like I just said, if you managed to have a full benefit, low deductible, no employer cost sharing plan for under $100 then you hit the jackpot. The data said the average plan at that period was typically 4x that much.

But what I am not seeing you square is why you think repeal will magically push healthcare costs to 2009 levels and reverse a trend that was ongoing well before Obama was even in the US senate?

Truth is, the failure of the ACA is that it didn't reverse already ongoing trends, not that it originated them. So the logic that just repealing it fixes the underlying problems driving premium inflation is not true.

This post was edited on 7/28/17 at 1:38 pm

Posted on 7/28/17 at 1:39 pm to bonhoeffer45

quote:Indeed.

These trends existed well before the ACA.

Posted on 7/28/17 at 1:41 pm to NC_Tigah

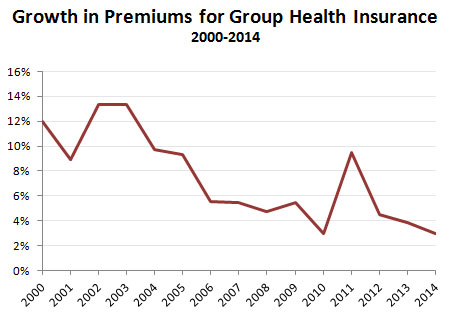

I don't know if you just don't know how to read charts, but that chart is not proving what you want it to prove..... Unless you are already conceding the point. But that is never like you.

This post was edited on 7/28/17 at 1:45 pm

Posted on 7/28/17 at 1:42 pm to bonhoeffer45

quote:

And I suppose you are in the employer market?

no individual market. my employer has never paid for my health care (i said i'm not a leech)

quote:

The data said the average plan at that period was typically 4x that much.

for young people with no PECs?

quote:

But what I am not seeing you square is why you think repeal will magically push healthcare costs to 2009 levels and reverse a trend that was ongoing well before Obama was even in the US senate?

i never said that. my question to 5th was always whether or not MY rates would have gone up 500% since 2010 had the ACA not passed

i understand i wouldn't be paying $100/month. even if inflation was insane and i was paying 2.5x what i was (which is almost double the increase rates you posted of 131%), i'd still be paying HALF of what i am today

quote:

, the failure of the ACA is that it didn't reverse already ongoing trends, not that it originated them. So the logic that just repealing it fixes the underlying problems driving premium inflation is not true.

it is true for certain demos

the demos the ACA was written to frick over to subsidize everyone else would see much less inflation over time

Posted on 7/28/17 at 1:47 pm to bonhoeffer45

quote:

Truth is, the failure of the ACA is that it didn't reverse already ongoing trends, not that it originated them. So the logic that just repealing it fixes the underlying problems driving premium inflation is not true.

Not entirely true. The statistics you showed reflect premium increases. More than 20% of American's have switched to High Deductible Health Plans in the last 10 years - from around 5% to almost 30%. Those plans, by definition have much lower premiums - often times less than half the premium of other plans. That alone is going to slow premium growth and give us the illusion that the cost of care is slowing down.

The offset, is that the out-of-pocket cost is increasing at a much, much higher rate, and that isn't shown in the statistics you are showing. As someone else pointed out, that is not showing up in the subsidies, either.

Posted on 7/28/17 at 1:50 pm to SlowFlowPro

quote:

for young people with no PECs?

Young people were typically better off price wise. But unless you are young forever, you are going to continue inching into the more expensive brackets.

I was a model of health in 2006 when I was on the individual market temporarily,and was never able to find a policy that was below 100 dollars that wasn't mostly shite, so I do wonder where you lived that you got such a great policy for so cheap?

quote:

i never said that. my question to 5th was always whether or not MY rates would have gone up 500% since 2010 had the ACA not passed

i understand i wouldn't be paying $100/month. even if inflation was insane and i was paying 2.5x what i was (which is almost double the increase rates you posted of 131%), i'd still be paying HALF of what i am today

Like I said, you probably would be slightly better off, though you would still probably be cursing your healthcare bills. But for how long would you remain better off? Unless you managed to stop aging, as you get older, the pocketbook hit in a less dispersed private market would end up being particularly harsh as most insurers would prefer to charge people a lot more as they age unless you are doing things like the ACA to offset it.

Posted on 7/28/17 at 1:57 pm to Jax-Tiger

quote:

Not entirely true. The statistics you showed reflect premium increases. More than 20% of American's have switched to High Deductible Health Plans in the last 10 years - from around 5% to almost 30%. Those plans, by definition have much lower premiums - often times less than half the premium of other plans. That alone is going to slow premium growth and give us the illusion that the cost of care is slowing down.

If you go to page 123(and at various places in the report before and after) they have a section analyzing high-deductible health plans.

Employers have pushed employees to higher deductible plans, but premiums in that sector are still on the rise. Though I am sure in some instances there are people that saw their premiums drop or slow because they are switched to a plan with much higher out-of-pocket expenses and benefit shrink.

