- My Forums

- Tiger Rant

- LSU Recruiting

- SEC Rant

- Saints Talk

- Pelicans Talk

- More Sports Board

- Fantasy Sports

- Golf Board

- Soccer Board

- O-T Lounge

- Tech Board

- Home/Garden Board

- Outdoor Board

- Health/Fitness Board

- Movie/TV Board

- Book Board

- Music Board

- Political Talk

- Money Talk

- Fark Board

- Gaming Board

- Travel Board

- Food/Drink Board

- Ticket Exchange

- TD Help Board

Customize My Forums- View All Forums

- Show Left Links

- Topic Sort Options

- Trending Topics

- Recent Topics

- Active Topics

Started By

Message

Flood Insurance Questions

Posted on 3/14/16 at 4:51 pm

Posted on 3/14/16 at 4:51 pm

At first, I was paying $700 a year for flood insurance on my home (flood zone A). Over the past 7 years it's crept up to about $1100, as of my prior year's premium. However, the most recent premium was a whopping $3,896.

My insurance company called FEMA, and apparently their only reaction was "Wow that's a lot" and can't tell me why it went up so much. They suggested I get an elevation certificate. However, I did, about 7 years ago. It said I was 2 feet below the flood plain, and the policy was apparently written without the certificate because neither FEMA nor my insurance company have any record of it.

Can't seem to find the damned thing either, so I may have to get another one if no one has any record of it.

But, if I'm 2 feet below, is there really any point? Wouldn't it just increase my premium further?

For the record, I'm not bitching about the premium if that's what I should be paying (Although, if it shoots any higher I'll start to get worried). I know "it never floods here" are famous last words and not directly indicative of how premiums are determined. I'm just surprised at the substantial increase and not very informed about these sort of things. Any insight is appreciated.

My insurance company called FEMA, and apparently their only reaction was "Wow that's a lot" and can't tell me why it went up so much. They suggested I get an elevation certificate. However, I did, about 7 years ago. It said I was 2 feet below the flood plain, and the policy was apparently written without the certificate because neither FEMA nor my insurance company have any record of it.

Can't seem to find the damned thing either, so I may have to get another one if no one has any record of it.

But, if I'm 2 feet below, is there really any point? Wouldn't it just increase my premium further?

For the record, I'm not bitching about the premium if that's what I should be paying (Although, if it shoots any higher I'll start to get worried). I know "it never floods here" are famous last words and not directly indicative of how premiums are determined. I'm just surprised at the substantial increase and not very informed about these sort of things. Any insight is appreciated.

This post was edited on 3/14/16 at 4:54 pm

2

2

Posted on 3/14/16 at 4:56 pm to ILikeLSUToo

the BR flood maps were changed back in 2008. if you had flood insurance then, you were semi grandfathered in on your premiums. but now you have to pay the new rates in full as the grace period ended.

LSU flood maps

this is a good site to look at where you stand as far as flood plane

EDIT: if you click on the parish, then use the "layers"icon on top right you can see what changed in 2008.

EDIT #2: FEMA Grandfathered rules

LSU flood maps

this is a good site to look at where you stand as far as flood plane

EDIT: if you click on the parish, then use the "layers"icon on top right you can see what changed in 2008.

EDIT #2: FEMA Grandfathered rules

This post was edited on 3/14/16 at 5:02 pm

Posted on 3/14/16 at 5:03 pm to ILikeLSUToo

Maybe your EC wasn't used bc it didn't help

Eta do you recall the surveyor call them up for copy on file

Eta do you recall the surveyor call them up for copy on file

This post was edited on 3/14/16 at 5:09 pm

Posted on 3/14/16 at 5:08 pm to tigeraddict

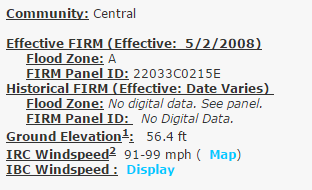

So it looks like my house was in Zone AE, and then in May 2008 it became Zone A. I purchased the home and the policy after that.

Posted on 3/14/16 at 5:10 pm to Chad504boy

quote:

Maybe your EC wasn't used bc it didn't help

That's my guess, which is why I'd hate to drop $400 on a new one for the same result.

quote:

do you recall the surveyor call them up for copy on file

Trying to figure that out, too. I found them via Google, so I may just have to start going down the list and calling them all.

Page 1 of 1

Page 1 of 1

Back to top