- My Forums

- Tiger Rant

- LSU Recruiting

- SEC Rant

- Saints Talk

- Pelicans Talk

- More Sports Board

- Fantasy Sports

- Golf Board

- Soccer Board

- O-T Lounge

- Tech Board

- Home/Garden Board

- Outdoor Board

- Health/Fitness Board

- Movie/TV Board

- Book Board

- Music Board

- Political Talk

- Money Talk

- Fark Board

- Gaming Board

- Travel Board

- Food/Drink Board

- Ticket Exchange

- TD Help Board

Customize My Forums- View All Forums

- Show Left Links

- Topic Sort Options

- Trending Topics

- Recent Topics

- Active Topics

Started By

Message

Finally found someone that agrees with me on the absurdity of the emergency fund

Posted on 5/16/17 at 3:37 pm

Posted on 5/16/17 at 3:37 pm

LINK

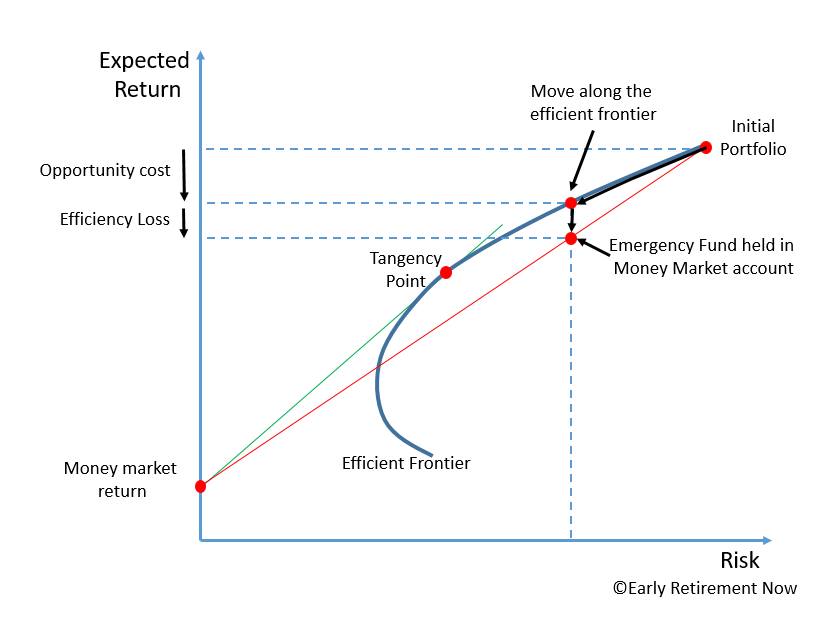

In our financial plan, you will never find the one staple item that every so-called financial planner calls the cornerstone of a responsible financial plan: the emergency fund. We have none. Zilch. Nada.

With the exception of about $100, maybe $200 in small bills in a safe place in our home, and about $1,000 in cash in our checking account we have zero cash sitting around. Not that we are so cash-strapped that we couldn’t afford an emergency fund. Our net worth is solidly in the seven figures and north of 30-35 times our projected retirement spending budget. We never had an emergency fund and never plan to have one. That doesn’t mean that we never have unexpected spending shocks. If we do need cash we will get it from our vast supply of “emergency cash,” which is, in exactly that order:

Credit card float (=interest free loan from the credit card company between the transaction and the credit card payment due date)

Papa ERN’s paychecks

The $100,000 HELOC (home equity line of credit) on our condo

Finally, a large sum in several brokerage accounts, more than half our liquid asset net worth

In our financial plan, you will never find the one staple item that every so-called financial planner calls the cornerstone of a responsible financial plan: the emergency fund. We have none. Zilch. Nada.

With the exception of about $100, maybe $200 in small bills in a safe place in our home, and about $1,000 in cash in our checking account we have zero cash sitting around. Not that we are so cash-strapped that we couldn’t afford an emergency fund. Our net worth is solidly in the seven figures and north of 30-35 times our projected retirement spending budget. We never had an emergency fund and never plan to have one. That doesn’t mean that we never have unexpected spending shocks. If we do need cash we will get it from our vast supply of “emergency cash,” which is, in exactly that order:

Credit card float (=interest free loan from the credit card company between the transaction and the credit card payment due date)

Papa ERN’s paychecks

The $100,000 HELOC (home equity line of credit) on our condo

Finally, a large sum in several brokerage accounts, more than half our liquid asset net worth

This post was edited on 5/16/17 at 3:41 pm

13

13

Posted on 5/16/17 at 3:42 pm to anc

so, basically how much money is too much to have sitting in a money market bank account?

Posted on 5/16/17 at 3:43 pm to anc

I'm an idiot!