Deductibles are the hidden cost that sometimes gets forgotten about. You are right about that. It is something I frequently saw journalists leave out about the CBO forecasts on the AHCA and the like. Pointing out that compared to the baseline, younger healthier people would have cheaper premiums in 2026 vs the ACA arrangement in 2026. The caveat being that the lower premiums would be offset entirely by higher deductibles and less benefits. And if you are someone that was 35 today, then 45 by the time of the AHCA implementation in 2026, you would be having your rates climb faster due to the change in age ratings.

Posted on 7/28/17 at 2:00 pm to bonhoeffer45

quote:Spoiler alert: he doesn't

I don't know if you just don't know how to read charts,

Posted on 7/28/17 at 2:01 pm to NC_Tigah

quote:Quoting this because he tends to edit these and I wanna preserve this one in amber

Indeed.

Posted on 7/28/17 at 2:08 pm to ODanMan

Obamacare bent the cost curve upwards. It's a program that required 10 years of taxes yet provides 6 years of service. The reason being is like many others noted it was meant to fail.

Posted on 7/28/17 at 2:09 pm to bonhoeffer45

quote:

Like I said, you probably would be slightly better off, though you would still probably be cursing your healthcare bills. But for how long would you remain better off? Unless you managed to stop aging, as you get older, the pocketbook hit in a less dispersed private market would end up being particularly harsh as most insurers would prefer to charge people a lot more as they age

over time i should accumulate more wealth and income so that offsets the increase

a bit more logical than giving breaks to those who have had decades to accumulate wealth and penalizing those trying to start their careers, i'd hope you'd agree

Posted on 7/28/17 at 2:10 pm to 5thTiger

quote:

I don't know you or your situation..but probably. That is what the data/trends say.

My own personal trend shows that my premiums barely increased prior to Obamacare being forced on us.

Posted on 7/28/17 at 2:15 pm to imjustafatkid

quote:

My own personal trend shows that my premiums barely increased prior to Obamacare being forced on us.

me too but that's a function of our age

we'd 100% be paying more now. probably in that 130-150% level that we say prior to the ACA

i don't think anyone is intellectually dishonest enough to say we'd be worse off than the 400-500% increase we have seen

Posted on 7/28/17 at 2:16 pm to ODanMan

Open up competition among states for insurance. Free market. Give me a price list and let me pick a doctor. Stop with absurd costs associated with regulations. Profit

Posted on 7/28/17 at 2:21 pm to SlowFlowPro

quote:

over time i should accumulate more wealth and income so that offsets the increase

a bit more logical than giving breaks to those who have had decades to accumulate wealth and penalizing those trying to start their careers, i'd hope you'd agree

Perhaps it would make more sense if wage growth and personal wealth outpaced healthcare inflation. And we didn't have this weird trend, especially in rural areas, of working class, non-college graduates, actually seeing their wages decrease after they hit a middle age threshold. Putting them in a particularly vulnerable position if you jack up their rates.

And while ironically the employer tax credit has been shown with pretty solid evidence to be a major driver in wage stagnation, it is probably not going away.

The way the ACA is set up is based on income when it comes to subsidies. So while the 3:1 age rating means younger people pay more, the theory is that younger people with lower incomes will find themselves getting more in subsides to pay off that. Now I think the Dems fricked up on how they structured it, since people that are fortunate enough to get good jobs are the ones that get hurt. If you are 27 and make 25,000 you are pretty golden in terms of affording health insurance compared to a 27 year old making 60,000 and living in an expensive city(though I think both situations are not particularly ideal).

But I will say, I am more then open to re-structuring the system in a way that addresses this problem. As is the young people with middle incomes are getting squeezed while people on either side tend to be better off comparatively. But it should be done in a way that isn't swapping harm for one group to an equal or greater harm to another.

This post was edited on 7/28/17 at 2:25 pm

Posted on 7/28/17 at 2:26 pm to bonhoeffer45

quote:

But I will say, I am more then open to re-structuring the system in a way that addresses this problem.

quote:

But it should be done in a way that isn't swapping harm for one group to an equal or greater harm to another.

literally impossible

the ACA just shifts costs onto different groups

any restructure will help one group and hurt another

Posted on 7/28/17 at 2:35 pm to bonhoeffer45

quote:Really?

I don't know if you just don't know how to read charts

It's unclear if your response relates to group health insurance which seems the closest analog attainable to ACA unsubsidized premiums, or confusion about rate of inflation. Try making a point, and we'll discuss it.

Posted on 7/28/17 at 2:36 pm to 5thTiger

quote:

It slowed the rise in costs of medical care.

Posted on 7/28/17 at 2:38 pm to 5thTiger

quote:

don't know you or your situation..but probably. That is what the data/trends say

Page 4 of 6

Page 4 of 6

Popular

Back to top