This post was edited on 5/16/17 at 3:53 pm

Posted on 5/16/17 at 3:47 pm to OnTheBrink

How is it humble bragging to state that I disagree with keeping "3 months salary" or whatever the flavor of the month is in a low interest account? Ive always thought this was stupid but it seems to be basic financial advice.

Posted on 5/16/17 at 3:49 pm to OnTheBrink

I've been lobbying this to the wife for YEARS.

If one of us were to lose our job we could easily cut back on expenses. I think at the maximum it should be a few months of the mortgage.

If one of us were to lose our job we could easily cut back on expenses. I think at the maximum it should be a few months of the mortgage.

This post was edited on 5/16/17 at 3:50 pm

Posted on 5/16/17 at 3:51 pm to anc

I'm with you on not having so much in the bank but $1000 in checking is a bit extreme if you are paying bills, credit card, mortgage, etc out of that account

Posted on 5/16/17 at 3:52 pm to anc

quote:

How is it humble bragging to state that I disagree with keeping "3 months salary" or whatever the flavor of the month is in a low interest account?

You know what, you are right, I read it as your annual salary is well into the 7 figures. I apologize and will remove it.

And to add to the thread, You sort of do have an emergency fund with the $1,500 or so you have sitting around, obviously not the 3-6 months people suggest. I don't think most people have this mountain of cash just sitting around waiting to get laid off and say "Yep, now is the time to use it!". I would say most people are in your shoes and have it spread out.

Posted on 5/16/17 at 3:56 pm to OnTheBrink

quote:

You know what, you are right, I read it as your annual salary is well into the 7 figures. I apologize and will remove it.

And to add to the thread, You sort of do have an emergency fund with the $1,500 or so you have sitting around, obviously not the 3-6 months people suggest. I don't think most people have this mountain of cash just sitting around waiting to get laid off and say "Yep, now is the time to use it!". I would say most people are in your shoes and have it spread out.

The text is an excerpt from the linked article. I'm not quite there yet!!!!

Posted on 5/16/17 at 4:02 pm to anc

I agree fully OP, but I don't think its bad advice. I don't know why you'd have more than $10k not invested in some form or fashion, but hey whatever floats your boat.

I also think that a ROTH IRA is a very underappreciated form of an "emergency" fund. You can pull out whatever cash you put in there tax free, you just can't touch the interest earned. So if you aren't maxing your roth, its a great place for an "emergency" fund to build up.

I also think that a ROTH IRA is a very underappreciated form of an "emergency" fund. You can pull out whatever cash you put in there tax free, you just can't touch the interest earned. So if you aren't maxing your roth, its a great place for an "emergency" fund to build up.

Posted on 5/16/17 at 4:05 pm to anc

Damn, makes me rethink my emergency fund and cash in my safe

Posted on 5/16/17 at 4:24 pm to anc

Emergency funds are for people who need budgets (the vast majority of people). Guy is worth millions, so of course it is pointless.

Most people can't float $10k on a credit card and pay it all off the next month before paying interest. Most people don't have "several brokerage accounts" where they can just go liquidate assets.

Most people can't float $10k on a credit card and pay it all off the next month before paying interest. Most people don't have "several brokerage accounts" where they can just go liquidate assets.

This post was edited on 5/16/17 at 4:31 pm

Posted on 5/16/17 at 4:32 pm to baldona

quote:

I don't know why you'd have more than $10k not invested in some form or fashion, but hey whatever floats your boat.

I can understand if you are saving and plan to use the money in 3-5 years.

Posted on 5/16/17 at 4:34 pm to anc

Oh, I agree that holding cash in a savings account is usually a bad way to address the emergency fund issue.

The task is to be able to quickly and easily raise cash in the event of an emergency. A HELOC certainly fits this, but some people don't own a home or have enough equity in one. A Roth (or a portion that is invested conservatively) will too. If you have credit card debt, paying it off is the way to go b/c if you have an emergency you can charge it back up. Etc. etc.

A taxable savings account is probably one of the least effective ways to stash money for a rainy day.

The task is to be able to quickly and easily raise cash in the event of an emergency. A HELOC certainly fits this, but some people don't own a home or have enough equity in one. A Roth (or a portion that is invested conservatively) will too. If you have credit card debt, paying it off is the way to go b/c if you have an emergency you can charge it back up. Etc. etc.

A taxable savings account is probably one of the least effective ways to stash money for a rainy day.

Posted on 5/16/17 at 4:37 pm to anc

No chance I can live with $1,000 in our checking. CC bills are about $3,000/mo and mortgage + car note auto drafts are another couple grand. Yall must have no reoccurring expenses and not spend anything on your CCs

Posted on 5/16/17 at 4:59 pm to anc

quote:

Finally found someone that agrees with me on the absurdity of the emergency fund

Well you should have some part of your portfolio in fixed income, which is easily convertable to cash.

I don't think anyone believes the emergency fund has to be in cash, but you want something relatively stable.

I would keep about 15k in cash, which is two months operating expenses for the wife and I. But have a few hundo in fixed income positions that I could liquidate.

I actually have about 50k in cash right now as I lost my job and that was my severance.

Posted on 5/16/17 at 8:17 pm to TigerTatorTots

quote:

No chance I can live with $1,000 in our checking. CC bills are about $3,000/mo and mortgage + car note auto drafts are another couple grand. Yall must have no reoccurring expenses and not spend anything on your CCs

This. If he's worth as much as he says he is, then he has more than that in his checking. I'm OT poor and it takes a minimum balance of several thousand dollars to cover the mortgage,credit card, and Auto drafts which come out regularly. And we're debt free(other than house) at that.

This post was edited on 5/16/17 at 8:18 pm

Posted on 5/16/17 at 9:20 pm to anc

It all sounds good in theory, but it also sounds like a guy who has never replaced a 8k HVAC unit, and doesn't realize that you can get a significant discount paying in cash/check, as opposed to credit card (even with the rewards). Not to mention the hassle of a heloc or pulling money from a Roth loan if a larger expense. The x% in yearly gains from keeping it that tight can be made up by the x% in discount every year by paying cash for jewelry, furniture, and other things that are more negotiable in cash. Not to mention the convenience factor.

Posted on 5/16/17 at 9:23 pm to dragginass

Maybe I didn't read through the link carefully enough, but I found that part curious too.

If the main point is that it's not necessary to have an emergency fund in wads of hundreds under the mattress, then OK. But having been through two deep recessions (so far), I know VERY well that considering HELOCs, credit cards, or other borrowed funds, to be part of any sort of emergency fund is wishful thinking at best. I was in the middle of a 60% LTV refi when the credit markets froze up about a decade ago. My loan was approved but the bank president called me to say that they couldn't fund it at that time. It took an additional two weeks to get it closed. I had a personal line of credit with them also. That got arbitrarily cut in half. The (unused) HELOC that I had with BofA got totally wiped out. Banks were cutting and freezing lines of credit and card limits left and right - even for higher net worth/income borrowers. A friend of mine who typically borrowed against invoices nearly lost his business because of financing issues.

So there I was thinking that I had the world on a string with a good net worth, high credit score, good income, equities and properties... and I felt like a wet cigarette at a party. After that, I've always kept a few thousand squirreld away. Although I'd consider free cash in my trading account, my Roth and other liquid assets to be available in a true emergency. If the lost interest and opportunity cost of that really affects me over the next 10-15 years, I likely did some other things "wronger" than that.

If the main point is that it's not necessary to have an emergency fund in wads of hundreds under the mattress, then OK. But having been through two deep recessions (so far), I know VERY well that considering HELOCs, credit cards, or other borrowed funds, to be part of any sort of emergency fund is wishful thinking at best. I was in the middle of a 60% LTV refi when the credit markets froze up about a decade ago. My loan was approved but the bank president called me to say that they couldn't fund it at that time. It took an additional two weeks to get it closed. I had a personal line of credit with them also. That got arbitrarily cut in half. The (unused) HELOC that I had with BofA got totally wiped out. Banks were cutting and freezing lines of credit and card limits left and right - even for higher net worth/income borrowers. A friend of mine who typically borrowed against invoices nearly lost his business because of financing issues.

So there I was thinking that I had the world on a string with a good net worth, high credit score, good income, equities and properties... and I felt like a wet cigarette at a party. After that, I've always kept a few thousand squirreld away. Although I'd consider free cash in my trading account, my Roth and other liquid assets to be available in a true emergency. If the lost interest and opportunity cost of that really affects me over the next 10-15 years, I likely did some other things "wronger" than that.

Posted on 5/16/17 at 9:28 pm to anc

quote:

Finally, a large sum in several brokerage accounts, more than half our liquid asset net worth

Won't you get taxed heavily if you have to pull a lot of money out of the brokerage accounts?

Posted on 5/16/17 at 9:35 pm to anc

I keep enough to pay for the roof over my head for a few months and some for my golf habit.

Other than that, I max out my 401k, HSA and buy whatever stock or mutual fund I can at the time.

I love buying stocks - freaking love it. If all hell breaks lose, I won't be the only dumbass in a bind.

Other than that, I max out my 401k, HSA and buy whatever stock or mutual fund I can at the time.

I love buying stocks - freaking love it. If all hell breaks lose, I won't be the only dumbass in a bind.

Page 1 of 2

Page 1 of 2

Popular

Back to top